FOREX: FX OPTION EXPIRY

Of note:

EURUSD 8.64bn between 1.0830/1.0915.

USDJPY 2.45bn at 155.45/155.50.

AUDUSD 1.17bn at 0.6600 (fri).

GBPUSD 1.32bn at 1.2795 (wed).

AUDUSD 2.6bn at 0.6600/0.6630 (wed).

NZDUSD 1.53bn at 0.6200 (wed).- EURUSD: 1.0830 (300mln), 1.0835 (384mln), 1.0840 (559mln), 1.0850 (758mln), 1.0860 (1.21bn), 1.0865 (463mln), 1.0895 (396mln), 1.0900 (2.12bn), 1.0905 (882mln), 1.0915 (1.57bn).

- USDJPY: 155.15 (1.23bn), 155.45 (1.32bn), 155.50 (1.13bn), 156.00 (758mln), 157.00 (1.52bn).

- USDCAD: 1.3675 (275mln), 1.3685 (340mln).

- AUDUSD: 0.6700 (519mln).

- USDCNY: 7.2450 (696mln), 7.2500 (262mln), 7.2550 (896mln).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA: Call buyer

SFIM4 95.80c, bought for 0.25 in 5k (ref 94.98, 5 del).

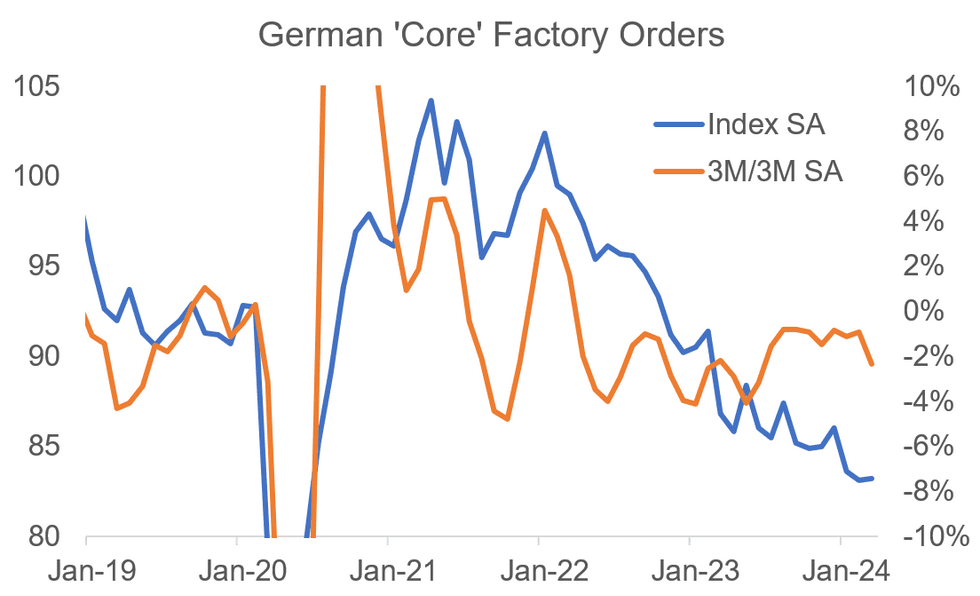

GERMAN DATA: Weak Domestic Demand Drives Factory Orders Drop, But 'Core' Stable

German factory orders fell by 0.4% M/M in March, softer than the +0.4% expected and an even bigger downside miss when considering a downward revision in February (by 1.0pp to -0.8% - all figures are real, SWDA). The underlying 'core' measure pointed towards some stabilisation, however.

- Factory orders fell 1.9% Y/Y (vs -0.7% consensus) vs -8.8% in February, with the improvement in the annual comparison mainly due to base effects.

- Core (ex-large ticket items) orders, a better measure of underlying activity, increased by 0.1% in March (vs -0.6% prior); its less volatile 3M/3M measure printed weaker than before, though, at -2.3% (vs -0.9% prior).

- The breakdown showed the slight 'core' rise was driven by foreign orders (+2.0% M/M vs -1.8% prior, the fastest growth in 4 months), with similar growth in both the Eurozone and non-EZ regions). In contrast, domestic orders decreased by 2.5% (vs +1.0% prior).

- From a category-by-category perspective, core orders rose in all main groups except intermediate goods, with durable goods a notable area of strength (+2.4% M/M vs +3.5% prior after a very weak Jan/Dec).

- Real manufacturing turnover meanwhile declined 0.7% M/M in March (1.1% prior, downwardly revised 1.1pp), adding to evidence that data released Wednesday will show industrial production ended its recent 2-month in March (-0.7% cons vs +2.1% prior).

- Overall, even though core orders are stabilising, the data looks weak compared with other recent German economic prints and soft domestic orders continue to point to an export-led rather than domestic-demand fuelled recovery. Looking ahead, while the key surveys (PMI and IFO) both suggested that manufacturing activity improved in April, they also both remained in contractionary territory.

MNI, Destatis

MNI, Destatis

GILTS: /STIR: Goldman: BoE To Clarify Reaction Function, Continue To Prefer Long 30s Vs. U.S.

Ahead of this week’s BoE meeting, Goldman Sachs expect “the market to focus on the conviction of the core of the MPC on how secure the underlying trend disinflation is.”

- “Disagreement among the MPC on the degree of inflation progress has made it more difficult for UK yields to fall.”

- “The vote split may not reveal fresh insights on that dimension, although if Deputy Governor Ramsden were to change his vote to a cut, it would be a dovish signal for current market pricing.”

- “We also think the new inflation projections are likely to show more confidence that inflation is sustainably coming down beyond H1.”

- “Though our economists expect the first cut to occur in June we do not think the MPC needs to send an explicit signal on Thursday, especially as current guidance already says the Bank rate is under review.”

- “In any case, we continue to prefer divergence trades in U.S. vs UK and think that view is best expressed at the long-end of the curve – stay long 30y Gilts against U.S. Tsys.”