EM CEEMEA CREDIT: Development Bank of Kazakhstan: $ BM L5Y – Final guidance

Oct-08 14:27

(DBKAZ: Baa2/BBB-pos/BBB)

IPT: 5.25%

FV: 4.90%

Final Guidance: 4.9% (+/-5)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED FUNDS FUTURES: BLOCK: Oct'25 FF Sale

Sep-08 14:26

- -12,000 FFV5 95.96, post time bid at 1019:19ET.

- The Oct'25 contract trades 95.955 last (-.005)

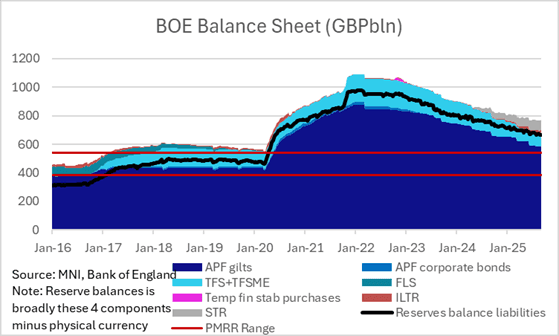

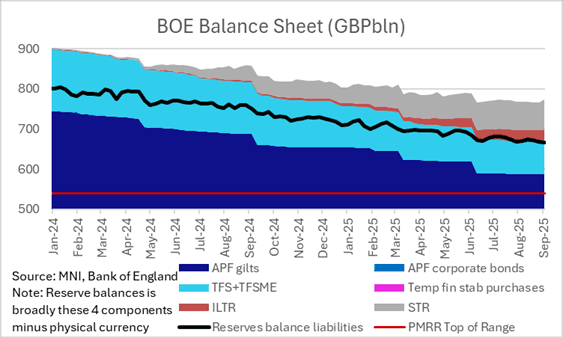

BOE: STR and ILTR operations post gilt redemption may impact 25/26 APF decision

Sep-08 14:06

- We will also be focusing on the take up of the STR and ILTR this week following the redemption of the formerly 10-year 2.00% Sep-25 gilt that has now matured.

- The BOE held GBP26.2bln of this gilt in nominal terms and will reduce the size of the APF holdings by GBP28.3bln in initial purchase terms.

- This follows a couple of weeks in which we have seen STR usage pick up by GBP9.6bln and ILTR usage pick up by GBP1.6bln.

- Together this means that demand-led balances have increased to GBP108.1bln (from the previous cycle peak of GBP102.2bln around 2 months ago.

- The market reaction will in our view will factor into the MPC’s decision on the size of the QT programme in the Oct’25 to Sep’26 period (which will be decided at the upcoming September MPC meeting).

- We favour keeping the pace of active sales broadly inline with the pace seen this year which would see around a GBP60-65bln target reduction in the size of the APF programme (including passive sales).

- We wrote more on this in July in BOE September APF Decision: What you need to know (see here).

US LABOR MARKET: MNI US Payrolls Preliminary Benchmark Revision Preview

Sep-08 14:02

We have published and e-mailed to clients the MNI Preview for tomorrow's preliminary benchmark revision to payrolls data. See the full note here: https://media.marketnews.com/US_Prelim_Benchmark2025_Preview_f1d718139b.pdf

- Tuesday’s preliminary annual payrolls benchmark revision is widely expected to imply large downward revisions to nonfarm payrolls growth through the twelve months to March 2025.

- We’ve seen estimates for a downward revision of at least 500k (using mid-point estimates when analysts quote a range) with a central guess of around -750k.

- History suggests the actual benchmark revision due with the Jan 2026 payrolls report will be smaller than what’s reported this week, but downward revisions could still be significant.

- Beware extrapolating these downward revisions beyond March 2025 after significant changes in the labor force since then.

- Also recall that last year saw issues in the publication of this preliminary estimate, with a late release.