POWER: EU Mid-Day Power Summary: CWE Climb

Aug-22 11:46

CWE German September is rising slightly amid small gains in TTF and above seasonal temperatures heading into next month, while France is being supported by possible nuclear curtailment surrounding river levels and the likelihood of additional exports to Switzerland amid extended nuclear works at the Gosgen.

- Nordic Base Power SEP 25 down 1.7% at 37.35 EUR/MWh

- France Base Power SEP 25 up 0.3% at 51.16 EUR/MWh

- Germany Base Power SEP 25 up 0.5% at 86.27 EUR/MWh

- EUA DEC 25 down 0.3% at 72.41 EUR/MT

- TTF Gas SEP 25 up 0.5% at 33.35 EUR/MWh

- TTF front month is set for a net gain on the week, reaching the highest since Aug. 6 at €33.5/MWh amid supply concerns. Seasonal maintenance in Norway is to ramp up next week, while hope of a Ukraine ceasefire has reduced through the week.

- EUAs/UKAs Dec25 are on track for a 2.57% and 3.11% and weekly gain, supported by over 8% gains in TTF amid supply concern with seasonal maintenance in Norway to ramp up next week.

- EdF has extended the planned outage at its 1.33GW Penly 2 nuke to 24 August from 21 August, latest Remit data show.

- The 1.31GW Belleville 2 started its planned works on 23 August, with the unit disconnected until 26 November.

- The six-month delay in restarting the 1.02GW Gosgen nuclear power plant is due to extended verification work with newly applied calculation methods for its feedwater system.

- The completion of the Aurora Line at the turn of 2025–26 will lift transmission capacity between Finland and northern Sweden to 1.9GW in both directions. At the same time, it will increase the fixed safety margin to 200MW from 100MW.

- Greece is reviewing whether to extend deadlines for 900MW of battery projects, with the first major milestone for around 700MW from the initial two auctions set for 30 September.

- Nuclearelectrica has signed a €175mn contract with Arabelle Service France to refurbish the turbo generator at the 700MW Unit 1 of Romania’s 1.4GW Cernavoda nuclear power plant.

- The UK planning Inspectorate has accepted the 800MW Great North Road solar and biodiversity park near Newark-on-Trent for examination.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: AUD Uptick Firms Further on Break of $0.66

Jul-23 11:46

- AUD clearing 0.6600 at typing, with the uptick accelerating on the break of a cluster of resistance into 0.6595. Above here, resistance is scant until 0.6688, the Nov 07 high, printed shortly after the US election last year. Additionally, 0.6700 represents the 76.4% retracement of the Sep 30 '24 - Apr 9 bear leg.

OUTLOOK: Price Signal Summary - Gilts Remain Above recent Lows

Jul-23 11:45

- In the FI space, Bund futures traded higher again, on Tuesday. This week’s gains have resulted in a move through resistance around the 50-day EMA, at 130.24. The clear break of the EMA undermines a recent bear theme and highlights a possible reversal. Sights are on 130.85 61.8% of the Jun 13 - Jul 14 bear leg. A break of this level would open 131.33, the Jun 20 high. Key support and the bear trigger has been defined at 129.08, the Jul 14 low.

- Gilt futures traded sharply higher on Tuesday, extending the recovery from the Jul 18 low. The contract has breached the 20-day EMA, strengthening a bullish theme and this undermines the recent bearish condition. A continuation higher would signal scope for a climb towards 92.42 next, a 50.0% retracement of the Jul 1 - 18 bear leg. On the downside, key support and the bear trigger has been defined at 91.08, the Jul 18 low.

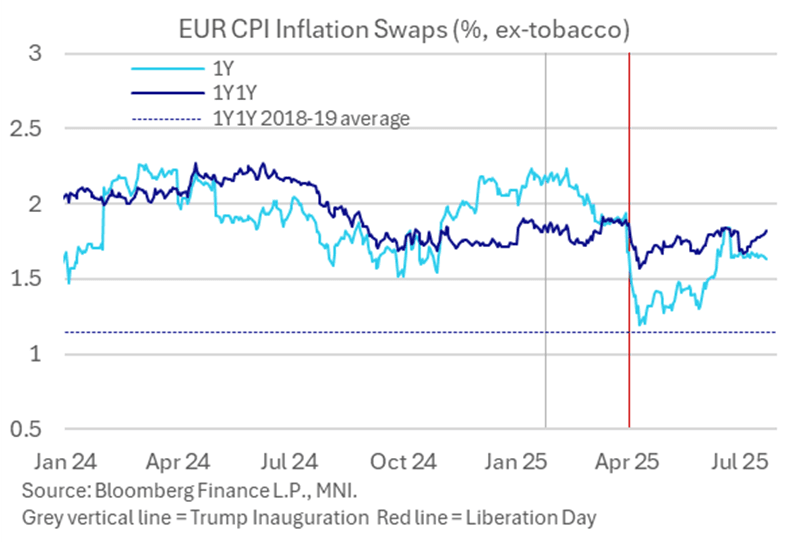

EGBS: Growth Concerns Modestly Outweigh Inflation Aspects Of Tariff Retaliation

Jul-23 11:42

- EGBs see the growth negative angle outweighing higher near-term inflation risks on the potential US-EU trade escalation as Bloomberg reports the EU plans to react with 30% tariffs of its own if no deal.

- German 2Y yields are almost 1bp lower post headlines but still +0.4bp on the day. The curve holds its modest steepening with 2s10s at 79.7bp (+1.1bp on the day).

- EUR 1Y CPI ex-tobacco inflation swaps are also holding lower, at 1.63% (-1bp on the day), although the 1Y1Y at 1.82% is at its highest since late June and having last been more clearly higher prior to early April US reciprocal tariff announcements.