AMERICAS OIL: Diesel options no longer appear to be in the lunatic fringe

Jul-25 17:23

Diesel options no longer appear to be in the province of the lunatic fringe: Kloza

- Tom Kloza posts on X, “with January ULSD ~$2.405/gal you can buy a $2.50/gal call option for ~11cts/gal.”

- “A $2.75gal call costs ~6cts/gal and a $3/gal call fetches 4cts/gal.”

- ULSD AUG 25 up 0.9% at 2.43$/gal

- US ULSD crack up 1.3$/bbl at 35.48$/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

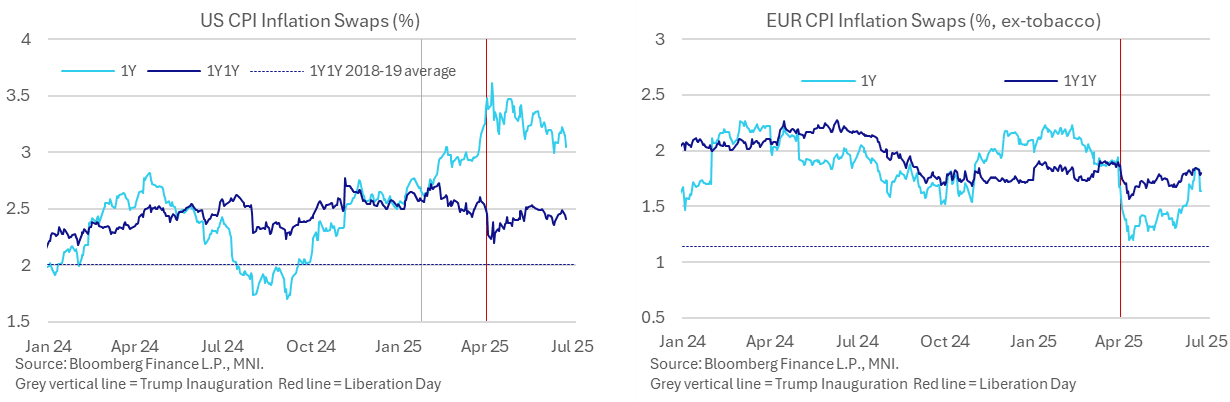

INFLATION: 1Y Inflation Expectations Trend Lower Whilst 1Y1Y Steady

Jun-25 17:10

- US 1Y market inflation expectations have been below levels just before US Liberation Day tariff announcements of Apr 2 for most of June although are trending lower.

- However, at 3.05%, these 1Y CPI inflation swaps are only back to late March levels and hold a large portion of the widening vs 1Y1Y expectations since President Trump’s inauguration.

- WTI futures plunged early this week on the limited Iranian response to US airstrikes on nuclear facilities and a subsequent Israel-Iran ceasefire. However, with the August contract at $66/bbl, it’s only back to mid-June levels and at the lower end of pre-tariff rough ranges of $65-70/bbl.

- This is something partly reflected by the recent pullback in surveyed short-term inflation expectations, including in yesterday’s Conference Board consumer survey, leaving them with mixed degrees of relative elevation (see here).

- It follows trade policy de-escalation but with further focus increasingly turning to further trade deal prospects ahead of the current 90-day window ending July 8th.

- EUR CPI swaps meanwhile have seen the opposite, with the 1Y pushing back towards pre-Apr 2 levels having dropped sharply on growth fears. There have however been warning shots recently as deliberations continue – no deal would see tariff rates of 50% on nearly all EU goods exports from July 9th.

- Specifically, Reuters last week reported that European officials are increasingly resigned to a 10% baseline rate on reciprocal tariffs in any US-EU trade deal. One of the sources, an EU official, said negotiating the level down had become harder since the U.S. started drawing revenues from its global tariffs. "10% is a sticky issue. We are pressing them but now they are getting revenues," said the official.

- Bloomberg yesterday then reported that the EU is planning to impose retaliatory tariffs on US imports, including on Boeing, if the US puts a baseline tariff on EU goods.

PIPELINE: Corporate Bond Update: $3B CaixaBank 3Pt Launched

Jun-25 17:09

- Date $MM Issuer (Priced *, Launch #)

- 06/25 $3B #CaixaBank $1B each: 4NC3 +90, 6NC5 +105, 11NC10 +130

- 06/25 $1.25B *Swedish Export Cr 2Y SOFR+35

- 06/25 $1B #Cheniere Energy +10Y +128

- 06/25 $750M *Resolution Life 10Y 6.75%

- 06/25 $Benchmark Welltower 5Y +95a, 10Y +115a

- 06/25 $Benchmark Honda 3Y +90a, 5Y +100a, 10Y +120a

- 06/25 $Benchmark Republic of Peru +10Y +125, 30Y +140

- 06/25 $1B Czechoslovak Grp 5.5NC2 6.5%a (dual currency w/ E1B)

US TSYS/SUPPLY: Review 5Y Auction: Tail

Jun-25 17:04

- Tsy futures retreat slightly (FVU5 to 108-20.75 from 108-21.5 at the cutoff) after the latest $70B 5Y note auction (91282CNK3) tailed: 3.879% high yield vs. 3.872% WI; 2.36x bid-to-cover vs. 2.39x prior (5 auction average).

- Peripheral stats: Indirect take-up retreats to 64.68% from 78.4% prior, directs rebound to 24.44% vs. 12.4% prior (5 auction low), primary dealer take-up at 10.88% vs. 9.2% prior.

- The next 2Y auction is tentatively scheduled for July 28.