AUSSIE BONDS: Futures Lower But Up From Session Lows, Job Vacancies Fall

Aussie bond futures are holding lower, but slightly up from session lows. 10yr futures were last around 95.63, off 4bps, (with lows at 95.61). 3yr futures were around 96.445, off 2bps (session lows at 96.42). ACGB yields are holding around 2-4bps higher, also off best levels. The back end is firmer in yield terms, the 10yr close to 4.33%, while the 3yr was last near 3.53%. This leaves the 3/10s curve near 80bps, +2bps steeper for the session.

- Earlier highs in the 3yr yield were close to 3.55%, which was near recent highs back to mid July. Beyond that lies the 3.60% area.

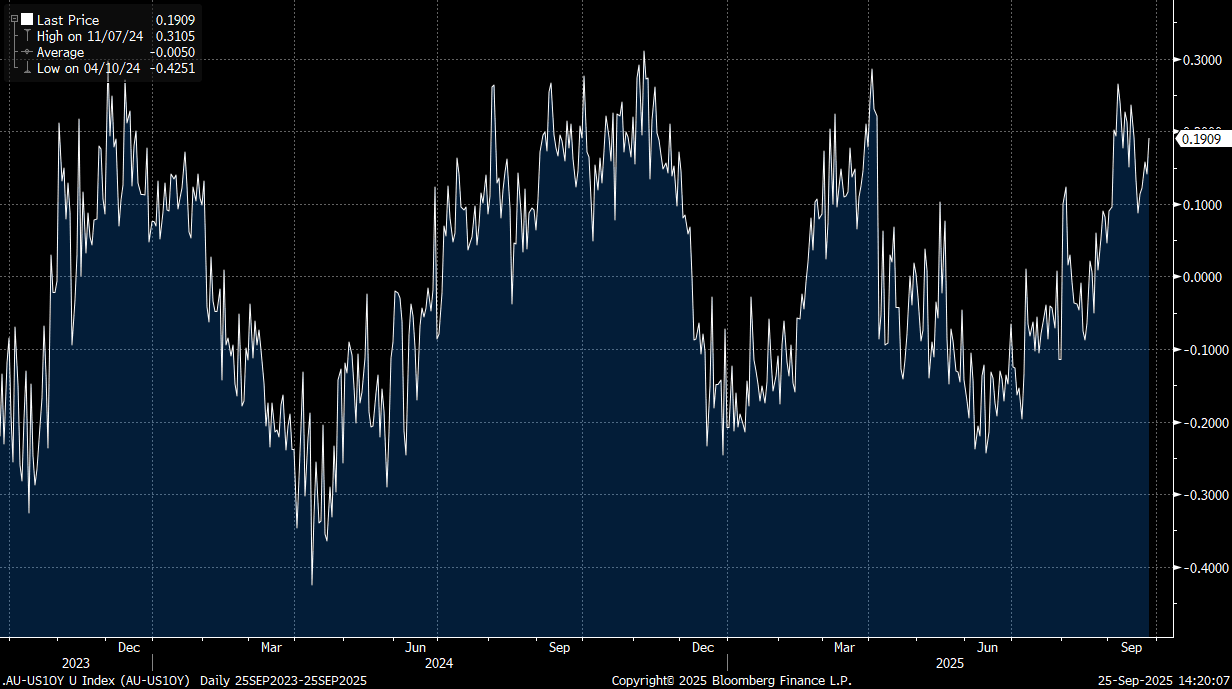

- For the 10yr, focus may rest with the 10yr spread with the US. The AU-US 10yr spread got above +20bps earlier, but we sit back under this level in latest dealings. The chart below shows that the spread hasn't been able to sustain the +20-30bps region in recent years.

- On the data front, job vacancies continued to normalise in Q3 but the pace has slowed implying a gradual easing in labour market conditions. In the 3 months to August they fell 2.7% q/q after rising 2.8% q/q to May but are now down only 1.5% y/y after-2.8% and -16.9% y/y in Q3 2024. The level is in line with February’s.

- The data calendar is empty until next Tuesday , when building approvals, private credit, along with the RBA decision are all due. The RBA is seen on hold at 3.60%.

Fig 1: AU-US 10-yr Spread Back Close To Cycle Highs

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

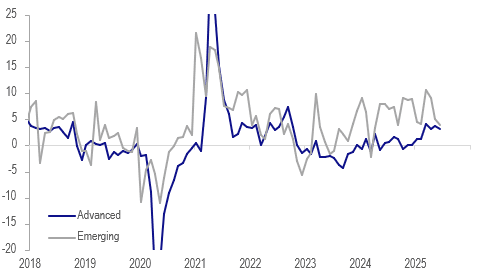

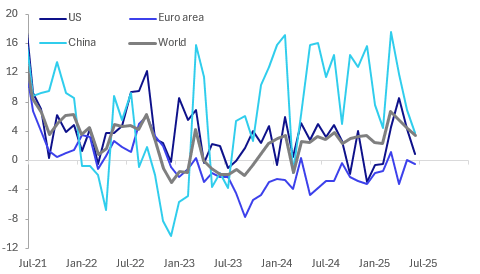

GLOBAL MACRO: Global Trade Growth Slowing After Q1’s Frontloading

CPB global trade data showed a continued slowdown in volumes in June after the frontloading earlier in the year to beat the initial US import tariff deadline. Global trade fell for the third straight month, while it was the second for exports. The bringing forward of shipments is likely to make interpreting trade data difficult for a while and some Asian central banks have warned the pullback could impact H2 2025 growth.

Global export volume growth y/y%

- Global trade volumes fell 0.4% m/m in June to be up 3% y/y after -0.4% m/m & +4.1% y/y. The Baltic Freight Index suggests they could recover in coming months but container rates suggest further slowing.

- Exports contracted 0.3% m/m to be up 3.4% y/y after -0.8% m/m & +4.4% y/y. 3-month momentum slowed over Q2 but remains robust. Growth peaked in March at 6.7% y/y.

- Developed markets saw their exports rise 0.1% m/m in June but annual growth slowed to 3.1% from 3.8% in May and 4.2% in March. Shipments are being driven by Japan and advanced Asian countries while they’re weak from Europe. The US also appears to have frontloaded exports in case of retaliation for its trade policy.

- Emerging market export volumes fell 0.7% m/m to be up 4.0% y/y after -0.8% m/m & +5.1% y/y. They peaked in March at 10.7% y/y. China and emerging Asia have seen a considerable slowdown since March at 3.7% y/y from 17.5% and 3.6% y/y from 10.8% respectively. Eastern European export growth is weak while Latin America’s remains solid.

Export volumes y/y%

AUSSIE BONDS: Yields Tick Up, RBA Mins Uncertain On Pace Of Easing

Aussie bond futures sit off earlier highs, but have traded tight ranges overall so far in Tuesday trade. YM was last near 96.60, -.01, while XM was last at 95.67, -.02. Earlier highs in this benchmark were at 95.70. Government bond yields are slightly higher across the curve, with the back end slightly firmer from a yield standpoint. US developments have been in focus, with Trump stating he will remove Fed Governor Cook, driving a steeper US yield curve. For Australia, the 3yr ACGB yield was last around 3.39%, up 1bps, while the 10yr was close to 4.31%, up nearly 3bps.

- We had the RBA minutes earlier, where we saw a brief yield pullback but there was no follow through. Given the August decision to cut rates was unanimous, the discussion regarding the outlook was the important part of the RBA meeting minutes. They were clear that further rate cuts were consistent with underlying inflation returning to the 2.5% mid-point of the target band. It was the pace of future easing that “was not yet possible to judge” with the risks around the outlook “in both directions”.

- There hasn't been a strong shift in RBA market pricing, with the OIS dated Dec contract still around the 3.23% level, which is where we ended Monday trade.

- In the swap space we have been relatively steady as well, with the 3yr last close to 3.25%.

- Tomorrow's calendar brings the July CPI print.

BONDS: NZGBS: Front End Yields Lower, Following US Lead, 2yr Swap At Fresh Lows

The initial impetus in NZ government bond yields was higher, but there was no follow through. The 2yr NZGB yield got near 3.04% in the first part of dealing, but we now sit back at 2.98%, off around 3bps. Other parts of the curve are down less in yield terms, but equally have moved off earlier highs. The 10yr was last around 4.36%, off earlier highs near 4.40%. NZ yields look to be largely following US developments, where US President Trump stated he is removing Fed Governor Cook, with immediate effect. This has weighed on front end US Tsy yields, but aided back end yields as the Tsy curve has steepened.

- In the swap space, the 2yr rate has made fresh lows, last near 2.74%, off around 5bps for the session so far. These levels were last seen in the first parts of 2022.

- Local news flows has been light. Via BBG: "NZ July Residential Mortgage Lending Is Highest Since 2021, Gains 36% y/y, Increases 3% m/m after seasonal adjustment: RBNZ". This may point to better housing market momentum, as we progress through the second half. Market expectations remain for further easing, while the RBNZ noted after its easing last week that the lags involved with monetary policy will continue to aid housing market sentiment.