FOREX: FX OPTION EXPIRY

Of note:

EURUSD 7.33bn at 1.0750/1.0810.

USDJPY 1.22bn at 152.00.

USDCAD 1.16bn at 1.3810.

AUDUSD ~1bn at 0.6640/0.6650.

NZDUSD 1.55bn at 0.6070/0.6090.

EURUSD 1.65bn at 1.0800/1.0820 (fri).

AUDUSD ~1bn at 0.6660 (mon).

EURUSD 2.25bn at 1.0800 (tue).

USDJPY 2.29bn at 151.00/151.15 (tue).

USDCAD 5.05bn at 1.3800/1.3820 (wed).

- EURUSD: 1.0750 (1.17bn), 1.0755 (1.35bn), 1.0775 (629mln), 1.0780 (1.25bn), 1.0785 (1.01bn), 1.0800 (1.36bn), 1.0805 (340mln), 1.0810 (223mln), 1.0850 (772mln), 1.0865 (423mln), 1.0880 (379mln), 1.0900 (1.72bn).

- GBPUSD: 1.2900 (593mln).

- EURGBP: 0.8325 (275mln), 0.8340 (580mln), 0.8350 (286mln).

- USDJPY: 151.50 (751mln), 152.00 (1.22bn), 152.45 (401mln), 152.50 (255mln).

- USDCAD: 1.3810 (1.16bn).

- AUDUSD: 0.6605 (1.55bn), 0.6640 (667mln), .6650 (351mln).

- NZDUSD: 0.6075 (858mln), 0.6090 (700mln).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: PBOC Stimulus Boosts Equity Sentiment & Recovery for EURJPY

- Despite today’s poor German IFO data adding to the weaker-than-expected flash PMIs on Monday, the Chinese stimulus announcement overnight has boosted sentiment in equity markets, which in turn has provided support for the single currency, and in particular EURJPY (+0.80%).

- The cross briefly traded back above 161.00 in recent trade, from a 159.24 low overnight, and is now approaching the 50-day EMA at 161.73, an average we have not traded above since late July.

- EURUSD (+0.28%) has also been steadily grinding higher, rising back towards the US session highs from yesterday. Above here, 1.1169 is the high this week and a resumption of gains would refocus the market’s attention on 1.1202, the Aug 26 high and bull trigger.

- Countering the narrative is EURGBP, which continues to consolidate at depressed levels, following a range breakout to the downside during yesterday’s session. Alongside the breach of key support at 0.8383, we have also breached 0.8340 overnight, the Aug 2 ’22 low, placing the pair at the lowest level since April 2022.

- AUD would usually have thrived with today’s developments, however, with the RBA not discussing a rate hike at today’s meeting, the AUD (-0.04%) underperforms on the modestly dovish tilt.

- The USD index is little changed on the session, with just US consumer confidence on the data calendar. Potential comments from hawkish Fed dissenter Bowman will be monitored, while BoC Gov. Macklem participates in a fireside chat.

GILT TECHS: (Z4) Correction Extends

RES 4: 102.00 Round number resistance

- RES 3: 101.78 1.00 proj of the Sep 2 - 6 - 9 price swing

- RES 2: 101.06/101.54 High Sep 18 / 17

- RES 1: 99.88/100.39 20-day EMA / High Sep 19

- PRICE: 98.74@ 10:12 BST Sep 24

- SUP 1: 98.71 Intraday low

- SUP 2: 98.11 Low Sep 2 and a key support

- SUP 3: 98.00 Round number support

- SUP 4: 97.30 1.236 Fibonacci retracement proj of the Sep 2 - 17 rally

A bull cycle in Gilt futures remains intact, however, the sell-off that started Sep 7, highlights a corrective phase and this week’s move lower suggests potential for a continuation near-term. Support at 98.92, 76.4% of the Sep 2 - 17 bull leg, has been cleared and this strengthens the current bearish theme. The break exposes the key support at 98.11, the Sep 2 low. For bulls, a reversal higher would refocus sights on 101.54, Sep 17 high.

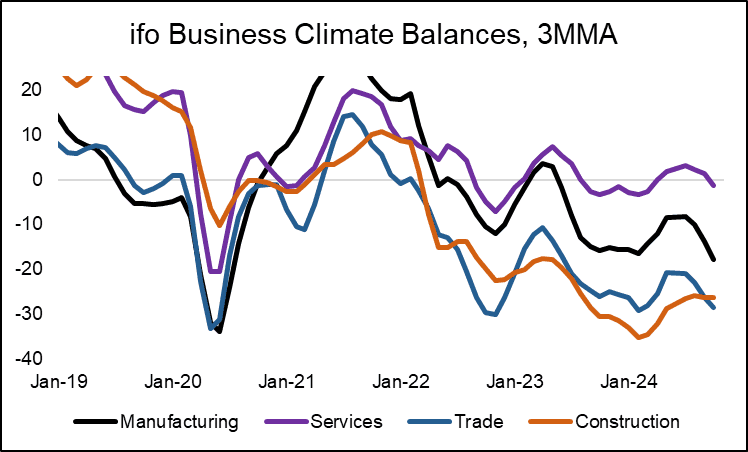

GERMAN DATA: IFO September Details Suggest Further Industrial Decline Ahead

The details behind the September's IFO survey suggest that the decline in the manufacturing sector is set to continue. Sentiment deterioration was quite broad-based, as demonstrated by the below chart of 3-month averages.

- Manufacturing: current assessment -21.5 vs -17.8, expectations -21.7 vs -17.9. The overall climate (-21.6 vs -17.8) is now significantly worse than when it bottomed out during late 2023/early 2024 ("cycle" low at -17.2 Dec-23). This aligns with IWK's Demary pointing to structural under-investment as a main driver behind the decline in a recent interview with MNI (MNI INTERVIEW: VW Crisis Should Be Wake-Up Call - IWK's Demary', MNI, September 18).

- Services: the only main sector with the current assessment in expansionary territory (+6.5 vs +12.3), although expectations remained negative (-13.0 vs -14.0) to tilt the overall climate balance back into negative territory.

- Trade: current assessment -25.3 vs -24.4, expectations -34.2 vs -30.3. On a 3mma measure, the sector now prints close to its initial pandemic fallout, with the climate index of -28.4 vs lows of -33.1 at the depths of the pandemic.

- Construction: stabilized recently but at a very low level with current assessment -18.9 vs -18.3, expectations -31.2 vs -34.8.