HUF: Forint Sensitivity to NatGas Prices Assists 4% Recovery from YTD Low

A number of factors have been working in favour of the forint after the currency hit its lowest level since 2022 earlier in the year. While a broader rally of the euro against a weak greenback will have assisted gains, optimism that a Ukraine ceasefire deal can be reached has provided a substantial tailwind across CEE FX, notably prompting a rally in the Polish zloty to a 7-year high. But owing to the lack of improvement in domestic fundamentals and uncertainty over how the NBH's reaction function will evolve, questions over the sustainability of the HUF rally may soon be raised.

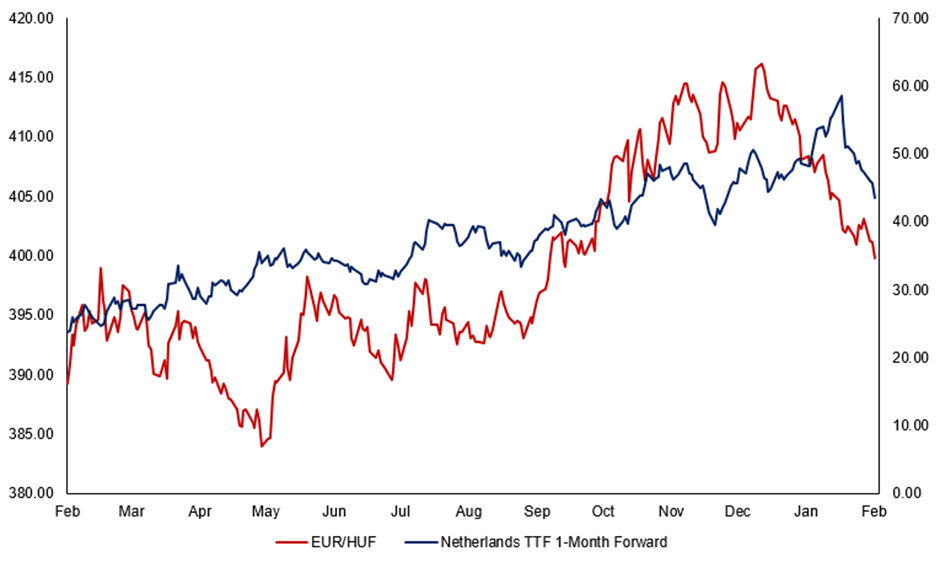

- The forint may stand to outperform if a Ukraine-Russia ceasefire deal is reached given the currency’s acute sensitivity to swings in natural gas prices, with 1-month TTF forwards over 23% lower compared to the early-Feb highs. EURHUF has moved in tandem with the turn lower, tipping the 14-day RSI below the 'oversold' 30-threshold in the process, with the cross at a 4-month low.

- Prospects of a more hawkish policy mix following the above consensus inflation print for January has also underpinned the forint’s rally. The data leaves the central bank with little room for manoeuvre even with new management taking the helm next month. In practice, this likely means we will see little material change to the central bank’s key guidance next month, with NBH expected to retain its “careful and patient approach” to monetary policy.

- However, the forint’s high beta to swings in risk sentiment raise questions of how far the rally can run. JP Morgan noted last week that they believe “we are at peak NBH hawkishness,” while ING say “the market remains very fragile, and we can’t label the situation as a rock-solid turnaround.”

- Indeed, it remains to be seen how central bank communication evolves under the leadership of Varga, and whether the central bank retains its hawkish bias once inflation peaks and slows down through H2-2025. Meanwhile, markets still await clarity over President Trump’s tariff proposals, while domestic economic activity data is yet to suggest that a meaningful turnaround in the economy is on the horizon.

Figure 1: EUR/HUF vs. Netherlands TTF Natural Gas 1-Month Forward

Source: MNI/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: Estoxx calendar put spread

SX5E (21st Feb) 160p vs (20th Jun) 130p, bought the Feb for 0.70 as a 1x1.5 put spread in 12k (12kx18k).

GILT AUCTION PREVIEW: Potential short-dated conventional gilt tender Thursday

- The DMO announced earlier this morning that it would be looking to hold a tender on Thursday this week for a potential conventional sub-5 year gilt.

- We note that already in this fiscal year the 0.125% Jan-26 gilt (ISIN: GB00BL68HJ26) has been reopened via tender twice for GBP2.0bln in September and November.

- This gilt is still trading at a premium to the rest of the curve (even when taking into account its low coupon) and we think that there is still strong demand for this gilt in the market.

- We think the market agrees with our assessment as the 0.125% Jan-26 gilt is underperforming similar gilts around a similar maturity this morning.

- In terms of the size, there is only GBP2.6bln remaining in the unallocated bucket and we still have a 10-year syndication of GBP8.5bln and linker syndication of GBP4.5bln remaining this year. Given this tender and those two remaining syndications, we think it looks unlikely the linker syndication will be upsized if we see a sizeable tender this week, but still see a change of the 10-year syndication being increased to GBP10.0bln.

- If the DMO wanted to leave the option to upsize the 10-year syndication, the maximum size of the tender would be around GBP1.25bln nominal. With the two tenders being for GBP2.0bln, however, there is the chance of a larger size.

- We therefore pencil in a GBP1.0-2.0bln size for this week's transaction. Note that there is no PAOF applicable to gilt tenders.

- The DMO is open for consultation comments until 15:30GMT today and will make an announcement regarding the timing and size of the tender at 7:30GMT tomorrow.

Corrected to say "underperforming" rather than "outperforming" this morning.

GILT AUCTION PREVIEW: Potential short-dated conventional gilt tender Thursday

- The DMO announced earlier this morning that it would be looking to hold a tender on Thursday this week for a potential conventional sub-5 year gilt.

- We note that already in this fiscal year the 0.125% Jan-26 gilt (ISIN: GB00BL68HJ26) has been reopened via tender twice for GBP2.0bln in September and November.

- This gilt is still trading at a premium to the rest of the curve (even when taking into account its low coupon) and we think that there is still strong demand for this gilt in the market.

- We think the market agrees with our assessment as the 0.125% Jan-26 gilt is underperforming similar gilts around a similar maturity this morning.

- In terms of the size, there is only GBP2.6bln remaining in the unallocated bucket and we still have a 10-year syndication of GBP8.5bln and linker syndication of GBP4.5bln remaining this year. Given this tender and those two remaining syndications, we think it looks unlikely the linker syndication will be upsized if we see a sizeable tender this week, but still see a change of the 10-year syndication being increased to GBP10.0bln.

- If the DMO wanted to leave the option to upsize the 10-year syndication, the maximum size of the tender would be around GBP1.25bln nominal. With the two tenders being for GBP2.0bln, however, there is the chance of a larger size.

- We therefore pencil in a GBP1.0-2.0bln size for this week's transaction. Note that there is no PAOF applicable to gilt tenders.

- The DMO is open for consultation comments until 15:30GMT today and will make an announcement regarding the timing and size of the tender at 7:30GMT tomorrow.