USDCAD TECHS: Has Pierced The 50-Day EMA

- RES 4: 1.3920 High May 21

- RES 3: 1.3862 High May 29

- RES 2: 1.3798 High Jun 23

- RES 1: 1.3747/74 50-day EMA / High Jul 17

- PRICE: 1.3715 @ 16:56 BST Jul 18

- SUP 1: 1.3639/3557 Low Jul 08 / 03

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

USDCAD is trading closer to its recent highs. Attention is on resistance at 1.3747, the 50-day EMA. It has been pierced. A clear break of it is required to highlight a possible stronger short-term reversal. This would open 1.3798, the Jun 23 high. For now, a bear trend remains firmly in place. A resumption of weakness would refocus attention on key support at 1.3540, the Jun 16 low. Clearance of this level would confirm a resumption of the downtrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Late SOFR/Treasury Option Roundup

Mixed SOFR & Treasury option flow on net, underlying futures well off initial gap bid post FOMC, curves mildly steeper while projected rate cut pricing gains slightly on longer dates vs. this morning's levels (*) as follows: Jul'25 at -2.6bp (-3.6bp), Sep'25 at -18.7bp (-17.7bp), Oct'25 at -31.6bp (-29.1bp), Dec'25 at -48.2bp (-45.1bp).

- SOFR Options:

- +3,000 SFRH6 95.50 puts, 3.0 vs. 96.325/0.10%

- +2,500 SFRZ5 96.25/96.37/96.62/96.75 call condors, 1.75

- -1,000 SFRZ5 96.12 straddles, 42.5

- +4,000 SFRU5 95.68/95.81/96.00/96.12 put condors, 4.5

- +2,000 SFRZ5 95.75 puts, 3.75

- -5,000 SFRN5 95.68/95.81 put spds, 1.75 ref 95.89

- Pit/screen over +55,000 SFRU5 95.50/95.62 put spds, .25 ref 95.86, bid for more

- 3,700 SFRZ5 96.25/96.50 call spds vs. 95.68 puts ref 96.115

- -3,000 0QN5 97.25/97.31 call strip vs. SFRN5 96.50/96.56 call strip, cab net 0QN over

- +4,000 SFRQ5 95.68/95.75 put spds, 2.5 ref 95.855

- +5,000 0QH6 97.25/98.00 call spds, 13.0 vs. 96.745/0.18%

- 2,000 SFRV5 96.18/96.43 call spds ref 96.09

- 2,800 SFRU5 95.93/96.00/96.06 call flys

- +3,000 SFRU5 95.56/95.62/95.68 put flys, 1.25 ref 95.86

- +12,800 SFRH6 96.50/97.00/98.00 broken call flys, 2.5 ref 96.32 to -.33

- 1,600 3QZ5 96.25/96.62/97.00 call flys, 8.0

- Treasury Options: (July serial options expire Friday)

- 5,000 FVU5 111 calls, 10.5 ref 108-07.75 to -08

- 2,500 TUN5 103.25/103.37/103.5/103.62 put condors, ref 103-22

- 1,250 FVN5 108.25/108.5/109/110 broken call condors ref 108-09.75

- 1,800 FVN5 107.25/107.75/108.25 put flys ref 108-09.5

- 2,000 USU5 114/116/118 call flys ref 114-06

- +5,000 TYQ5 110.5/111.5/112 1x3x2 call flys 4 over TYQ5 112/113/113.5 1x3x2 call flys

- +2,000 TYQ5 114.5 calls, 8

- -3,000 TYN5 110.75 calls, 16 vs 110-22.5/0.50%

- +3,000 TYN5 111.5 calls, 6

- +1,500 Wed wkly TY 110.75/111/111.25 call flys, 3.0

- +6,500 Wed wkly FV 107.5/107.75 put spds, 1 (exp today)

- +2,000 TYN5 110.5/111/111.5 call flys, 8

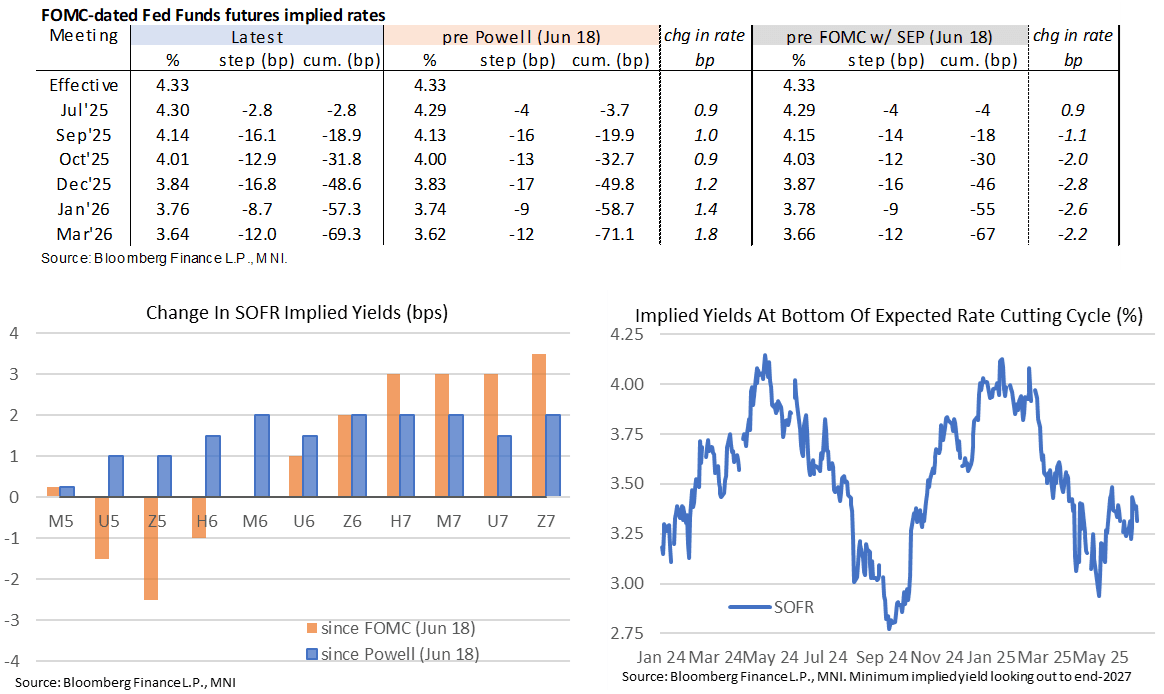

STIR: Twist Steepening In Fed Rates In Contained Reaction To Dot Plot & Powell

- Near-term Fed rates are back more dovish on pre-FOMC levels again (SFRZ5 yield -3bps since 1400ET decision) having at one point in Powell’s press conference fully unwound the front-loaded dovish reaction to the unrevised 2025 median dot.

- The continued reaction is however distorted by a drop in crude futures from Trump Iran comments, including that he hasn’t made a decision on using force yet.

- Fed Funds implied rates are 1bp higher since the decision for the July meeting but beyond that 1-2.5bp lower for 2025 meetings.

- Cumulative cuts from 4.33% effective: 3bp Jul, 19bp Sep, 32bp Oct, 48.5bp Dec and 57bp Jan.

- That said, a combination of increases for 2026 & 2027 median dots and Powell patience helps see greater increases in 2026 and 2027 implied yields.

- SOFR futures steepened further through the conference, with SFRZ5/Z6 shifting from -0.65 pre-decision to -0.615 pre-Powell and now -0.605.

- The implied terminal yield of 3.27% (SFRZ6) is 2bp higher since Powell took to the podium, 3bp higher post-FOMC but still -1bp lower on the day. It has closed lower on Jun 12.

- Powell helped a hawkish reaction with various messages rather than a single headline: downplaying the message from the dot plot, implied patience (will learn a great deal over the summer/looking over the coming months) and noting that rates aren’t very high with policy being modestly rather than previously moderately restrictive. He did however in the last question note "we don't rule things in or out. Certainly a hike is not the base case at all."

FOREX: Greenback Reverses Higher as Powell Downplays Economic Concerns

- The US dollar spent much of the pre-Fed session trading with a moderate downward bias as President Trump hinted at potential talks with Iran, which fleetingly boosted risk sentiment. On the FOMC release, this greenback weakness extended as the Fed confirmed the median dot for 2025 year-end rates as steady in predicting two further cuts this year.

- USDJPY traded down to a low of 144.34 on the release, while EURUSD tried to consolidate gains back above 1.15.

- However, higher median Fed dots for 2026 and 2027 and a relatively optimistic view of economic activity and the labour market prompted a sharp dollar reversal higher through Chair Powell’s press conference, with the USD index rallying to fresh session highs.

- Once again, USDJPY was in focus here as the pair rose back above 145.00, narrowing the gap to the overnight highs and initial resistance around 145.45. Further out, key short-term resistance is 146.28, the May 29 high.

- Both the EUR and GBP were laggards amid the dollar reversal, both notable underperformers across G10. For GBPUSD, we have printed fresh pullback lows as the move extends below 1.3415, placing greater attention on the next important support, which lies at 1.3350, the 50-day EMA.

- Thursday remains busy on the central bank front, with the SNB kicking off the calendar. This will be followed by decisions from the Norges Bank and the BOE. In terms of data, New Zealand GDP and Australian employment figures are scheduled.