FOREX: GBPUSD Hovers Above Trendline Support

Sep-24 09:22

- Over the course of the European morning, the US Dollar is trading with a supportive tone. Despite most major pairs remaining well within the post-Fed ranges, the likes of EUR and GBP have extended session declines to just shy of 0.4% in recent trade.

- For EURUSD, the solid amount of option expiries between 1.1750-1.1800 appear to have capped the overnight price action, with the pair slowly edging back below 1.1775 as we approach the NY crossover. Last week’s low at 1.1726 is the immediate point of reference on the downside, however, support to watch is at 1.1678. the 50-day EMA.

- GBPUSD has traded through the 50-day EMA, and this leaves support at 1.3458 exposed, a trendline drawn from the Aug 1 low. Clearance of this line would strengthen a bearish threat. Below here, key support resides at 1.3333, the Sep 3 low.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

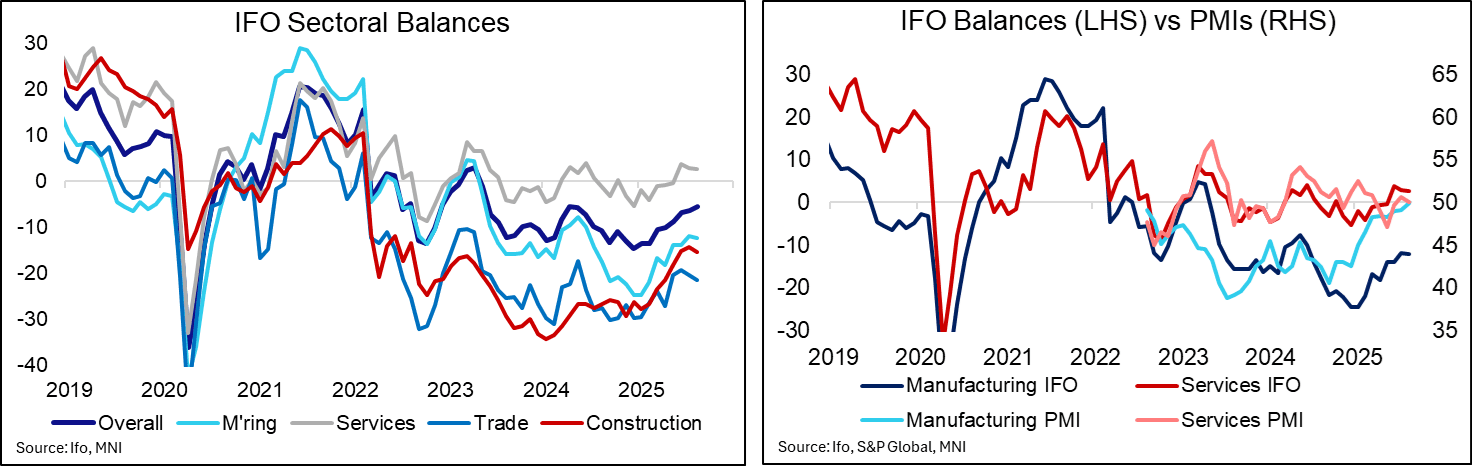

GERMAN DATA: Latest Ifo Improvement On Shaky Ground Looking By Sector

Aug-25 09:15

The details of the Ifo business climate by sector didn’t corroborate the minor increase in the overall index, seemingly implying a higher response rate from services-related firms in the August survey. We wonder if that's down to response rates in the holiday season.

- The business climate balance increased from a seasonally adjusted -6.4 to -5.5 (we wrote on the index earlier – GERMAN DATA: A Sixth Consecutive Improvement For Ifo Business Climate – 0935BST) but all four main sectors saw their business climate balance soften.

- Latest sectoral values with highlights from the Ifo press release (link):

- Services inched lower for a second month to 2.6, but remains the only sector in positive territory. “While the current situation was assessed as significantly better, expectations became more cautious. Sentiment, however, improved among architecture and engineering firms.”

- Manufacturing gave back some of its latest increase, dipping to -12.2 from -11.9. “Companies were somewhat less satisfied with current business. Expectations were revised slightly downward, and there are still no indications of growth in order intake. Sentiment among capital goods manufacturers improved noticeably.”

- Construction unwound the latest increase as it fell to -15.3 from -14.3. “The index edged down slightly after many months of stability. Companies expressed less satisfaction with the current situation. However, their outlook for the coming months improved.”

- Trade continues to lag and saw a second monthly decline to -21.4 from -20.3 for its lowest since April. “The index weakened, driven by poorer business performance. However, expectations were slightly less pessimistic.”

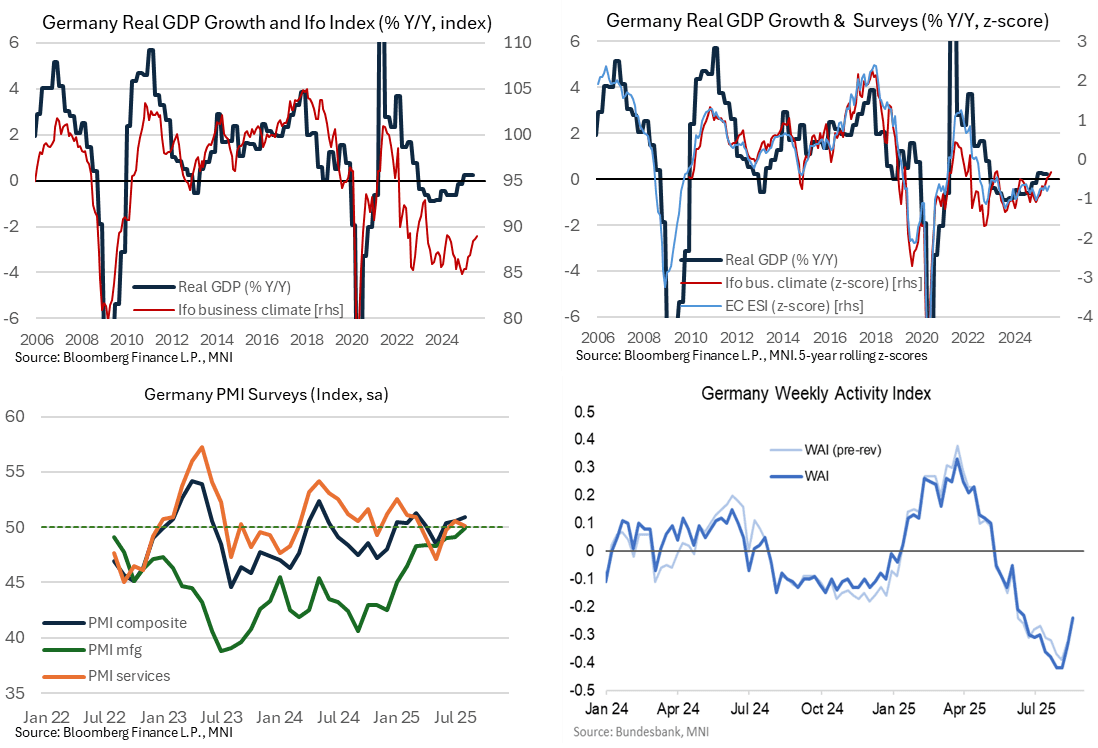

GERMAN DATA: A Sixth Consecutive Improvement For Ifo Business Climate

Aug-25 08:35

The Germany Ifo business climate index increased for a sixth consecutive month in August as it takes it to the high of its range for the past eighteen months, but it still suggests little material upside to tepid German real GDP growth despite this.

- The Ifo Business Climate index was close to expectations as it slightly improved in August to 89.0 (cons 88.8) from 88.6 in July.

- Whilst still subdued by historical standards, it’s nevertheless at its highest since Apr 2024 on the back of six consecutive monthly improvements.

- This trend improvement has come with increases in both the current assessment and more notably the expectations indexes. This expectations-led improvement continued this month, with the expectations index rising to 91.6 (cons 90.5) from 90.8 vs the current assessment edging a tenth lower to 86.4 (cons 86.7).

- A seeming post-pandemic structural break with the historical fit between the business climate index and real GDP growth complicates the readthrough to growth implications, although rolling z-scores have more recently been useful.

- Here, the Ifo business climate has started to look a little more optimistic than the European Commission’s Economic Sentiment Index (to July) but even then the Ifo series suggests little upside to still tepid German real GDP growth of 0.2% Y/Y as of Q2 (having averaged -0.4% since 1Q23).

MNI: GERMANY AUG IFO BUSINESS CLIMATE INDEX 89

Aug-25 08:00

- MNI: GERMANY AUG IFO BUSINESS CLIMATE INDEX 89