EU CREDIT MACRO: CREDIT MACRO: Fund Flows

May-24 14:49

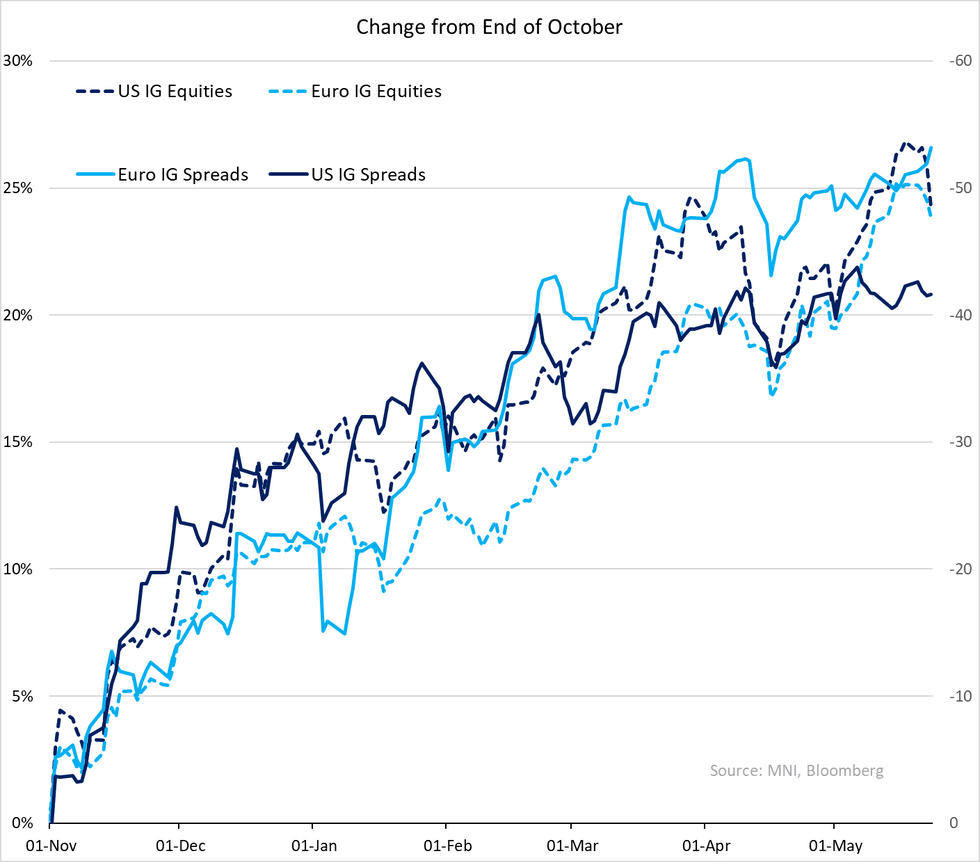

- Broad based inflows hitting everyone; €/$/£ IG & HY with particular strength in $. US led equity inflows & govvie inflows across both regions continued.

- Credit macro is dwindling in its relevance to spreads for now. UK April (real) retail sales miss this morning doing little to take rates off US PMI beats - the miss continues weak retail data for April. Some weakness in $ETF's on -$886m outflow from LQD - hard to be concerned with no signs of it being broad-based yet but also heading into a seasonal summer lull that tends to particularly acute in July/August and in €s. Add on any opportunistic pre-funding estimates (particularly in HY) that we may be in for an even larger dip with perhaps some offset in IG on a continued M&A pickup.

- Supply expectations (bbg) for next week in €/£ IG/HY incl. covered are at ~€16.5b down from ~€25b for this week (actual €28b). $IG at $15-$20b down from $20-25b this week (actual $26b). Public holidays on Monday in UK & US.

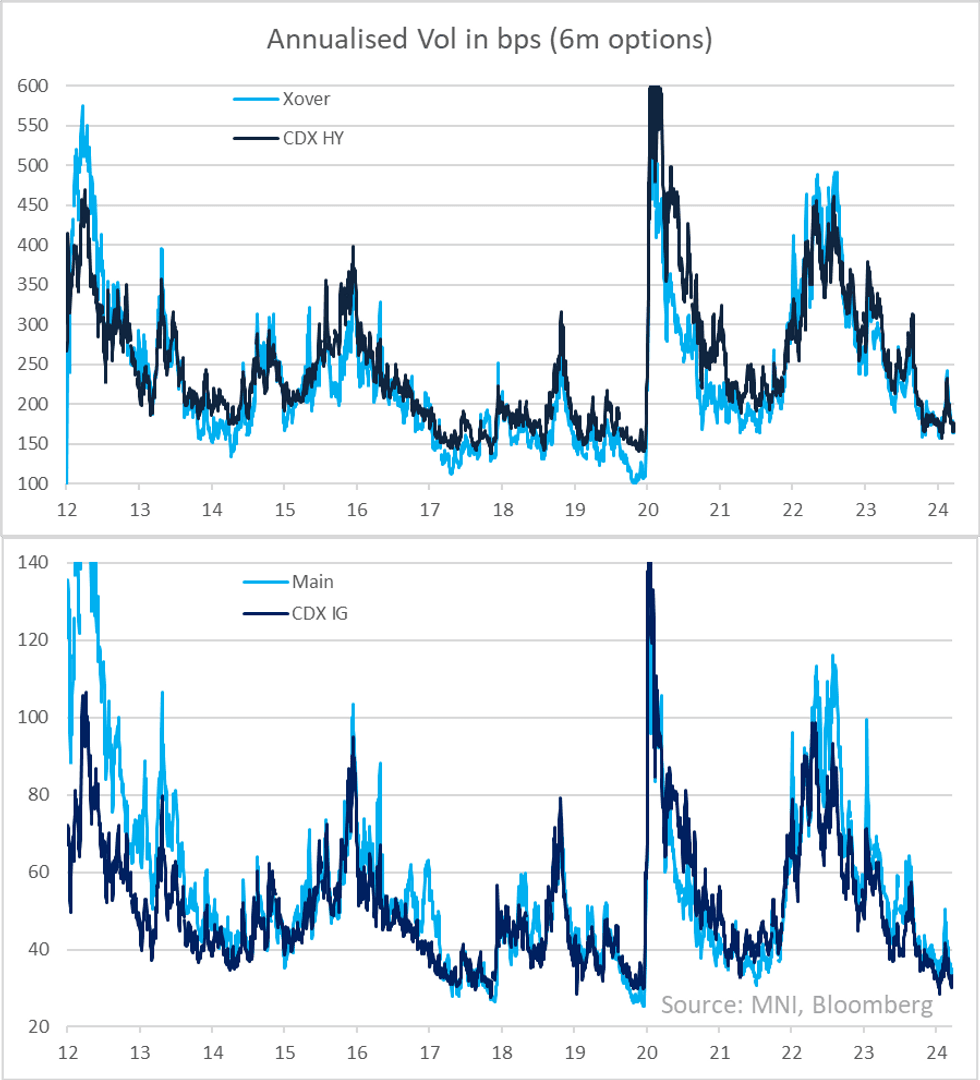

- In absence of anything interesting in macro we will leave you with below - vol in spreads are dead (well known) but so are option implied forward vols - 6m annualised in bps on CDX & iTraxx indices below.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB SYNDICATION: 30-year Jun-54 GGB: Priced

Apr-24 14:44

- Size: E3bln (larger than the E1.5-2.5bln MNI expected)

- Reoffer: 98.057 to yield 4.241%

- Books closed in excess of E33bln (inc E1.8bln JLM interest)

- Spread set at MS+165bp

- Guidance was MS+175bp area then revised to MS+170bp +/-5bps (WPIR)

- Benchmark: 2.50% Aug-54 Bund + 151.8bp

- Coupon: 4.125% annual, act/act, short first

- Maturity: 15 June, 2054

- Settlement: May 2, 2024

- ISIN: GR0138018842

- Bookrunners: BNPP, BofA, DB (B&D), GS, JPM, PIRAEU

- Timing: Allocations and pricing later today

From market source / Bloomberg

GILT AUCTION PREVIEW: On offer next week

Apr-24 14:34

The DMO has announced it will be looking to sell GBP3.75bln of the 4.625% Jan-34 Gilt (ISIN: GB00BPJJKN53) at its auction next Wednesday (May 1st).

US EIA: CRUDE OIL STOCKS EX SPR -6.37M TO 453.6M APR 19 WK

Apr-24 14:32

- US EIA: CRUDE OIL STOCKS EX SPR -6.37M TO 453.6M APR 19 WK

- US EIA: DISTILLATE STOCKS +1.61M TO 116.6M IN APR 19 WK

- US EIA: GASOLINE STOCKS -0.63M TO 226.7M IN APR 19 WK

- US EIA: CUSHING STOCKS -0.66M TO 32.4M BARRELS IN APR 19 WK

- US EIA: SPR +0.79M TO 365.7M BARRELS IN APR 19 WK

- US EIA: REFINERY UTILIZATION WEEK CHANGE +0.4% TO 88.5% IN APR 19 WK