OIL: Iran Headlines Drive Crude Lower

Oil prices are down sharply at the start of today’s APAC trading after NBC reported that a top Iranian official said that the country would “commit to never making nuclear weapons” and “getting rid of its stockpiles of highly-enriched Uranium” in exchange for reduced sanctions. This would add to global oil supplies after OPEC announced a +400kbd increase from June.

- WTI is currently down 1.5% to $62.18 but off the intraday low of $61.86 after falling 1.2% on Wednesday. The benchmark remains higher on the month up around 7% driven by progress on a US-China trade deal. The downtrend continues with the bear trigger at $54.67. A clear break of $63.55, 50-day EMA, would open the possibility of a reversal.

- Brent has fallen another 1.3% to $65.22/bbl today after 1.2% yesterday. The bear trigger is at $59.00, while key resistance is at $66.59, 50-day EMA.

- EIA reported that US crude stocks rose 3.45mn barrels last week, larger than expected, but products continued to decline with distillate down 3.2mn and gasoline 1.0mn signalling still solid demand. Refining utilisation increased 1.2pp to 90.2%, slightly below the same time last year.

- Also on the supply side, OPEC’s April report showed that it had increased output by 25kbd last month less than the planned 138kbd. Further rises in production will be considered at the group’s June 1 meeting. The IEA report is released later today.

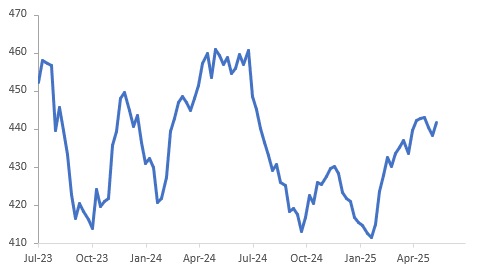

US EIA crude stocks ex SPR

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Outflows Resume Across the Region

Constant outflows continue to be the thematic we see as we watch the equity flows across the major markets.

- South Korea: Recorded outflows of -$188m as of yesterday, bringing the 5-day total to -$1,584m. 2025 to date flows are -$11,666m. The 5-day average is -$317m, the 20-day average is -$323m and the 100-day average of -$152m.

- Taiwan: Had outflows of -$642m as of yesterday, with total outflows of -$1,402m over the past 5 days. YTD flows are negative at -$18,358. The 5-day average is --$280m, the 20-day average of -$247m and the 100-day average of -$249m.

- India: Had outflows of -$518m as of the 9th, with total outflows of -$2,815m over the past 5 days. YTD flows are negative -$16,476m. The 5-day average is -$563m, the 20-day average of -$44m and the 100-day average of -$150m.

- Indonesia: Had outflows of -$138m as of yesterday, with total outflows of -$488m over the prior five days. YTD flows are negative -$2,318m. The 5-day average is -$98m, the 20-day average -$50m and the 100-day average -$37m

- Thailand: Recorded outflows of -$34m as of the 11th, outflows totaling -$250m over the past 5 days. YTD flows are negative at -$1,396m. The 5-day average is -$50m, the 20-day average of -$25m the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$18m as of yesterday, totaling -$222m over the past 5 days. YTD flows are negative at -$2,796m. The 5-day average is -$44m, the 20-day average of -$60m the 100-day average of -$40m.

- Philippines: Saw inflows of +$3m as of yesterday, with net outflows of -$62m over the past 5 days. YTD flows are negative at -$290m. The 5-day average is -$12m, the 20-day average of -$3m the 100-day average of -$6m.

AUD: AUD Bounce Takes A Pause

The AUD buying over the last few days seems to have slowed, topping out in both the London and New York session at levels around 0.6340. US equities continued to bounce with risk stabilising. The CFTC data shows Asset managers were active last week paring back their shorts aggressively. A problem that has not gone away though is the US-China relationship and how further tensions could impact the Yuan. The AUD will continue to be seen as a proxy to China so it is worth keeping an eye on how the PBOC intends to let this play out.

- EUR/AUD - Overnight range 1.7910 - 1.8087, further consolidation as we approach a long weekend. Asia opens under pressure breaking the overnight lows and is currently dealing around 1.7900.

- GBP/AUD - Overnight range 2.0766 - 2.0920, GBP/AUD continues to consolidate having found some support back toward 2.06 as the GBP played catch up to the move lower in the USD.

- AUD/JPY - Overnight range 89.91 - 90.78, everyone's favourite way to express risk aversion in FX finds dips shallow as the pair consolidates. The 92/94 area is very strong resistance but the weekly shadow and rejection of the pivotal 85.00 area will make shorts nervous. While markets remain in turmoil and uncertainty high the JPY crosses should continue to find sellers on bounces.

- AUD/NZD - Overnight range 1.0741 - 1.0779, the cross is dealing in Asia around 1.0760 with very little direction. Resistance towards 1.0900/1.1000 should be tough first up, look for some consolidation after stale longs have been stopped out last week. Note on Thursday we get both NZ CPI and Australian jobs data.

Fig 1: AUD/JPY Spot

AUSSIE BONDS: Richer After A Solid Session For US Tsys, RBA Minutes Due

ACGBs (YM +1.0 & XM +3.0) are slightly stronger after US tsys opened in today’s Asia-Pac session little changed.

- Yesterday, risk stabilised, and US yields benefited as money was put back to work.

- The US 10-year yield is dealing in the Asia-Pac session around 4.3815%, after closing yesterday at 4.3739%.

- The US market has been forced to reduce the number of cuts it was expecting as the Fed has been consistent in saying it was worried about inflation due to the President's policies. Bostic spoke this morning: "Right now range of possible outcomes has multiplied. Inflation is still much higher than target. Not in a position to boldly move in any direction, need more clarity." (via RTRS/BBG)

- Today, the local calendar will see the release of the RBA Minutes for the April Meeting.

- Cash ACGBs are 1-3bps richer with the AU-US 10-year yield differential at -1bp.

- Swap rates are also lower with EFPs little changed.

- The bills strip has bull-flattened, with pricing flat to +4.

- RBA-dated OIS pricing is flat to 3bps softer across meetings today. A 50bp rate cut in May is given a 40% probability, with a cumulative 120bps of easing priced by year-end.