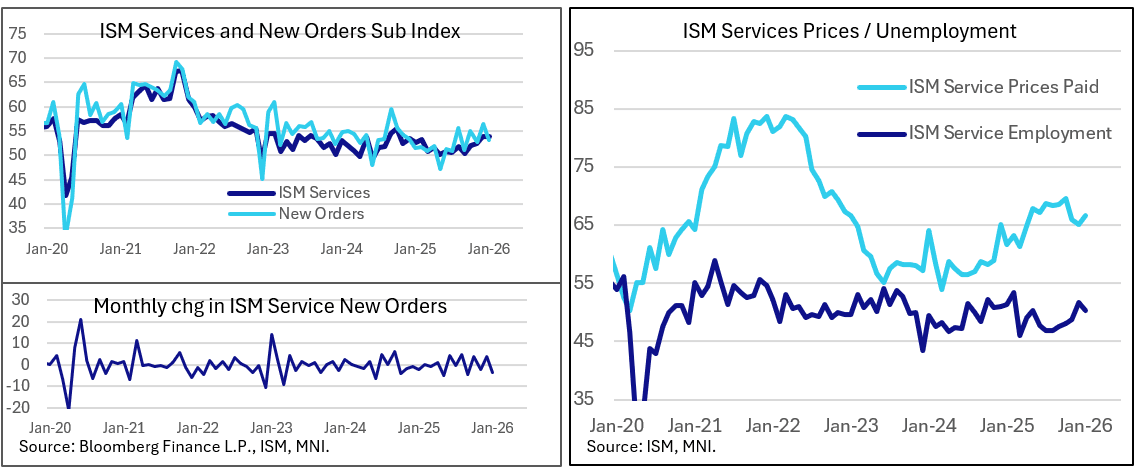

US DATA: ISM Services Opens 2026 On Firm Ground, But So Do Price Pressures

January's ISM Services report was solid overall, with some mixed dynamics beneath the surface including continued persistence in price pressures. Overall it shouldn't change perceptions of activity in the services sector, which entered 2026 on solid footing and appears to be maintaining that momentum.

- The headline PMI came in at 53.8 for a joint-15 month high. This was a steady reading vs December's 53.8, revised down from 54.4 as part of the annual seasonal adjustment revisions; it's unclear whether the consensus for a drop to 53.5 considered this revision.

- As expected, New Orders couldn't sustain December's torrid pace, falling 3.4 points to 53.1. But that is still above the average seen over the last year and bodes well for future activity.

- Similarly, Employment stumbled a little, falling to 50.3 from December's 10-month high 51.7, though that makes 2 consecutive months above 50 following 6 consecutive contractions. A cautionary note here is that just 5 industries reported better employment on net (one of which is the relatively non-cyclical Health Care & Social Assistance), with 8 reporting declines.

- New export orders disappointed at 45.0 (down 9.2 points) which marked the lowest since March 2023, after December's 15-month high. And Imports returned to contraction after one month in expansion (48.2, down 2.1 points). These categories are a little unusual in that around 40% of respondents do not participate in imports/exports or don't measure them separately from overall orders, though clearly there remains trade-related strain in the industry.

- Prices Paid rose 1.5 points to 66.6 for a 3-month high with 17 industries reporting higher prices (and non reporting declines), suggesting that inflationary pressures in the sector persist. We also saw an uptick in this category in the ISM Manufacturing report, which lends a cautionary tone to the week's data.

- On the unambiguously positive side, we took note of the jump in Business Activity, by 2.2 points to a 15-month high 57.4.

- Elsewhere, Inventories fell below 50 after 2 months of expansion, at 45.1 (down 9.1 points), with Inventory Sentiment in "too high" territory for the 33rd consecutive month. Supplier Deliveries picked up 2.4 points to 54.2, a 14th month indicating slower deliveries and thus boosting the overall PMI per the ISM's methodology.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UN: Sec-Gen Raises Concern About Precedent Set By US' Venezuela Operation

In a statement to a meeting of the UN Security Council, Secretary-General Antonio Guterres says that the UN is "concerned about the possible intensification of instability in Venezuela" following the US operation that saw President Nicolas Maduro captured and transported to the US to face narco-trafficking charges. Guterres says there are also concerns regarding the precedent the operation may set for how relations among states are conducted, and whether the op respected the rules of international law.

- Guterres calls on all Venezuelan actors to "engage in an inclusive, democratic dialogue", and says the UN is ready to support all efforts aimed at assisting Venezuelans in finding a peaceful way forward.

- It is unclear if a resolution will be put to a vote to condemn the US's actions in Venezuela. Even if a resolution is passed, it is unlikely to have any impact on the future actions of the Trump administration vis-a-vis the immediate control of Venezuela, and its interactions with the newly inaugurated interim president, Delcy Rodriguez.

- The precedent set by the US's actions are being closely followed in other NATO states following President Trump's comments after the Maduro operation regarding future control of Greenland. Danish PM Mette Frederiksen said a short time ago that she believes Trump is "serious about wanting to take over Greenland", but that both Denmark and Greenland have said no. Adds that any US attempt to seize Greenland will see "everything stop" with regards to NATO cooperation.

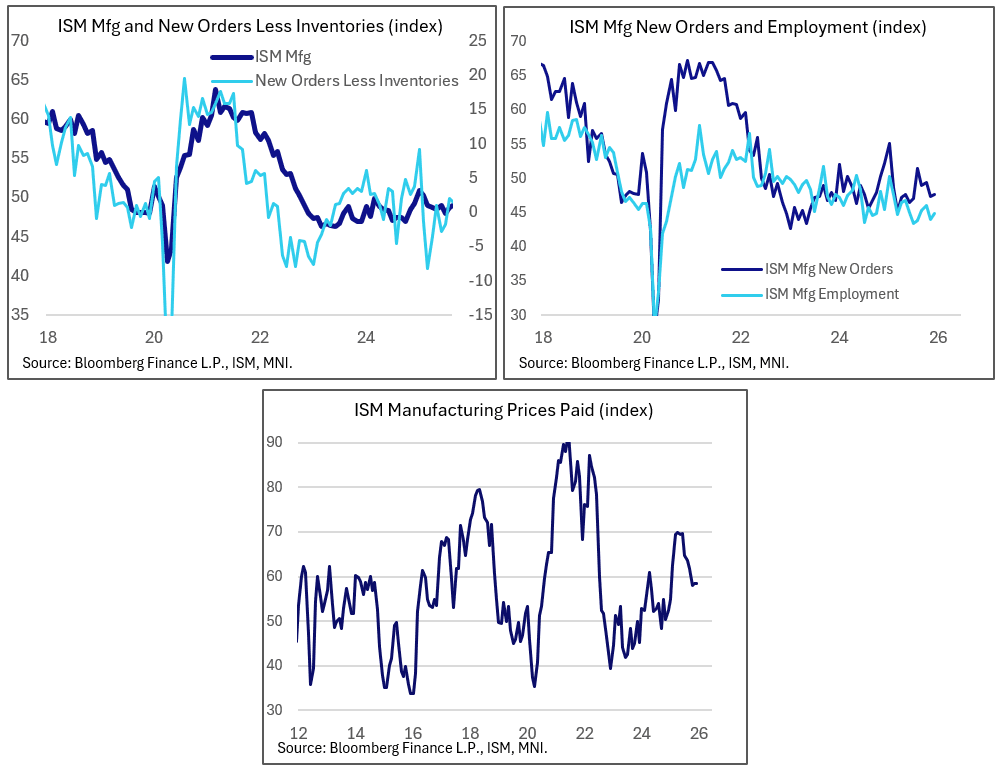

US DATA: Tariff Concerns Abound In Limp ISM Manufacturing Activity Data

The ISM Manufacturing report for December was relatively steady vs November and in line with broad expectations, quietly falling to a 14-month low (Oct 2024) in showing continued softness in activity with price pressures steadying at a high level.

- The headline PMI reading was a little weaker than the consensus of analysts had anticipated at 47.9 (48.4 expected, 48.2 prior), though MNI had signaled that some deterioration should be unsurprising given poor regional Fed surveys and a dip in the S&P PMI for the month.

- This marked a 10th consecutive sub-50 reading indicating contraction in sector activity, and the sub-indices pointed to softer production but a potential bright spot in improved demand vs November. Reflecting the fairly flat headline reading, the sub-indices were relatively steady: New Orders +0.3 to 47.7, Production -0.4 to 51.0. Two standouts were backlogs up 1.8 to 45.8 with inventories down 3.7 to 45.2.

- In trade, the volatile imports reading was down 4.3 points to a 7-month low 44.6 due to "Tariff-related pricing pressures" per the report, but conversely export orders were up 0.6 to a 9-month best 46.9 despite "softer international orders tied to tariffs and ongoing uncertainty around U.S. economic policy".

- Attention as always was on the employment category which ticked up 0.9 to 44.9, suggesting a slower pace of contraction in manufacturing jobs. That said "For every comment on hiring, there were three on reducing head counts. Companies continued to focus on accelerating staff reductions due to uncertain near- to mid-term demand. The main head-count management strategies remain layoffs and not filling open positions."

- Additionally prices paid were steady at 58.5, defying consensus eyeing an uptick (58.7 expected, 58.5 prior) though again this suggests continued elevated pressures due in large part to tariff policy ("The Prices Index reading continues to be driven by increases in steel and aluminum prices that impact the entire value chain, as well as tariffs applied to many imported goods.") The lack of an increase is consistent with regional Fed indices and the S&P PMI which showed a pullback in inflationary pressures albeit at high levels.

- The anecdotal comments from various respondents were universally negative, with many citing soft demand and price pressures due to tariffs (that aren't able to be fully passed on, impacting margins). On New Orders, "For every positive panelist comment about new orders, 1.3 comments indicated concern about near-term demand, driven by tariff costs and other uncertainties."

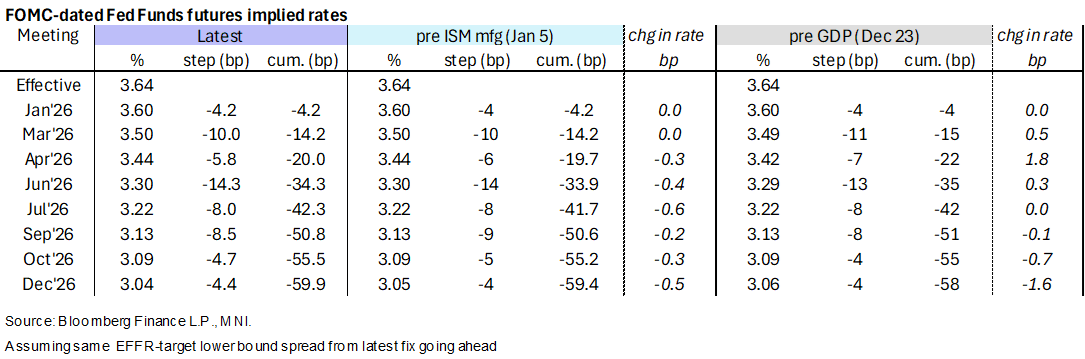

STIR: Marginally Dovish Impact From Small ISM Mfg Miss

- US rates have seen little net impact from the ISM manufacturing report for Dec, continuing to shy away from fully pricing a next FOMC cut with the April meeting and instead still comfortably pricing a next move in June under the new Fed chair.

- FF cumulative cuts from 3.64% effective: 4bp Jan, 14bp Mar, 20bp Apr, 34.5bp Jun, 51bp Sep and 60bp Dec.

- SOFR futures have mostly firmed 1 tick since the release, currently ranging from -0.0075 (Z5) to +0.035 (Z7) from Friday’s close when looking out to end-2027. The latter is back to levels at the start of the US session whilst the terminal implied yield of 3.10% (Z6) remains within some recent narrow ranges.

- Today’s moves have been dominated by broad FI gains following the US capturing of Maduro before a short-lived paring of those gains from a combination of corporate issuance and Kashkari (’26 voter) sounding patient on the prospect of further rate cuts on CNBC.

- The ISM manufacturing index disappointed slightly although wasn’t a huge surprise considering some softer alternative indicators, whilst the prices paid index was unchanged and new orders saw a very small improvement at still contractionary levels.