EUROZONE ISSUANCE: EGB Supply

Nov-09 06:51

Italy is still due to issue tomorrow while Austria and Germany have already come to the market this week. We pencil in gross nominal issuance of E14.3bln, down from E34.5bln last week.

- Italy will look to conclude issuance for the week on Friday with a 3/7/15/30-year BTP auction. On offer will be E2.5-3.0bln of the 3-year on-the-run 3.85% Sep-26 BTP (ISIN: IT0005556011), E1.0-1.5bln of the off-the-run 7-year 3.50% Mar-30 BTP (ISIN: IT0005024234), E1.5-2.0bln of the 7-year on-the-run 4.00% Nov-30 BTP (ISIN: IT0005561888), E1.0-1.5bln of the 25-year 3.25% Mar-38 BTP (ISIN: IT0005496770) and E0.75-1.0bln of the on-the-run 30-year 4.50% Oct-53 BTP (ISIN: IT0005534141).

For more on this week and next week's supply see the PDF here:

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Equities fade, USD leans in the green

Oct-10 06:38

- The Dollar is closer to flat against the CHF, SEK, AUD, EUR, while CAD, GBP, NZD and Yen are 0.10% to 0.14% down going into the European session.

- The NOK is the worst performer, now down 0.39% and off its worst level, following the lower CPI.

- Risk On has faded since the EU Cash Govie open, Estoxx futures (VGZ3) might be showing in the green, but the contract has still failed to close Yesterday's downside gap, up to 4183.00.

- This, still remains the first initial retracement level.

- On the other side of the Atlantic, Emini is also fading into the EU session, but the contract did manage to fully close Yesterday's gap, and still trading above that level today.

- Next resistance in ESZ3 is seen at 4399.00.

SWEDEN: Monthly GDP Indicator Falls in August

Oct-10 06:37

Swedish monthly GDP figures for August came in just below consensus at -0.2% M/M (vs -0.1% cons; a revised +0.8% prior) and +0.3% Y/Y (vs -0.3% prior).

- The press release notes that the print was pulled down by strong imports of goods, while consumption lost momentum relative to the summer months.

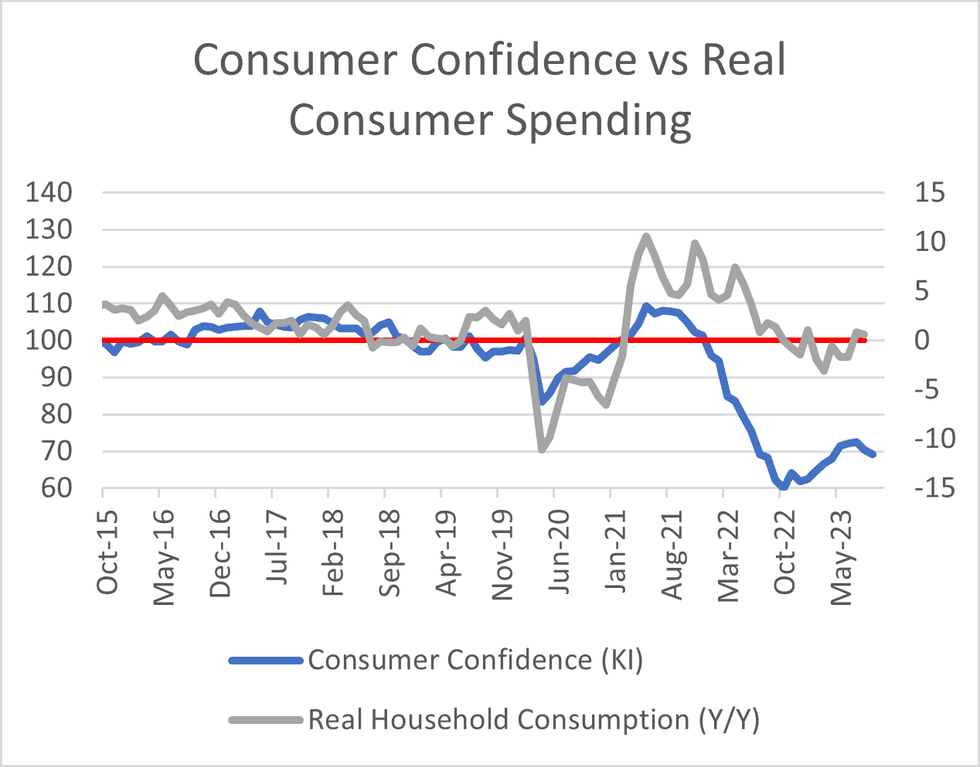

- Household consumption was +0.5% M/M and +0.6% Y/Y (vs +0.6% M/M and +0.8% Y/Y in July respectively). As with prior months, hard consumption data continues to hold up better than the extremely negative consumer confidence prints in the Economic Tendency Indicator.

- On a Y/Y basis, overall production recovered somewhat, with private sector production +0.7% Y/Y (vs -2.2% prior), services production 0.6% Y/Y (vs +0.6% prior) and industrial production +4.7% Y/Y (vs -5.1% prior).

- Further details on the drivers of each component have not yet been released.

NORWAY: Fairly broad-based fall in inflation

Oct-10 06:30

- The slowdown in Norwegian inflation looks fairly broadbased.

- Consumer goods prices fell -0.3%M/M to +1.8%Y/Y. That's the lowest Y/Y print since 2020 and down from +4.3%Y/Y in August and down from a peak of +10.7%Y/Y in October 2022.

- Services ex-rent rose +0.1%M/M but the Y/Y print fell to 5.7%Y/Y versus +6.3%Y/Y prior, the lowest Y/Y print this year, and down from a peak of +6.9%Y/Y in February.

- Energy also came in probably a bit lower than expected, falling -10.5%M/M (-34.6%Y/Y).

- Rents remained broadly steady at +4.2%Y/Y.