EUROZONE ISSUANCE: EGB Supply (1/2)

The EFSF is likely to hold a syndicated transaction in the upcoming week. Germany, Spain and France are due to hold auctions in the week. Belgium will hold an ORI operation as well as closing its latest Bons d’ Etat retail offering during the week. We pencil in issuance of E30.3bln for the week (excluding retail) up a little from E29.5bln this week.

- The EFSF sent an RFP (Request for Proposal) on Wednesday regarding an upcoming transaction. That means a transaction is likely in the upcoming week (MNI pencil in Monday or Tuesday). We had initially expected an EFSF transaction in either late August or by mid-September (September had looked likely after the ESM RfP was released on Wednesday 20 August). On size, E3bln could be expected (which would complete the EFSF's funding needs for 2025). There is a chance of a smaller E2bln transaction with a further E1bn sold later this year, but that seems a less likely option to us.

- Germany will kick off issuance for the week on Tuesday, selling E4.5bln of the 1.90% Sep-27 Schatz (ISIN: DE000BU22106).

- Germany will return to the market on Wednesday, with E5bln of the 10-year 2.60% Aug-35 Bund (ISIN: DE000BU2Z056) on offer.

- Also on Wednesday, the subscription period for Belgium’s Bons d’ Etat is scheduled to close. Two lines will be on offer for retail investors: the 1-year 1.90% Sep-26 Bons d' Etat (ISIN: BE3871306366) and the 10-year 3.20% Sep-35 Bons d' Etat (ISIN: BE3871307372).

- After the first three days (to Thursday 28 August), E147.7mln of the 1-year and E40.5mln of the 10-year had been taken up.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

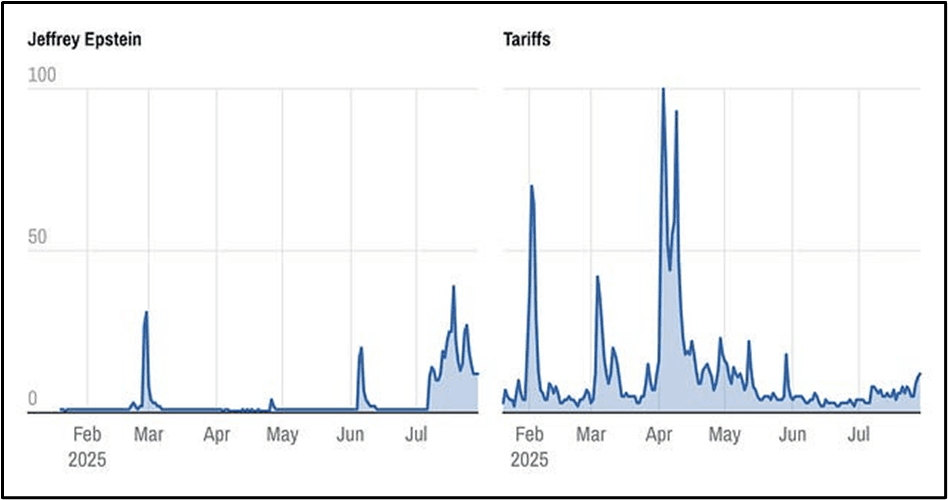

US: Epstein Case Unlikely To Signficantly Damage Trump Approval

Nate Silver at Silver Bulletin writes that despite the high volume of news reports about President Donald Trump's handling of the Jeffrey Epstein case, it may not resonate broadly enough with the electorate to impact Trump’s approval.

- Silver notes: “Google search traffic in the United States reveals that the peak of interest in the Epstein case a couple of weeks ago was only about one-third as high as the one surrounding tariffs in April. I know that might seem like an apples-to-oranges comparison, but tariffs are an interesting benchmark precisely because they’re one of the few things that did produce notable political fallout for Trump.”

- Silver adds: “There remains a strong case that voters are concerned about the economy and the cost of living, but that everything else is priced in.”

Figure 1: “Google search traffic for tariff and Epstein topics”

Source: Silver Bulletin

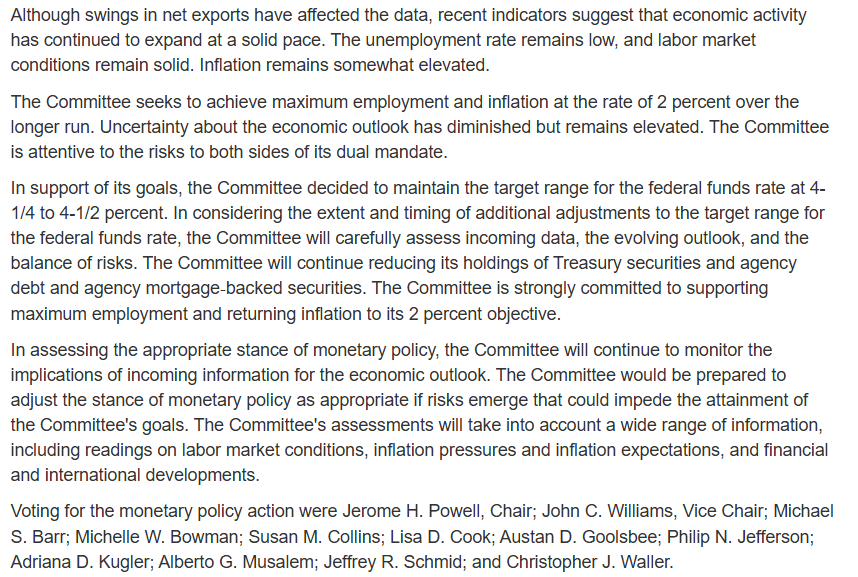

FED: Statement: Changes Seen Limited, With Growth Description And Dissents Eyed

The main focus for the 2pm FOMC Statement release will be the dissents to the (almost certain) decision to hold. The June Statement is in the image below.

- The opening paragraph of the Statement is often changed to reflect incoming data since the prior meeting, and July’s could clean up the language slightly.

- When GDP is released the morning of a Fed decision, the Statement usually reflects the outcome in the first sentence, which in June read "Although swings in net exports have affected the data, recent indicators suggest that economic activity has continued to expand at a solid pace." It's unclear whether that needs much of a change given the pickup in growth in Q2 vs Q1 was driven largely by inventory and net export "swings".

- If the Statement highlights the softening in final domestic demand this would be a dovish development, though it's more likely this will be mentioned by Powell in the press conference. The Statement is very likely to keep the description of labor market conditions as “solid”, and inflation as “somewhat elevated”, though a change to either would probably be a dovish tilt.

- The second paragraph will likely remove the reference to how uncertainty about the outlook “has diminished” but the rest of the language should remain intact, given how frequently Committee members used the term “uncertainty” in describing the current state of play.

- Finally, on dissents: This meeting is likely to have at least one and possibly two dissents: Vice Chair Bowman and Gov Waller have each expressed support for cuts to resume at this meeting. This would be the first time since 1993 that two Governors dissent.

- It could be taken as a hawkish surprise if there are no dissents, and perhaps even if there is just one dissent (Bowman the more likely to vote with the majority in our view). Likewise a third dissent in favor of a cut would be a major dovish surprise.

- Note that Gov Kugler is not participating at this meeting for personal reasons, so won't be mentioned in the vote at the end.

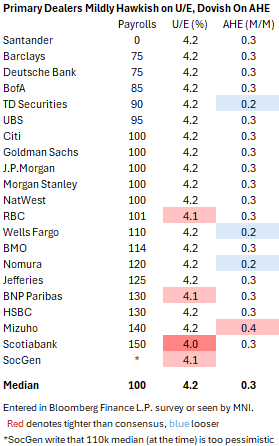

US LABOR MARKET: Payrolls Growth Seen Slowing Again After Public Sector Boost

- Nonfarm payrolls are expected at a seasonally adjusted 104k in July per the broad Bloomberg survey after a surprisingly resilient 147k in June which came along with rare upward revisions.

- The median primary dealer analyst eyes 100k whilst the Bloomberg whisper currently sits at 120k after little reaction to the stronger than expected ADP report for July.

- Government payroll growth is expected to be much softer after a surprise 73k surge in June, which we think was more likely down to seasonal adjustment quirks. There’s a wide range of primary dealer estimates for public payrolls growth in July, from +20k to -55k.

- Consensus sees private sector payrolls rising 100k after a disappointing 74k in June and the breadth of gains should again be watched. 59k of this came from the cyclically insensitive health & social assistance category, whilst roughly as many of the 250 industries increased on the month as those that decreased.

- Payrolls growth should continue to be viewed against long-run breakeven estimates of around the 100k mark although some, such as Deutsche Bank, see this potentially being as low as 50k owing to continued immigration curbs. Indeed, border encounters remain far lower than previous years, albeit plateauing since February, and ICE detention center populations have increased further.

- The unemployment rate is widely expected to tick up a tenth to 4.2% after a surprisingly low 4.11% in June as it pulled back from a cycle high of 4.244% in May. A faster-than-expected deterioration will be required for the final six months of the year to reach the FOMC's June Q4 median projection of 4.5%.

- AHE growth is widely expected at 0.3% M/M after a dovish surprise in June and hawkish surprise in May, which would see the Y/Y inch higher again after seven consecutive unrounded declines. Average hours worked should also be watched from an already low 34.2 in June.

- The full MNI Payrolls Preview will be published tomorrow morning to take into account of the upcoming FOMC decision and press conference.