HYBRIDS: Hybrids: Week in Review

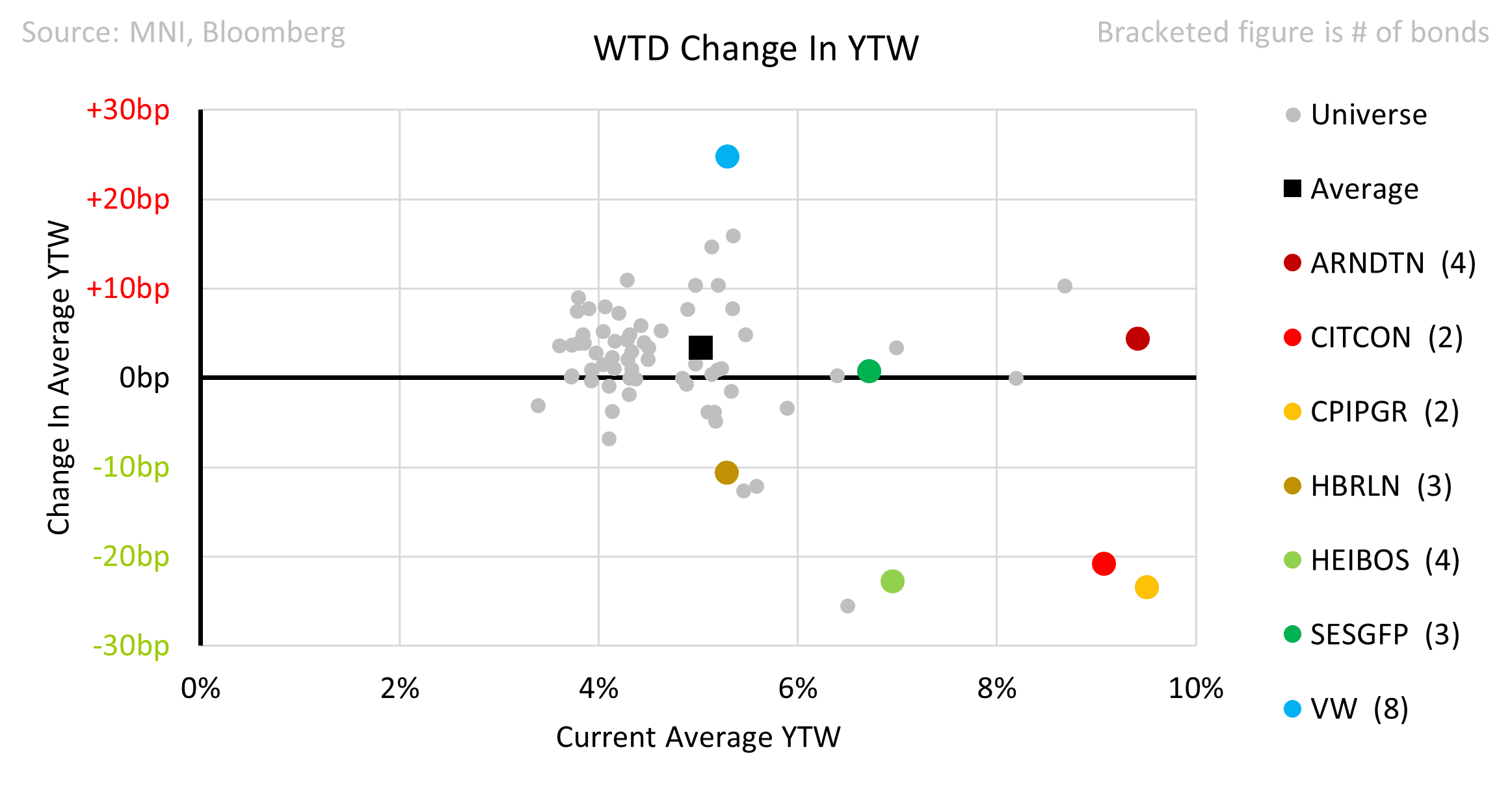

- Mobico – what a difference a week makes. Perps are closing the week 9.25 pts below the pre-US Bus sale level. Bonds are now yielding 10.6% to the Second Reset Date in Feb ’31. We are hearing that some senior bond holders are considering challenging the US Bus sale as an Event of Default though with the deal due to close in Q3 it will be a while before anything develops here. Perps do not have the same EOD language.

- SES was moved to Negative Outlook by Fitch. Bonds were steady. The equity has been drifting lower from March highs.

- Longer dated VW Call29 and Call31 were just over 1pt lower on the week. The senior curve was +8bps wider on average having reported on 29th.

- Harbour Energy bought a €900m NC5.25 @6.125% We thought that this was right on FV. With little upside bonds gave up 1pt in secondary. OPEC is meeting over the weekend which saw Brent fall on Friday and the equity give back some gains. TTF futures are up 4% on the week which may help. The tender on the HBRLN 2.4985% Call26 closes 8th May which may see some cash come back into the name.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: J.P.Morgan Note That Most Positioning Indicators Screen Long

Ahead of the “Liberation Day” announcement J.P.Morgan note that their “Treasury client survey index has retraced near multi-year highs. This lengthening in duration positioning is consistent with other position indicators we follow: CTAs and core bonds funds have also added to duration positioning over the past month, although macro hedge funds appear to have reduced exposure, with our empirical beta now showing close to flat positioning for that cohort”.

EUROPEAN FISCAL: French YTD Deficit Sees A Second Month Tracking Below 2024

The central government cash balance saw a budget deficit of E40.3bln in the first two months of the year, an improvement from E44.0bln in Jan-Feb 2024 and below the equivalent average of E41.7bln between 2019-25.

- The E40.3bln deficit equates to 29% of the E139bln central government deficit forecast for 2025 (worth circa 4.6% GDP), similar to February 2024's realised 28% of total 2024 deficit and 29% in 2023 but above the 25% seen in 2022.

- The return to what was closer to a more typical two-month deficit after a particularly good start to the year (E17.3bn in Jan vs E25.7bn in Jan 2024) came in large part from a one-off shift in intervention expenditure across Jan-Feb 2025 vs full payment solely in January last year.

- More broadly, two-month expenditure summed to E77.8bln (vs E75.1bln in Feb 2024) whilst revenue increased by a greater extent to E45.2bln (from E40.2bln in Feb 2024).

- The year-on-year increase in two-month revenue was due to a rise in tax receipts (E43.5bln from E38.6bln in Feb 2024), whilst non-tax revenues were again stable (unchanged at E1.1bln).

- All key sub-components of tax revenues increased in YTD Y/Y terms, in particular other tax revenues at E10.1bln (vs E7.2bln in Feb 2024).

- Intervention expenditure summed to E19.0bln (vs E19.3bln to Feb 2024).

- Capital expenditure also rose to E5.1bln from E3.7bln in February 2024 likely due to the "increase in investment expenditures by the Ministry of the Armed Forces" as noted in the press release.

- A reminder that translation to a general government basis is difficult so early in the fiscal year, especially given ongoing negotiations around pension reform. Last week, Insee published the total 2024 general government budget deficit which came in at 5.8% of GDP - three tenths below the Finance Ministry's latest projections, though Budget Minister Montchalin had suggested the deficit could come in “a little bit lower” than 6%.

- Note also the prospect of increased French defense spending - and crucially how this increase is funded presents a risk to the general government deficit target of 5.4% of GDP for 2025.

US DATA: Strength In Factory Orders Reinforces Solid Pre-Tariff Narrative

New orders for manufactured goods ("factory orders") were a little stronger than expected in February, with the headline reading of 0.6% M/M (0.5% expected, 1.8% prior upwardly revised from 1.7%). The 3M/3M annualized rate of orders growth picked up to 1.6%, implying improved momentum after 2 consecutive negative monthly readings.

- Durable goods were minimally revised in the final reading: headline orders were upped 0.1pp to 1.0% M/M, but orders ex-transport (0.7%), and core capital goods orders (-0.2%) and shipments (0.8%) were all unrevised.

- As we noted following the durable goods report - in which orders greatly exceeded expectations - manufacturing data for February was suggestive of strong "hard" data for manufacturing in Q1. The factory orders data further supports this narrative.

- Incoming data since then - including a very weak ISM Manufacturing report for March - further supports the other part of the narrative however, which is that recent manufacturing strength reflects front-running the impact of tariffs, implying a dropoff in demand later in the year that may already be reflected by slowing core capital goods orders in February.