POWER: Italy November Power to Open Lower

Italy November power is expected to trade down, once liquid, with losses in EU gas prices.

- Italy Base Power NOV 25 closed up 0.4% at 108.92 EUR/MWh on 2 Oct

- Italy Power Cal 26 closed up 0.5% at 104.28 EUR/MWh on 2 Oct

- TTF Gas NOV 25 down 1.3% at 31.05 EUR/MWh

- EUA DEC 25 up 0.6% at 77.87 EUR/MT

- TTF front month has been bouncing within a €1/MWh range since falling to a low of €30.735/MWh on Oct. 1, with returning pipeline supplies set against limited storage injections.

- The latest two-week ECMWF weather forecast for Rome suggests mean temperatures will remain below normal throughout the forecast period.

- Mean temperatures in Rome are forecast at 14.9C on Saturday and at 18.3C on Sunday, from 14.9C on Friday and below the seasonal normal.

- The PUN index declined to €96.11/MWh for Friday’s delivery, down from €104.40/MWh the day before.

- Wind output in Italy is forecast at 2.61GW during base load on Saturday and at 4.37GW on Sunday, from 6.07GW on Friday. Solar PV output is forecast at 8.99GW during peak load on Saturday and at 6.39GW on Sunday, from 8.83GW on Friday according to SpotRenewables.

- Residual load in Italy is forecast at 19.87GWh/h on Saturday and at 14.16GWh/h on Sunday, from 20.87GWh/h on Friday, Reuters data showed.

- Power demand in Italy is forecast at 27.41GWh/h on Saturday and at 23.62GWh/h on Sunday, from 31.79GWh/h on Friday, Reuters data showed.

- Italian residential/commercial gas consumption is forecast at 45.8mcm/d on Saturday and at 41.9mcm/d on Sunday, from 67.4mcm/d on Friday, Bloomberg data showed.

- Italy’s hydro balance forecast has been revised slightly revised up to 1.14TWh on 17 October, from 1.08TWh previously, Bloomberg data showed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: 30-Year Yields Near Next Upside Level

UK 30-Year yields have again hit the highest level since the late ‘90s, 5.735%. Moving average studies further underscore the bearish trend in long end UK paper/uptrend in yields. The 1.236 Fibonacci projection of the Jun 13-Jul 18-Aug 5 price swing nears (5.74%). The next projection of that move above there lies at 5.79%.

BUNDS: New 14yrs high for the German 30yr Yield

- A new 14yrs high for the German 30yr Yield, highest since July 2011.

- Next upside level is at 3.45%, and this would equate to 111.16 in UBU5 Today.

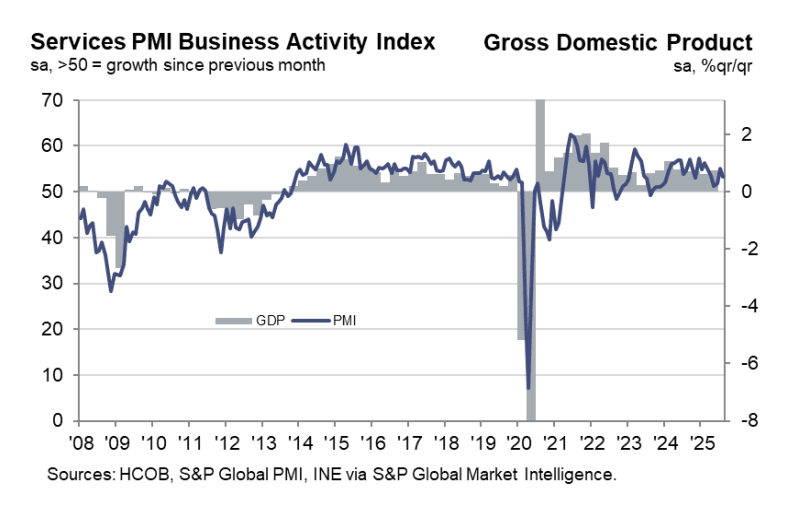

SPAIN DATA: August Services/Composite PMIs: Weaker Than Exp, But Still Solid

The Spanish services PMI was weaker-than-expected at 53.2 (vs 54.5 cons, 55.1 prior), somewhat disappointing after a stronger-than-expected manufacturing reading on Monday. That left the composite PMI at 53.7 (vs 54.9 cons, 54.7 prior). The composite PMI has nonetheless been above 50 for 24 consecutive months now, underscoring Spain’s position as the Eurozone growth outperformer post Covid.

Details of the PMI were solid from an activity standpoint, but its worth noting another acceleration in inflationary pressures amongst services firms.

Key notes from the release:

- “Higher activity was again principally linked to a rise in new business”…“ Some firms pointed to the release of previously delayed contract agreements as a reason for increased new work. Improved product and service provision also helped to support the marked rise in sales volumes”.

- “Firms were suitably encouraged to take on additional staff in August, largely in response to higher workloads overall”….“ Employment levels have now risen on a continuous basis for just under three years, although growth in August was noticeably slower than July’s four-month high”

- “Prices data showed a pick-up in inflationary pressures. Input prices overall rose to the greatest degree since February with firms pointing to higher supplier charges in general”.

- “Service providers took advantage of a positive demand environment by passing on their increased input costs to clients wherever possible. This helped to underpin the steepest rise in selling prices since April 2024”.