US STOCKS: Equity Roundup: Real Estate, Materials and Financials Leading

Sep-30 16:01

Stock indexes trading steady/mixed, respite from midweek selling with SPX near middle of range, Real Estate, Materials and Financial shares outperforming ahead midday. Currently, SPX eminis trade steady at 3654.25 vs. 3627.0 low; DJIA -89.82 (-0.31%) at 29133.44; Nasdaq +46.4 (0.4%) at 10783.74.

- S&P E-Minis trend conditions remain bearish and short-term gains are considered corrective. Moving average studies are in a bear mode position, highlighting the current trend direction. Attention is on key support at 3657.00, Jun 17 low. it has been pierced. A clear break would strengthen bearish conditions and confirm a resumption of the broader downtrend. This would open 3600.00. Initial firm resistance is 3936.25, Sep 20 high.

- SPX leading/lagging sectors: Real Estate (+1.41%), Materials (+1.2%) and Financials (+0.94%) outperforming, banks outpacing diversified financials and insurance companies. Laggers: Utilities (-0.56%), Consumer Staples (-0.2%) and Consumer Discretionary (+0.16%) underperformed, the latter weighed by consumer durables and apparel.

- Dow Industrials Leaders/Laggers: United Health (UNH) rebounds from midweek sell-off +6.71 at 515.54, Goldman Sachs (GS) +4.42 at 300.53, Microsoft (MSFT) +2.67 at 240.17. Laggers: Nike (NKE) hammered on poor earnings/inventory glut (NKE) -10.33 at 85.0, Walmart (WMT) -0.54 at 131.71.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: BLOCK, Another Sep Quarterly Sale

Aug-31 15:57

- -7,500 SFRU2 96.775 (+0.0075), post-time bid at 1154:32ET adds to 7.5k sold earlier same level

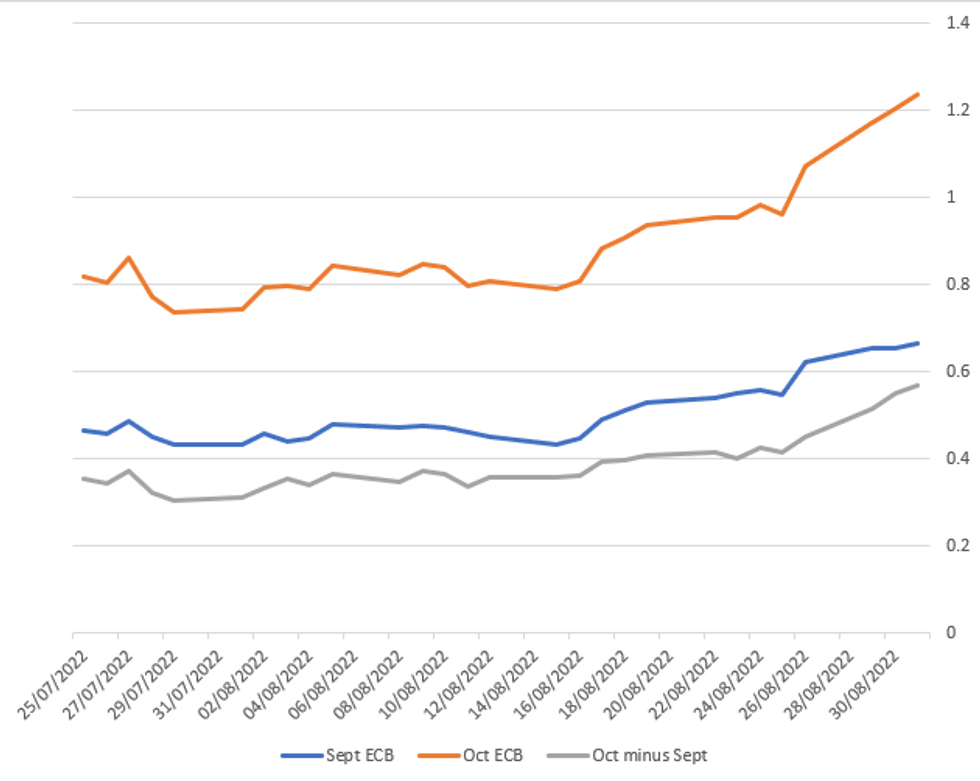

ECB: Analysts, Market Pricing Increasingly Eye 75bp September Hike

Aug-31 15:57

BofA, Credit Suisse, Goldman, and Nordea (and potentially others?) have upped their calls today for next week's ECB meeting, and are now looking for a 75bp hike.

- Futures haven't fully priced in a 3/4 point raise. The market is pricing 66-67bp (high of 68bp today) for September, with around 124bp through the October ECB (high of 125bp today).

- Pre-Jackson Hole last Thursday, pricing was for 96bp in cumulative Sep plus Oct hikes, with 55bp priced for September alone.

US TSY FUTURES: BLOCK, 30Y-Ultra Bond Sale

Aug-31 15:44

Example of how thin market depth can be in midday summer trade: Long end shifts lower after latest Ultra-bond block sale:

- -2,575 WNZ2 149-29, sell through 150-02 post-time bid at 1135:39ET, 149-25 last (-21)