STIR: Initial Hawkish Data Reaction In Fed Pricing Unwound

Initial hawkish Fed pricing move on the firmer-than-expected retail sales, lower than-expected weekly jobless claims and firmer-than-expected Philly Fed readings pared, with the retrace seemingly driven by the softer-than-expected import price data (which was accompanied by negative revisions).

- FOMC-dated OIS essentially flat vs. pre-release levels as a result, showing 1bp of easing for this month, 14bp through September, 27.5bp through October and 44.5bp through December. No major multi-week range breaks seen given the second-round dovish move.

- SOFR implied terminal rate pricing into 3.22% vs, 3.24% pre-data.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: US REDBOOK: JUN STORE SALES +5.0% V YR AGO MO

- MNI: US REDBOOK: JUN STORE SALES +5.0% V YR AGO MO

- US REDBOOK: STORE SALES +5.2% WK ENDED JUN 14 V YR AGO WK

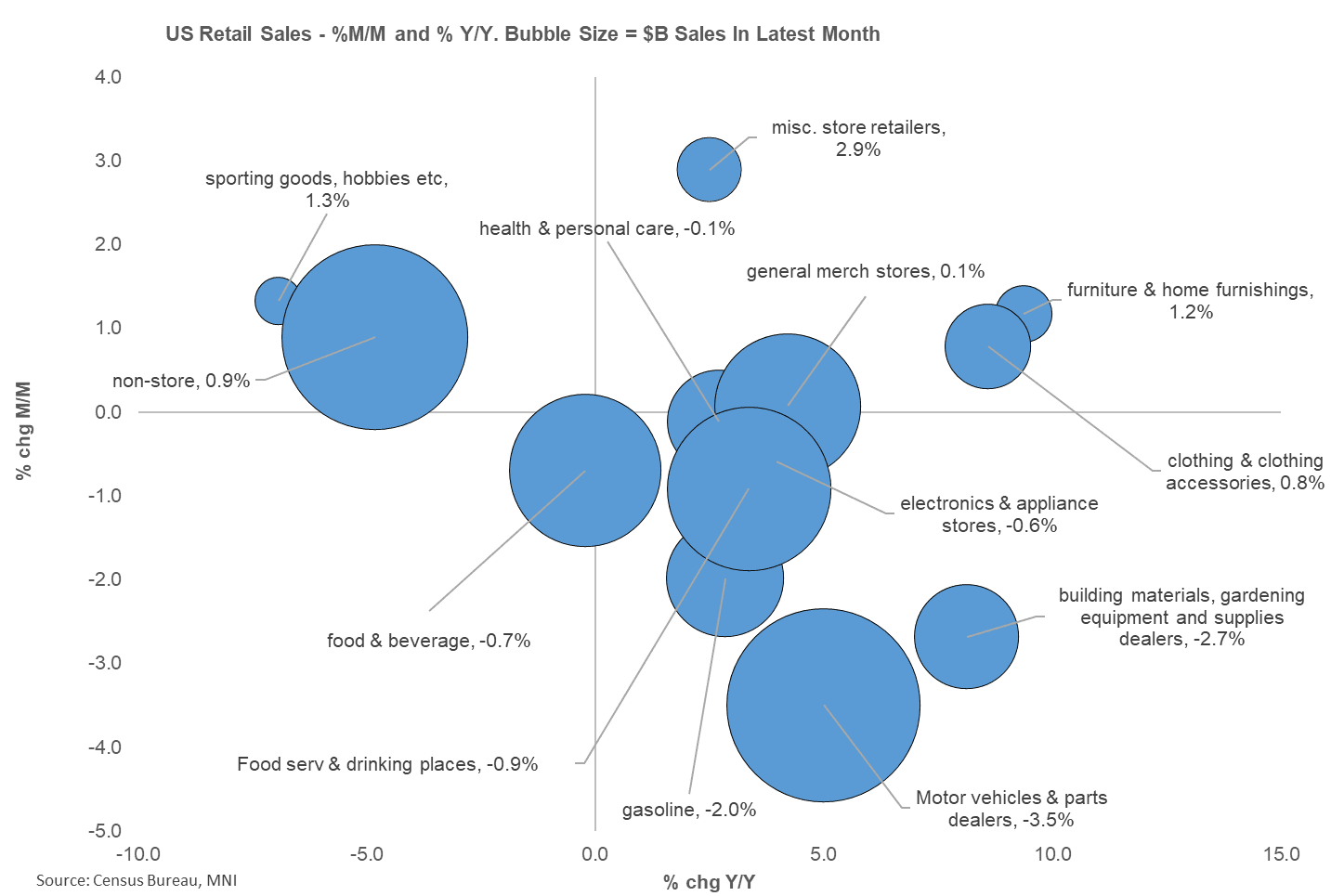

US DATA: Control Group Flatters Mixed Retail Sales Report

May saw the biggest month-to-month drop in retail sales (-0.91% M/M SA unrounded, vs -0.6% consensus and -0.1% April rev from +0.1%) since March 2023, with ex-autos/gas weaker than expected (-0.1% vs +0.3%) and surprisingly decelerating from April (0.1%, rev down from 0.2%). Likewise, ex-auto sales unexpectedly fell, by 0.3% (+0.2% expected, 0.0% prior rev down from 0.1%).

- Bucking the trend was the closely-watched Control Group, which rose more than expected at 0.4% (0.3% consensus), with prior revised up (April -0.1%, from -0.2%).

- The reason for the Control Group "beat" was the poor performance of several major categories of retail sales that aren't included in Control: vehicle sales, which dropped the fastest in 11 months at 3.9% M/M in line with expectations for a sharp decline (-0.6% prior); gasoline sales, which fell 2.0% (-0.7% prior) also as expected given 2.6% CPI deflation in this category; building materials/gardening sales, which fell 2.7% M/M for the biggest decline in 16 months (0.3% prior); and food services and drinking places, whose fall of 0.9% (biggest drop in 27 months) looks to have been unexpected, versus strength in the prior two months.

- The pullback in restaurant sales is somewhat concerning from a discretionary spending perspective, though of course all of the individual series are volatile. But the Control Group performance flatters the broader report in terms of gauging the health of consumption. Motor Vehicles/Parts and Food Services/Drinking Places, plus Food/Beverage stores (-0.7%) are three of the top four categories of retail sales by size making up 60% of the total, and each contracted.

- The standout was on the upside was non-store retail, the second-largest category, which impressed with 0.9% M/M gains; the smaller categories of clothing (+0.8%), miscellaneous scores (+2.9%), furniture (+1.2%) sporting goods (+1.3%) which were all arguably tariff-impacted categories saw gains albeit largely in a rebound from a poor month or two prior, though electronics stores (-0.6%) weakened.

NORGES BANK: MNI Norges Bank Preview: June 2025 - Gearing Up for the H2 Cut

FOR THE FULL PUBLICATION PLEASE CLICK HERE

EXECUTIVE SUMMARY:

- Norges Bank is firmly expected to hold rates at 4.50% on Thursday, at a quarterly meeting which includes an updated MPR and rate path projection. We expect guidance that the policy rate “will most likely be reduced in the course of 2025” will remain unchanged, with a risk of firmer guidance towards a September cut.

- Developments since the March meeting should warrant a modest downward revision to the rate path, but we still expect the June iteration to be consistent with two cuts this year. Over the last three months, spot inflation pressures have been lower than expected and energy prices have softened (assuming the latest spike on Israel/Iran tensions has come too late to impact the June forecasts). These factors should pull down the June rate path.

- However, mainland economic signals portray an economy that is coping relatively well with rates at 4.50%. This should limit the downward rate path revision and allow the board to guide for future easing without feeling pressured to commit to a specific meeting. Norges Bank were forced to abandon long-standing guidance for a 25bp cut at the March decision, owing to an unexpected uptick in domestic inflation pressures. This may also deter the Board from including meeting-specific guidance this week. In any case, a rate path that is consistent with 2x25bp cuts in H2 should be well understood by markets as being consistent with cuts in September and December, given Norges Bank’s historical aversion from meaningful policy pivots at non-MPR meetings.