SWEDEN: Insufficient Demand Drives Industrial Capacity Underutilisation In Q1

May-21 07:55

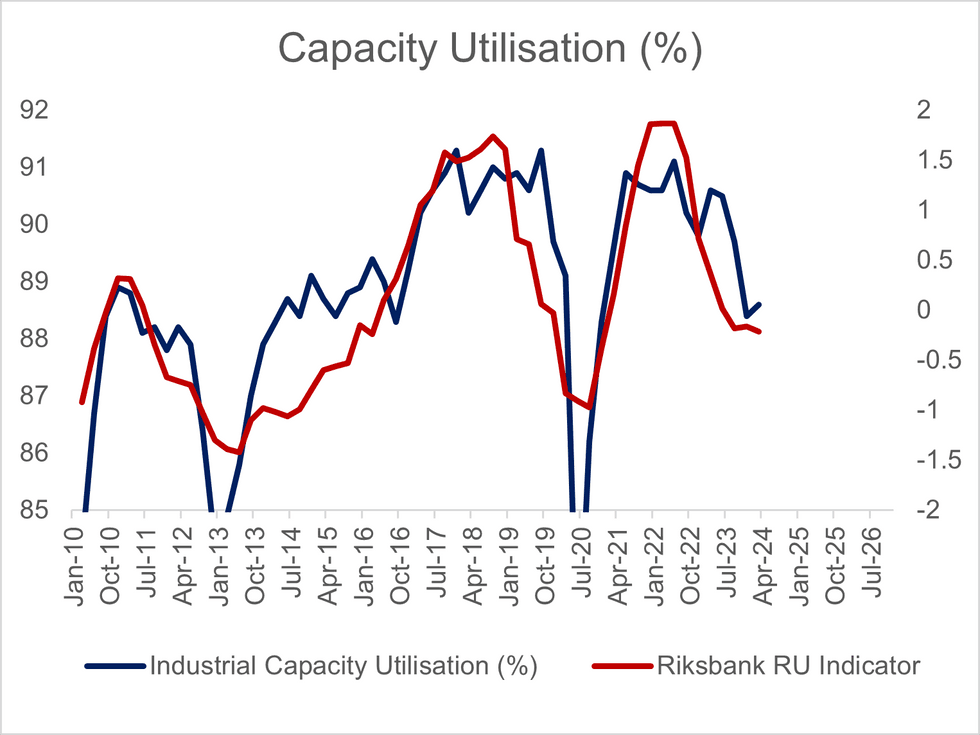

Swedish first quarter industrial capacity utilisation was 88.6% (vs 88.4% in Q4 ’23, 90.6% in Q1 ’23). The 2000-2019 average for this series is 88.4%.

- Of those firms reporting less than 100% capacity utilisation, 60% assigned “insufficient demand” as the primary reason, up from 53% in Q1 ’23.

- 22% of firms reported “production disruptions” as the primary reason for their underutilisation. Only 5% of firms assigned “lack of employees” as their main factor.

- The Riksbank’s own measure of resource utilisation showed similar declines through 2023. In Q1, this indicator printed was -0.21 (i.e. indicating underutilisation).

- From the March monetary policy report: “As GDP growth increases towards the end of 2024, resource utilisation is expected to gradually return to balance”.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Tsys Hold Modest Gains, Fed Enters Policy Blackout Tonight

Apr-19 19:31

- Treasury futures have been trading sideways in modestly positive territory since midmorning Friday - a rather quiet end to a hectic week, the Federal Reserve entering their self-imposed media Blackout regarding policy at midnight tonight.

- Treasuries surged higher on heavy volumes early overnight (TYM4>1.13M by the open) after Israel launched targeted attack against Iran. Safe haven support in rates faded receded as both sides downplayed the action.

- Safe haven bid pushed Jun'24 10Y futures to 108-22.5 high late Thursday evening, while the contract currently trades 107-28.5 (+6) after the bell - well above initial technical support of 107-13+ Low Apr 16. 10Y yield 4.6125% -.0181, curves mildly flatter: 2s10s -.485 -36.050.

- Projected rate cut pricing held largely steady vs. late Thursday lvls: May 2024 -2.6% w/ cumulative -0.6bp at 5.322%; June 2024 at -13.5% w/ cumulative rate cut -4.5bp at 5.283%. July'24 cumulative at 12.1bp, Sep'24 cumulative -23bp.

- Look ahead: economic data picks up next Tuesday with regional manufacturing data from Philly and Richmond Fed, S&P PMIs and New Home Sales.

AUDUSD TECHS: Southbound

Apr-19 19:30

- RES 4: 0.6644 High Apr 9

- RES 3: 0.6537 50-day EMA

- RES 2: 0.6507 20-day EMA

- RES 1: 0.6481 Low Apr 1 and a recent breakout level

- PRICE: 0.6424 @ 16:39 BST Apr 19

- SUP 1: 0.6363 Low Apr 19

- SUP 2: 0.6339 Low Nov 10 and a key support

- SUP 3: 0.6315 Low Oct 31 ‘23

- SUP 4: 0.6270 Low Oct 26 ‘23 and a key support

AUDUSD remains vulnerable and the pair traded to a fresh trend low Friday. Key support at 0.6443, the Feb 13 low, has recently been cleared highlighting an important technical breach that has confirmed a resumption of the downtrend that started late December last year. Scope is seen for an extension towards 0.6339, the Nov 10 ‘23 low. Firm resistance is seen at 0.6537, the 50-day EMA. Short-term gains are considered corrective.

CANADA: CIBC Caution On Wednesday’s Retail Sales

Apr-19 19:29

- CIBC expect that nominal retail sales increased a “sluggish” 0.1% M/M in February, in line with the advance estimate.

- “However, excluding autos, sales could have fallen by 0.2% (cons 0.0), following a jump in January that was likely boosted by milder than normal weather.”

- They expect per-capita spending to look worse as households curtail discretionary spending with higher mortgage payments and the rising unemployment rate biting.

- “Goods prices fell in February, which means that retail sales will likely show modest growth in volume terms.”

- For Q1, they see “relatively healthy” goods consumption, “but that reflects a boost from activity amidst mild winter weather.” They see per-capita real retail sales roughly -1.5% Y/Y “and that weakness leaves the door open for a June cut from the BoC.”