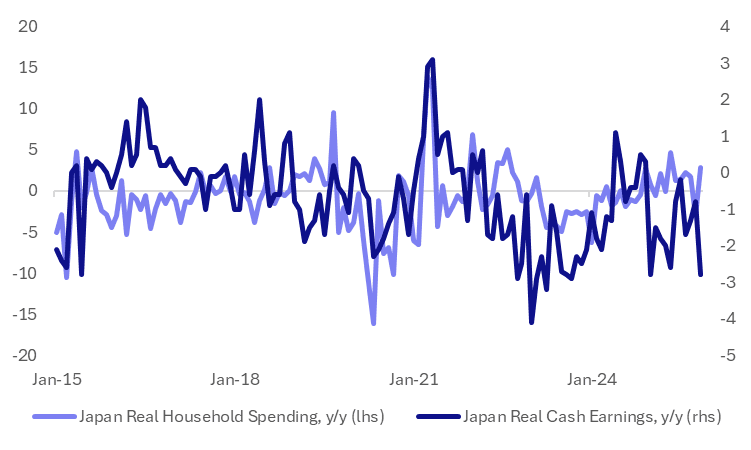

JAPAN DATA: Household Spending Jumps In Nov, Outpacing Weaker Earnings

Japan real household spending rose 2.9%y/y in Nov, well above the -1.0% forecast and -3.0% Oct outcome. In m/m terms spending was up 6.2%, the strongest monthly rise since 2021. The chart below updates real spending y/y versus real labour earnings, also in y/y terms. The two series tend to follow each other from a trend standpoint, but for much of 2025, spending outcomes were running ahead of the real cash earnings measure. This divergence widened in Nov. Whilst yesterday's labour earnings data was disappointing, the BoJ regional economic report still pointed to positive wage momentum for 2026 - via our policy team: many branch managers reported expectations for sustained pay increases, with several pointing to wage growth at levels similar to or higher than those seen in 2025.

- In terms of the detail on today's spending update, food spending rose 0.9%y/y from -1.1% in Oct. Spending on transport, communication also surged to 20.4%y/y from -9.2%.

Fig 1: Japan Real Household Spending & Labour Earnings Y/Y

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: ACGB Dec-30 Auction Result 2025

The AOFM sells A$1000mn of the 4.75% 21 April 2027 bond, #TB136:

- Average Yield (%): 4.3532 (prev. 3.5254)

- High Yield (%): 4.3550 (prev. 3.5275)

- Bid/Cover: 2.6630x (prev. 2.7625x)

- Allotted at Highest Accepted Yld as % of Bid at that Yld (%): 69.9 (prev. 86.4)

- Bidders 36 (prev. 32), successful 16 (prev. 13), allocated in full 7 (prev. 7)

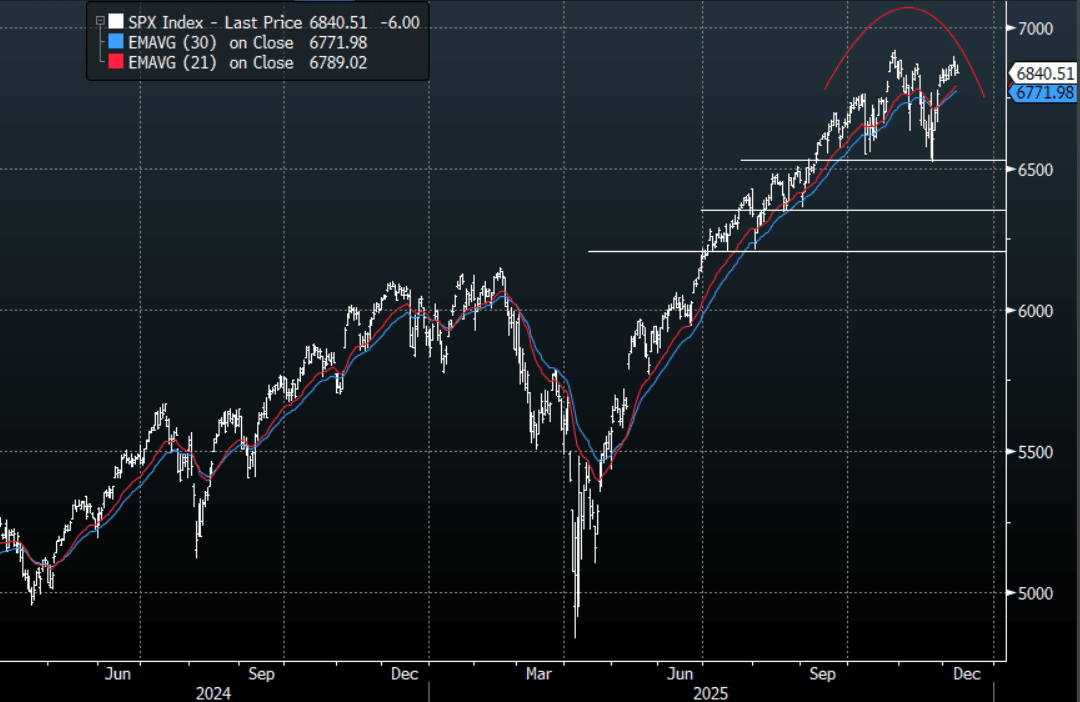

US STOCKS: S&P(ESZ5) - Treads Water Ahead Of FOMC

The S&P(ESZ5) overnight range was 6844.00 - 6872.75, SPX closed -0.09%, Asia is currently trading around 6846. Risk has traded on the soft side overnight as treasuries continue to be sold as we approach the FOMC. This morning futures have opened a little lower, E-minis(S&P) -0.05%, NQZ5 -0.10%. On the day, all eyes will now be turning toward the FOMC, the market is hoping for confirmation of more cuts, the risk is a hawkish Fed. I suspect we tread water on a 6800 handle until then.

- The FOMC tomorrow morning will be important with the market pricing in rate cuts, how many dissenters are needed to put a dent in this bullish view ?

- Andreas Steno Larsen on X: “I remain convinced that 2026 will bring a significant expansion in broad money. A shift is underway from the Fed toward “private channels”

- The S&P 500 Index Average True Range(ATR) for the last 10 Trading days: 55 Points

Fig 1: S&P 500 Index Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

MNI: JAPAN NOV CORP GOODS PRICE INDEX +2.7% Y/Y; OCT +2.7%

- MNI: JAPAN NOV CORP GOODS PRICE INDEX +2.7% Y/Y; OCT +2.7%

- JAPAN NOV CORP GOODS PRICE INDEX +0.3% M/M; OCT +0.5%