EUROZONE ISSUANCE: EGB Supply

Italy looks to hold an auction today while the Netherlands, Finland, and Germany have already held auctions this week and the EU has held a syndication. We pencil in estimated gross issuance for the week at E22.2bln, down from E31.3bln last week.

- Italy will conclude the week this morning by holding a 3/7/15/25-year BTP auction. On offer will be E3.5-4.0bln of the new 3-year 3.45% Jul-27 BTP (ISIN: IT0005599904), E2.0-2.5bln of the 3.45% Jul-31 BTP (ISIN: IT0005595803), E1.0-1.25bln of the 4.15% Oct-39 BTP (ISIN: IT0005582421) and E1.0-1.25bln of the 3.85% Sep-49 BTP (ISIN: IT0005363111).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EUROZONE ISSUANCE: EGB Supply

The EU and Italy have both announced syndications while the Netherlands, Germany, Spain and France are all due to hold auctions in the upcoming week while the EU is scheduled to hold a syndication. There is also the possibility of further syndications with Austria and the ESM (or possibly EFSF) as the most likely further candidates to hold transactions in our view. We pencil in estimated gross issuance for the week at E43.5bln, up from E19.8bln last week.

- The EU has a syndication scheduled for today with a new 30-year Oct-54 EU-bond on offer (ISIN: TBC). We look for a transaction size of E7-8bln.

- We had been unsure of whether the EU would choose to launch a new conventional 15-year or a new 30-year. Given that we have had the launch of the new 30-year announced for this week, we now expect the next syndication (W/C 10 June) to see a new conventional 15-year EU-bond launched.

- Italy will also come to the market in the “near future” (we expect today) week to launch a short long 15-year Oct-37 BTP Green (ISIN: TBC). Italy plans green issuance for 2024 of E11.5-13.5bln and has already sold E1.25bln. This seems to suggest that there would be an absolute upper limit of E10bln for the transaction today. If the MEF prefers to keep its options open for more than one further green auction later this year, it would suggest a slightly smaller transaction size today. We pencil in a rather wide E6-10bln range with around E7bln the most likely size in our view.

- We had noted on Friday that we thought the next Italian syndication could be brought forward given the lower-than-expected take up in last week’s BTP Valore. We had thought a 2040 BTP Green would be more likely than a 2037 maturity, however, given the gaps in the green curve.

- The Netherlands will kick off auctions for the week this morning with E1.5-2.0bln of the off-the-run short 5-year 0% Jan-29 DSL (ISIN: NL0015000LS8) on offer.

- Also this morning, Germany will come to the market to look to sell E5bln of the 2.90% Jun-26 Schatz (ISIN: DE000BU22056).

UK DATA: Labour Market Data Due at 7:00BST

- With the MPC last week deemphasising labour market data somewhat, we have looked at what it could take to trigger an upside surprise to the BOE's new private sector regular pay forecasts - and possibly derail a June cut.

- We find that without revisions it would take a huge increase in the single month private regular AWE numbers to the highest level since September 2023 to exceed the Bank's 6.0%Y/Y forecast in the 3-months to March.

- Even with a 0.1ppt upward revision to February's single month print, March's single month figure would have to be higher than December's.

- So overall, to get an upside surprise to the BOE's forecast is actually quite difficult without changing the narrative around the labour market.

- From the analyst previews we have read, the median expectation is for private regular AWE to increase 5.9%Y/Y - a tenth lower than the BOE's forecast.

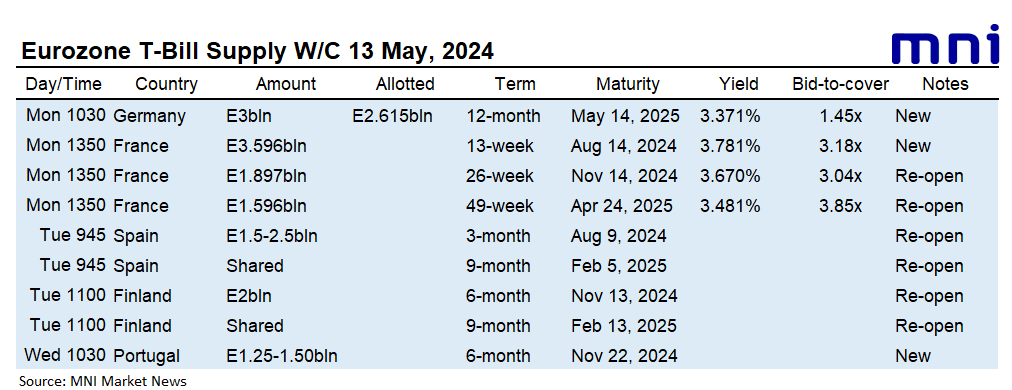

EUROZONE T-BILL ISSUANCE: W/C May 13, 2024

Spain, Finland and Portugal are due to sell bills this week, while Germany and France have already come to the market this week. We expect issuance to be E15.7bln in first round operations, down from E30.8bln last week.

- This morning, Spain will look to sell a combined E1.5-2.5bln of the 3-month Aug 9, 2024 letras and the 9-month Feb 5, 2025 letras.

- Also today, Finland will look to come to the market with up to a combined E2bln of the 6-month Nov 13, 2024 RFTB and the 9-month Feb 13, 2025 RFTB.

- Finally tomorrow, Portugal will look to sell a combined E1.25-1.50bln of the new 6-month Nov 22, 2024 BT and the new 12-month May 16, 2025 BT.

For more on future auctions see the full MNI Eurozone/UK T-bill auction calendar here.

For more on future auctions see the full MNI Eurozone/UK T-bill auction calendar here.