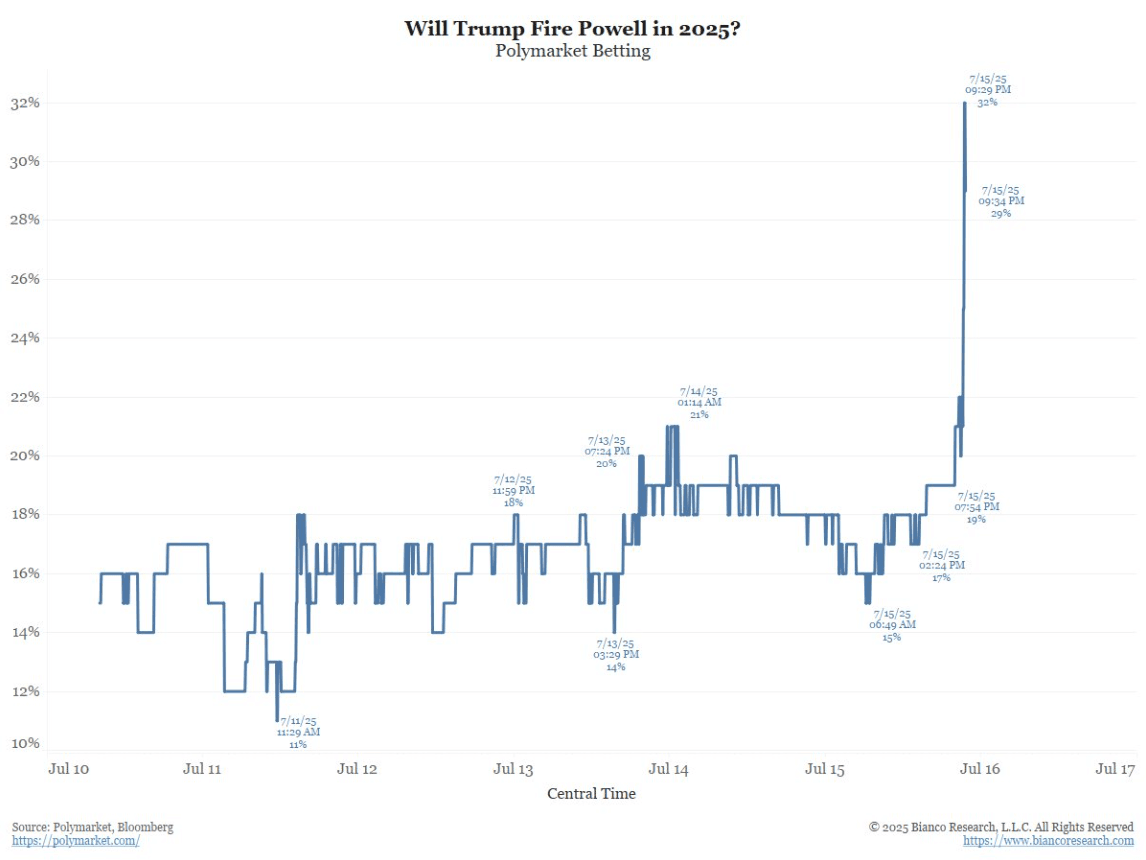

US: Is The Fed Chair Being Sacked Underpriced ?

A post on X from Congresswoman Anna Paulina Luna alluding to the imminent firing of Jerome Powell is adding fire to the situation. For the moment the market seems to be brushing this off and should it materialise is massively underpriced. What if the only way Trump can actually get yields lower is to replace the Fed Chair with someone who is willing to cut, and cut a lot. Should this happen it would further erode trust in US Assets and the USD would freefall once more. You would think the knee-jerk reaction would be higher in the Long-End but should an Uber Dove be appointed this could drive yields lower albeit with the front-end leading the charge and the curve steepening further.

- Rep. Anna Paulina Luna on X: “Jerome Powell is going to be fired. Firing is imminent.”

- (Bloomberg) -- “I think it sort of is,” President Donald Trump says when asked whether the renovations at the central bank were a fireable offense for Federal Reserve Chair Jerome Powell.

- Jim Bianco - “The betting market of “Will Trump fire Powell in 2025” has responded and the uptrend continues. See Graph Below.

Fig 1: Polymarket Betting - Will Trump Fire Powell In 2025

Source - @biancoresearch/Polymarket/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOJ: MNI BoJ Preview - June 2025: Focus On Future Rate Hikes & QT

EXECUTIVE SUMMARY

- The Bank of Japan (BoJ) is set to hold its Monetary Policy Meeting (MPM) on June 16–17, and although no changes are expected to the current policy rate of 0.50%, the meeting may still prove impactful for both domestic and global markets.

- The key area of interest will be Governor Kazuo Ueda’s post-meeting press conference. Investors will closely examine his comments for any signals on the timing and likelihood of future rate hikes.

- If the BoJ begins to hint at stronger underlying inflationary trends or shows greater optimism about the economy, it could stoke expectations of a rate hike in the autumn.

- The second area of market focus is on the BoJ’s Japanese Government Bond (JGB) purchase program.

- Currently, the BoJ is reducing its JGB purchases by ¥0.4 trillion per quarter, aiming for a pace of ¥2.9 trillion. This reduction is expected to continue without change through the first quarter of 2026. The real uncertainty lies in what happens beyond that point. Most analysts anticipate the BoJ will continue reducing purchases, but the pace is up for debate.

- Market expectations suggest a slower pace of reductions during fiscal year 2026. If the BoJ chooses to maintain the current pace of ¥400 billion reductions per quarter in FY2026, this would be interpreted as a mildly hawkish move.

- Full preview here:

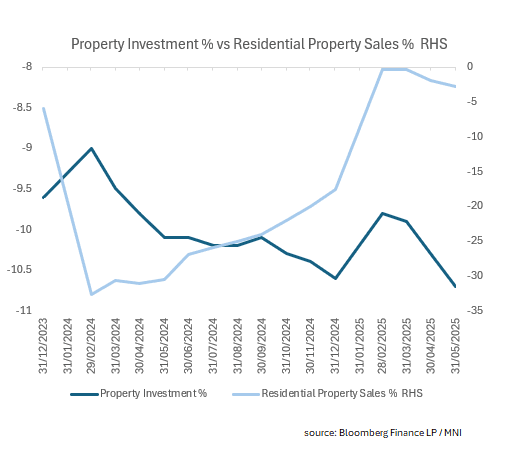

CHINA: Property Data Turns Down Again

- As new and used home prices (ex Shanghai) continue in their deflationary spiral, other data is showing signs of turning downwards after periods of improvement.

- China's Residential Property Sales and Property Investment YTD turned down again in May.

- Residential Property sales YTD YoY fell -2.8% (from -1.9% in April), the worst result this year.

- Property Investment YTD YoY declined -10.7% in May, from -10.3% in April and the worst result in over five years.

- There has been speculation as to the need for further policy stimulus with bond markets rallying post the data release.

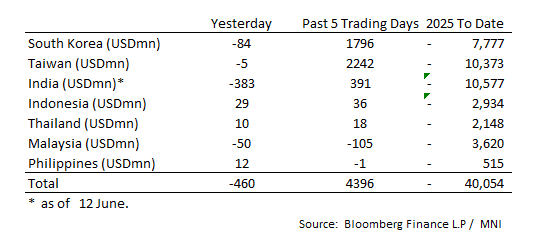

ASIA STOCKS: Large Outflow for India Thursday

Large inflows across major markets was the theme last week, despite India seeing large outflow on Thursday and flows tapering off on Friday for other markets.

- South Korea: Recorded outflows of -$84m Friday, bringing the 5-day total to +$1,796m. 2025 to date flows are -$7,777. The 5-day average is +$359m, the 20-day average is +$184m and the 100-day average of -$85m.

- Taiwan: Had outflows of -$5m as of Friday, with total inflows of +$2,242 m over the past 5 days. YTD flows are negative at -$10,373. The 5-day average is +$448m, the 20-day average of +$63m and the 100-day average of -$112m.

- India: Had outflows of -$383m as of the 12th, with total inflows of +$391m over the past 5 days. YTD flows are negative -$10,577m. The 5-day average is +$78m, the 20-day average of -$24m and the 100-day average of -$86m.

- Indonesia: Had inflows of +$29m Friday, with total inflows of +$36m over the prior five days. YTD flows are negative -$2,934m. The 5-day average is +$7m, the 20-day average +$14m and the 100-day average -$29m.

- Thailand: Recorded inflows of +$10m as of Friday, with inflows totaling +$18m over the past 5 days. YTD flows are negative at -$2,148m. The 5-day average is +$4m, the 20-day average of -$23m and the 100-day average of -$21m.

- Malaysia: Recorded outflows of -$50m as of Friday, totaling -$105m over the past 5 days. YTD flows are negative at -$3,620m. The 5-day average is -$24m, the 20-day average of -$28m and the 100-day average of -$24m.

- Philippines: Saw inflows of +$12m yesterday, with net outflows of -$1m over the past 5 days. YTD flows are negative at -$515m. The 5-day average is $0m, the 20-day average of -$15m the 100-day average of -$5m.