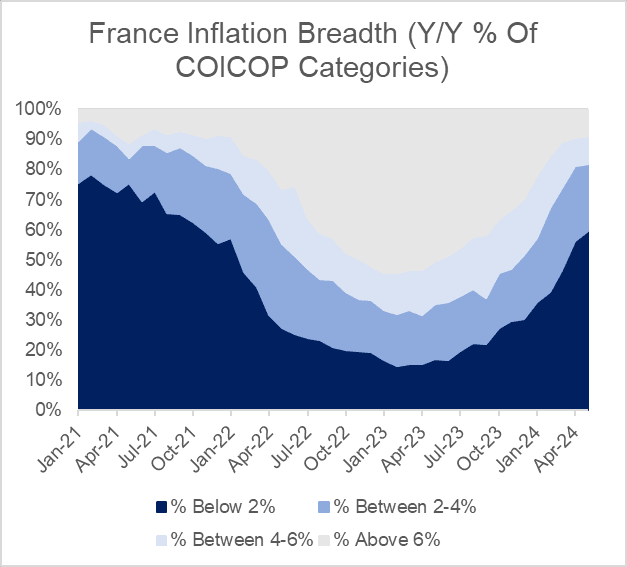

FRANCE DATA: Final HICP Breadth of Disinflation at Highest Since Oct'21

Final HICP data for May came in a touch softer than flash on an annual basis at +2.6% Y/Y (vs +2.7% flash, +2.4% prior), the non-seasonally adjusted M/M figure also came in slightly softer than flash at +0.1% (+0.2% flash, +0.6% in April). Recall that the flash French Y/Y print was 0.1pp above-expectation.

- This was a mixed report: as was suspected from flash release, the lesser extent of slowdown in CPI was driven by Services, although overall slowdown continues to be driven by both core and non-core components.

- Annual CPI came in a touch higher than flash at +2.3% Y/Y (+2.2% flash, +2.2% prior) although on a M/M basis it confirms flash at 0.0% (vs +0.5% prior) - the difference in evolution between HICP and CPI is due to the drop in reimbursements in the health sector and the change in energy prices.

- Looking at the breakdown of national CPI:

- Core inflation fell to +1.7% from +1.9% in April.

- Services fell less than anticipated from flash printing +2.8% Y/Y in May (+2.7% flash, +3.0% in April). The slowdown was due to transport services prices slowing to +0.2%Y/Y from +0.6%.

- Energy prices came in slightly softer than flash at +5.7% Y/Y (+5.8% flash, +3.8% in April)., the rise was due to base effects.

- Looking at the breadth of HICP inflation, MNI's analysis shows that the proportion of components with inflation below 2% continue to rise from 56% to 60% in May - the highest proportion since October 2021. Meanwhile, the proportion of components with inflation above 6% remained sticky at 9% from 9.4% in April - although this is the lowest level since October 2021.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Ratio call spread buyer

ERU4 96.62/96.87cs 1x1.5, bought the 1 for ~1.75 in 10k.

RIKSBANK: Minutes: Single-month Inflation Readings Downplayed

Interestingly, several members stressed that individual monthly inflation outcomes were not key determinants of the direction of monetary policy (e.g. Thedeen: “if CPIF inflation overshoots or undershoots the target by one or a couple of tenths of a percentage point in individual months, this should not in itself affect our plans for conducting monetary policy”).

- We read this as an attempt to temper market expectations for future rate cuts following soft individual inflation readings. A reminder that the May cut was supported because March inflation (the sole reading between the March and May Riksbank meetings) undershot the Riksbank’s forecasts significantly.

- As such, it provides support to our assessment that today’s inflation reading (which was a touch below consensus forecasts) does not change the picture much re: a possible June cut, given we will receive another inflation reading before the June meeting and the Riksbank’s guidance suggests the bar to cut in consecutive meetings is already quite high.

- Finally, Breman and Bunge affirmed that the Riksbank’s analysis into the long-run size of the balance sheet will come later this year.

FOREX: FX OPTION EXPIRY

FX OPTION EXPIRY (closest ones):

Of note:

USDJPY 1.09bn at 156.00.

AUDUSD 1.51bn at 0.6600.

USDCNY 1.13bn at 7.2000 (thu).

EURUSD 1.93bn at 1.0850 (fri).- EURUSD; 1.0795 (373mln), 1.0800 (504mln), 1.0825 (767mln), 1.0850 (724mln), 1.0900 (478mln).

- USDJPY: 156.00 (1.09bn).

- USDCAD: 1.3630 (341mln), 1.3650 (220mln).

- AUDUSD: 0.6600 (1.51bn).

- USDCNY: 7.20 (572mln), 7.23 (311mln).