BONDS: EUREX ROLLS

May-24 10:21

- It is still too early for EUREX roll, but it will be the next contracts to start to roll into the September expiry, expect that late next week.

- Buxl: Neutral.

- Bund: Mildly Bullish.

- Bobl: Bullish.

- Schatz: Neutral.

- BTP: Mildly Bearish.

- OAT: Mildly Bearish.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US 10YR FUTURE TECHS: (M4) Bearish Trend Condition

Apr-24 10:21

- RES 4: 109-25 50-day EMA

- RES 3: 109-26+ High Apr 10

- RES 2: 108-26 20-day EMA

- RES 1: 108-22+ High Apr 19

- PRICE: 107-26 @ 11:06 BST Apr 24

- SUP 1: 107-13+ Low Apr 16

- SUP 2: 107-07+ 76.4% of the Oct - Dec ‘23 bull leg (cont)

- SUP 3: 106-27 2.764 proj of Dec 27 - Jan 19 - Feb 1 price swing

- SUP 4: 106-08 3.00 proj of Dec 27 - Jan 19 - Feb 1 price swing

Treasuries are trading lower today. The trend outlook is unchanged and the direction remains down. Last week’s move lower reinforces current conditions and the move down has resumed this year’s bear trend. Furthermore, moving average studies remain in a bear-mode set-up, highlighting a clear downtrend. Sights are on 107.07+ next, a Fibonacci retracement. Firm resistance is 108-26, the 20-day EMA.

LOOK AHEAD: Wednesday Data Calendar: Durable/Capital Goods, Tsy Auctions

Apr-24 10:18

- US Data/Speaker Calendar (prior, estimate)

- Apr-24 0700 MBA Mortgage Applications (3.3%, --)

- Apr-24 0830 Durable Goods Orders (1.3%, 2.5%)

- Apr-24 0830 Durables Ex Transportation (0.3%, 0.2%)

- Apr-24 0830 Cap Goods Orders Nondef Ex Air (0.7%, 0.2%)

- Apr-24 0830 Cap Goods Ship Nondef Ex Air (-0.6%, 0.2%)

- Apr-24 1130 US Tsy $30B 2Y FRN, $60B 17W Bill auctions

- Apr-24 1300 US Tsy $70B 5Y Note auction (91282CKP5)

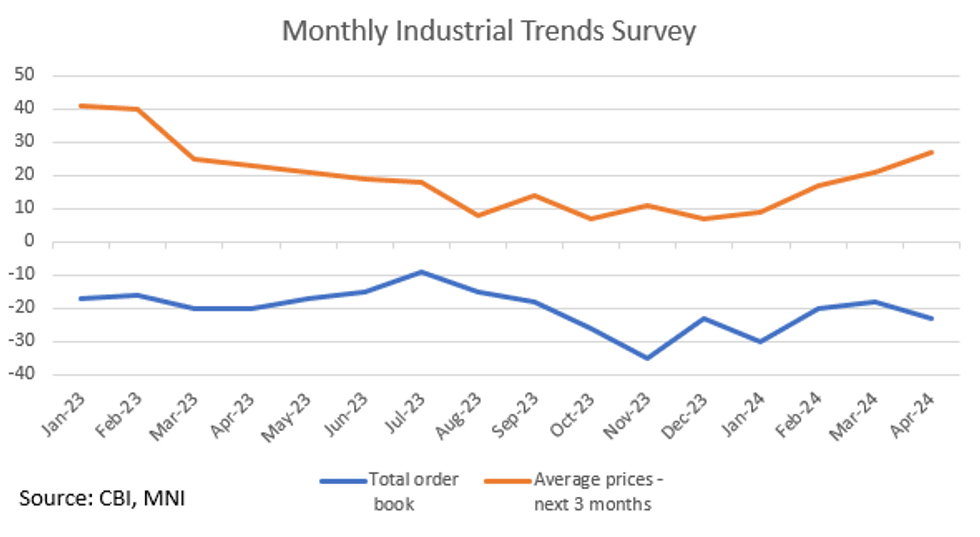

UK DATA: CBI Price Expectations Highest Since February 2023

Apr-24 10:13

UK CBI Order Books Balance fell to -23% (vs -18% prior) in April, the lowest level since January 2024, again remaining below the long run average of -13%.

- Expectations for average selling price for next three months picked up for the fourth consecutive month to 27% (from 21% in March) - making it the highest since February 2023, and again remaining higher than the long run average of 7%.

- The CBI surveys manufacturing firms and hence this will be of importance to the part of non-energy industrial goods (NEIG) that is domestically produced. This sustained pickup in average selling price expectation will be concerning to the MPC, particularly as NEIG inflation has been easing recently (while services inflation has remained more sticky). If NEIG starts to stabilise, rather than disinflating, services inflation may need to be lower to get inflation sustainably back to target.

- Survey conducted between 25 March and 12 April, with 257 manufacturing firms responding.