BOE: Greene due to speak on monetary policy at 17:30BST / 12:30ET

Sep-24 15:25

- Greene is due to speak on Wednesday in a speech entitled ‘Supply shocks and monetary policy’ (17:30) at the University of Glasgow Business School. We don't expect this to be market moving unless Greene says that she no longer believes that rates are restrictive. The text will be released here.

- This would be in contrast to her comments in her appearance ahead of the Treasury Select Committee on 3 September, when she said that "I think there are indications that we're still restrictive, but I'm not convinced that we're meaningfully restrictive. We've been in a rate cutting cycle for, you know, a year now, so it can't go on forever with us also being restrictive."

- Greene was also concerned about inflation persistence while being less concerned about downside risks to the labour market. We would be surprised if she changes this tone today. And we would be very surprised if she supported a November cut following her hawkish dissent in August.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 13W AUCTION: NON-COMP BIDS $2.072 BLN FROM $82.000 BLN TOTAL

Aug-25 15:15

- US TSY 13W AUCTION: NON-COMP BIDS $2.072 BLN FROM $82.000 BLN TOTAL

FED: US TSY 26W AUCTION: NON-COMP BIDS $1.799 BLN FROM $73.000 BLN TOTAL

Aug-25 15:15

- US TSY 26W AUCTION: NON-COMP BIDS $1.799 BLN FROM $73.000 BLN TOTAL

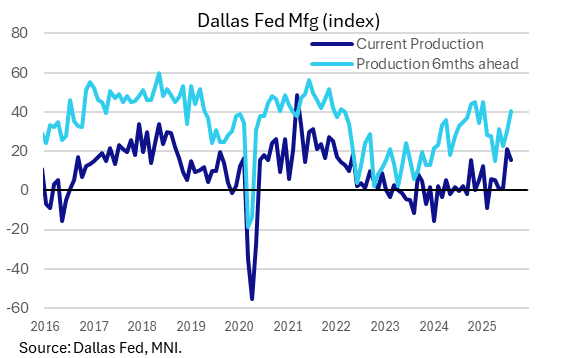

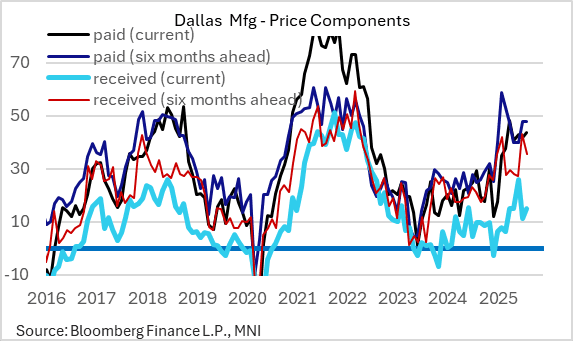

US DATA: Better Activity, Still-Elevated Inflation In Texas Manufacturing Sector

Aug-25 15:05

The Dallas Fed's Texas Manufacturing Outlook Survey for August showed continued growth in regional production, albeit with a slightly bigger than anticipated relapse in the overall general business activity index and slightly firmer price pressures. While these readings are volatile month-to-month, they continue to suggest improvement in activity after a tariff-hit period, but price pressures remain elevated (and regional firms still sound extremely concerned about tariff impacts).

- The general business activity index, which is tracked by Bloomberg consensus, missed expectations at -1.8 (vs -0.9 expected, +0.9 prior), which the Dallas Fed characterizes as "indicating little change in activity".

- But this underplayed the broader current strength in activity in the report. The production index, "a key measure of state manufacturing conditions" per the report, fell to 15.3 from 21.3 prior but remained above average, and other measures were also solid. The highlights in that department were new orders, rising for the first time since January (5.8 from -3.6), and shipments rising 12 points to 14.2 for a 3+ year high.

- Forward-looking indicators also suggested improvement (the 6-month production outlook rose to a 7-month high 40.4), while "labor market measures suggested increases in employment and work hours".

- Against this backdrop, price pressures mostly edged higher: current prices paid to a 5-month high 43.7 (up 2.0 points) with priced received at a 2-month high 15.1 (up 4.0 points). 6-month ahead prices paid were basically unchanged at 47.8 (up 0.1 points) albeit a fresh 5-month high, with future prices received pulling back to a 2-month low -12.3 from -4.5.

- Special questions (which also covered services firms ahead of Tuesday's Dallas Fed services release) showed that 48 percent of surveyed businesses "said they’ve been negatively impacted by higher tariffs this year" (just 2% said they were positively impacted), with more than 70 percent of manufacturing firms noting negative impacts. Note also "Firms negatively impacted by tariffs were mixed on whether they passed on cost increases to customers (48 percent of firms) versus absorbed costs internally (39 percent of firms)." The anecdotes in the report add some color to these findings - link here.