EQUITIES: EU Cash opening calls

Aug-04 06:56

Estox 50: +0.46%, Dax: +0.37%, CAC: +0.48%, FTSE +0.08%, SMI +0.08%.

- So looking for a positive open this morning, still doesn't recover anything near the 218 points fall seen this week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: EU Cash opening calls

Jul-05 06:56

- Estox 50: -0.55%

- Dax: -0.64%

- CAC: -0.40%

- FTSE -0.39%

- SMI -0.23%

USDCAD TECHS: Resistance Holds - For Now

Jul-05 06:55

- RES 4: 1.3427 High Jun 7

- RES 3: 1.3365 50-day EMA

- RES 2: 1.3355 High Jun 15

- RES 1: 1.3269/86 20-day EMA / High Jun 29

- PRICE: 1.3240 @ 07:54 BST Jul 5

- SUP 1: 1.3190/3117 Low Jun 28 / 27 and key support

- SUP 2: 1.3084 1.618 proj of the Apr 28 - May 8 - May 26 price swing

- SUP 3: 1.2992 50.0% retracement of the Jun - Oct 2022 bull rally

- SUP 4: 1.2954 Low Sep 13 2022

USDCAD is holding on to its most recent gains. The latest recovery still appears to be a correction and the trend is bearish. Looking at MA studies, they remain in a bear mode position, highlighting a downtrend. A resumption of weakness would open 1.2992, a Fibonacci retracement. On the upside, firm resistance is seen at 1.3269, the 20-day EMA. It has been pierced, a clear break would expose the 50-day EMA, at 1.3365.

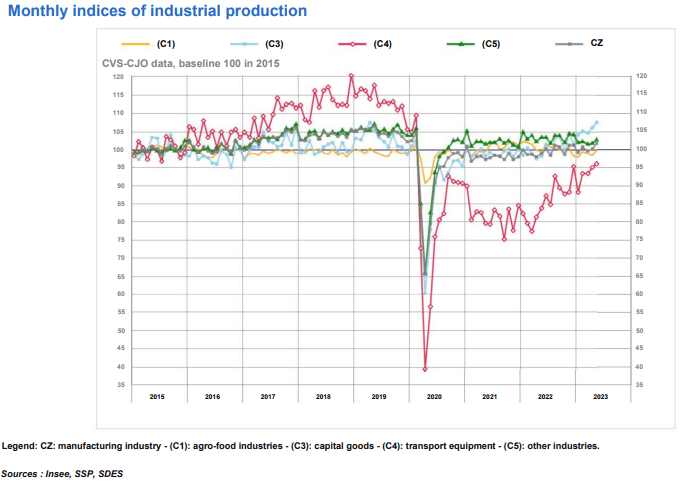

FRANCE DATA: Upside Surprise in Robust May Industrial Production

Jul-05 06:45

FRANCE MAY INDUSTRIAL PROD +1.2% M/M (FCST -0.2%); APR +0.8% M/M

FRANCE MAY INDUSTRIAL PROD +2.6% Y/Y (FCST +0.6%); APR +1.7%r Y/Y

- Kicking off the round of major eurozone May IP data, French industrial production beat expectations, posting a healthy +1.2% m/m increase against expectations of a -0.2% m/m contraction.

- With strikes at refineries easing, coking and refining production jumped markedly by +45.1% m/m (after +22.1% in April). Further rebounds were recorded in auto (+5.8% after -1.7%) and agro-food industries (+1.5% after -0.5%).

- Barring a pronounced June contraction, French IP now looks likely to post a positive contribution to Q2 q/q GDP.

- At +2.6% y/y, 2023 June IP was substantially stronger than this time in 2022.

- Yet Insee flagged that certain energy-intensive branches continue to struggle with high energy prices. March to May production for steel was down -19.1% y/y, paper down -24.2% y/y and chemicals down -13.1% y/y.

- The French manufacturing PMI has been in contractive territory since January, and continually deteriorating new orders imply a negative outlook for the industry in months to come.