HKD: Further HKD Buys May be Forthcoming to Boost Local Rates

Jun-26 07:44

- Just ahead of the APAC open Thursday, HKMA confirmed they intervened on the weak side of the band, buying HKD 9.42bln (~ $1.2bln) to defend the trading band - the first intervention on this side of the band since early 2023, but follows action on the strong-side just 8 weeks ago. We see this as the shortest gap on record between intervention on each side of the band in it's current form.

- The intervention settles on Friday, meaning Hong Kong's aggregate balance should shrink by ~HKD10bln to ~HKD 164bln.

- Today's ~$1.2bln sale is minor relative to the bank's intervention on the strong-side this year, which amounted to over $15bln - but the bank's staggered approach to intervention may mean we see further USD/HKD selling and further volatility in local rates before spot moves materially away from 7.85.

- HIBOR set higher in response to the intervention: 1m fixed at 0.96554% for a 7-week high, however HKD swap rates remain supressed, and no relief here could pressure HKMA to act again. This was noted by the bank's statement that they will "continue to closely monitor market developments". Through the last phase of intervention on the weak side in 2023, HKMA intervened on 8 occasions, buying a total of HKD 55bln. In 2022 interventions totalled HKD 242bln, across 41 occasions.

- Despite HKMA's actions today, carry remains key. USD/HKD differentials remain attractive even with today's move - and sharper intervention, twinned with a building 2025 IPO pipeline, improved corporate activity via bond sales and dividends may be required to alleviate excess liquidity, and reverse the pressure on local rates this year.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

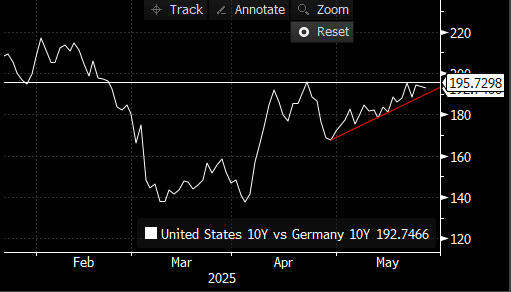

BONDS: The Tnotes/Bund spread finds some resistance

May-27 07:36

- The Tnotes/Bund is still finding some resistance at the 195.00bps mark, got close to 196.00bps.

- This is the April high and widest level since 21st February.

- The spread is 1.7bp tighter, as EGB futures outperforms led by the French OAT, following the lower than expected French Inflation.

- Further tightening bias in the US/German 10yr Spread, would see fades to 185.00bps, but a clear break above the 195.00bps will open to 200bps.

STIR: Light Dovish ECB Repricing Following Soft French Inflation Data

May-27 07:35

The lower-than-expected French flash May HICP print drove light dovish repricing in ECB-dated OIS, with ~1bp added to this year’s implied rate cutting cycle. There are now just shy of 60bps of easing priced through year-end (i.e. a deposit rate of between 1.50% and 1.75%. ECB speakers have generally expressed confidence in the inflation outlook in recent weeks, which has likely limited the dovish reaction to the data. Tariff developments will be key in determining the likelihood of sequential 25bp cuts in both June and July.

- France is also only 19% of the Eurozone HICP basket, with the other major countries (Germany, Italy and Spain) set to report this Friday.

- Following the data, BdF Governor Villeroy said that the data was “another very encouraging sign of disinflation in action”. Villeroy noted that “the normalization of monetary policy is doubtless not complete and we could — in the conditional — see this at our Governing Council meeting next week”.

- This isn’t a surprising view, with Villeroy stating on May 13 that “the Trump administration’s protectionism will lead to a restarting of inflation in the US, but not in Europe, which will doubtless allow for another interest-rate cut between now and the summer”.

- Euribor futures are +0.5 to +4.5 ticks through the blues, with blues leading the rally (following the JGB-led bull flattening in global FI markets this morning).

- The EC’s May consumer and business survey is due at 1000BST, while Bundesbank’s Nagel is scheduled to speak this evening.

| Meeting Date | ESTR ECB-Dated OIS (%) | Difference Vs. Current Effective ESTR Rate (bp) |

| Jun-25 | 1.922 | -24.6 |

| Jul-25 | 1.838 | -33.0 |

| Sep-25 | 1.706 | -46.2 |

| Oct-25 | 1.653 | -51.5 |

| Dec-25 | 1.577 | -59.1 |

| Feb-26 | 1.556 | -61.2 |

| Mar-26 | 1.547 | -62.2 |

| Apr-26 | 1.554 | -61.4 |

| Source: MNI/Bloomberg. | ||

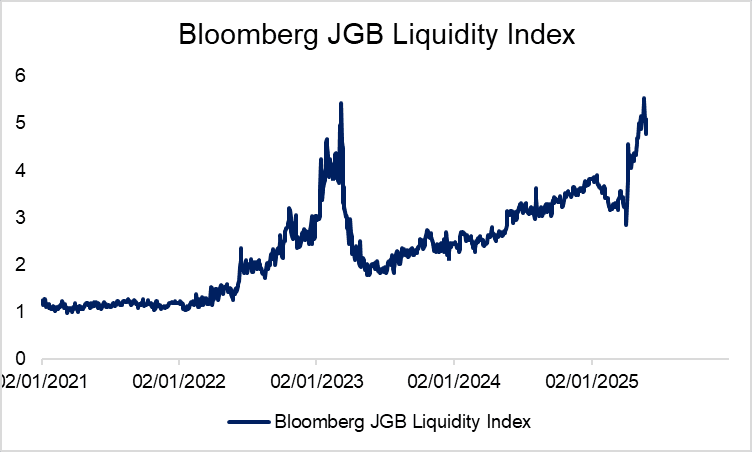

JGBS: Mid-June In Focus For MOF Selling and BOJ Buying Tweaks

May-27 07:23

- These factors have come against a backdrop of reduced liquidity in the Japanese bond market, especially at the long-end. Bloomberg’s JGB liquidity index (which isn’t a perfect measure of this given it includes all bonds with a maturity greater than one year) has fallen from last week’s highs but remains elevated, indicating worse liquidity conditions.

- Reuters notes that the MOF will make a decision on its issuance plan around mid- to-late June, after holding discussions with market participants.

- This will align closely with the BOJ’s June 17 meeting, where the bank will review its bond purchase reduction plan. The BOJ is currently reducing bond purchases by JPY400 billion per quarter through March 2026. A former BOJ official recently told MNI that the BOJ should clearly communicate the pace at which it plans to reduce its JGB holdings, including both purchases and expected redemptions, to help maintain bond market stability.