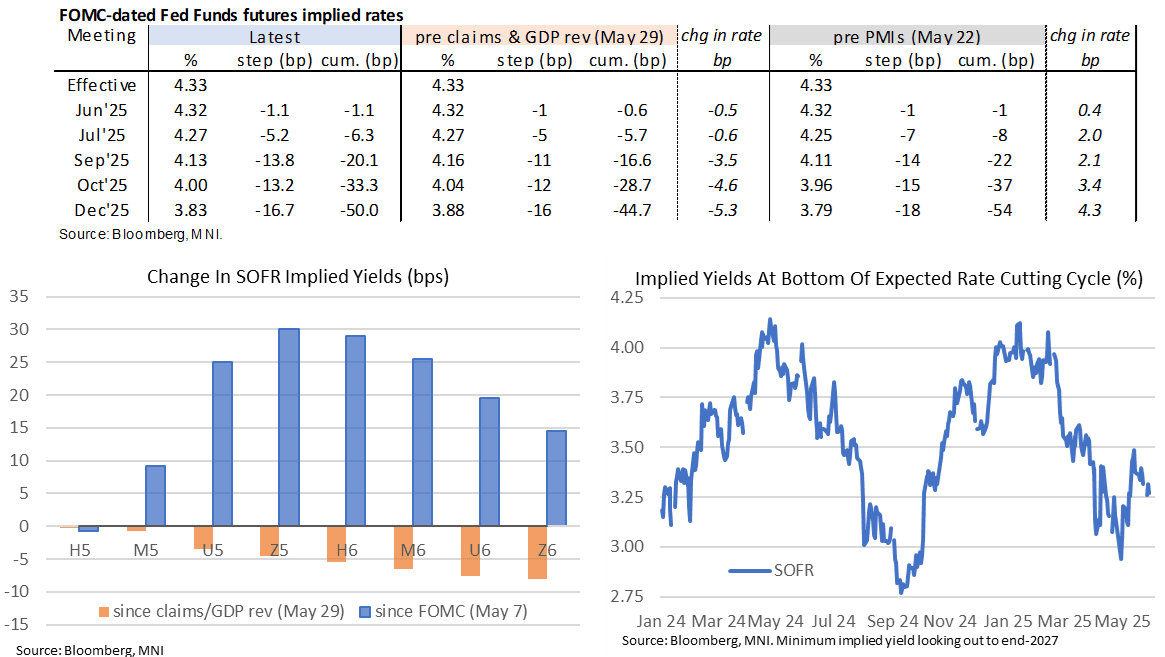

STIR: Cuts Pared But Still Only Fully Pricing Next Move In Oct

May-29 16:36

- Fed Funds implied rates are holding the large majority of today’s solid decline, although the path still only fully prices a next cut with the Oct FOMC and 50bp of cuts for what’s left of 2025.

- It’s a move that started ahead of 0830ET data with risk softening more broadly before accelerating on the surprisingly high jobless claims prints plus weak consumption in Q1 GDP revisions.

- Cumulative cuts from 4.33% effective: 1bp Jun, 6.5bp Jul, 20bp Sep, 32.5bp Oct and 50bp Dec.

- The SOFR implied terminal yield of 3.27% (SFRZ6) is now 4.5bp lower on the day, masking a 8bp decline since the 0830ET data and 11bp since US desks filtered in this morning. It swings back to the dovish end of the circa 100bp +/-5bp range of cuts from current effective rates seen over the past two and a half weeks.

- Ahead, Trump administration deliberations after the court ruling against the IEEPA approach to tariffs.

- Fedspeak follows with Gov. Kugler (permanent voter) at 1400ET but we don’t expect anything market moving there with just opening remarks. Dallas Fed’s Logan (’26 voter) could be more impactful but doesn’t speak until 0825ET.

- Tomorrow sees a solid data docket, with the April PCE report, advanced trade for April, MNI Chicago PMI and the final U.Mich consumer survey which will be watched after a tentative improvement was suggests in the preliminary release which wrapped up shortly after the US-China trade de-escalation on May 12.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SNB: Works Underway On Extended Liquidity Facility - Martin

Apr-29 16:30

The SNB is working on introducing a new liquidity support framework, centred on the Extended Liquidity Facility (ELF). The ELF encompasses [the previous] Extended Liquidity Assistance (ELA) and brings liquidity support closer to standard operations, SNB Vice Chairman Martin highlights today at a speech in Geneva.

- "A key objective of the ELF is to enhance banks' access to liquidity while reducing the stigma that can be associated with such support. It allows simplified access to limited liquidity volumes, while maintaining the same requirements as under ELA for larger volumes."

- "Regulatory efforts to strengthen banks' resilience to liquidity risk are also underway. Important initiatives include increasing banks' own liquidity provisions, introducing a minimum collateral requirement for central bank support, and anchoring a Public Liquidity Backstop in law. Together, these measures will enhance the ability of banks to withstand liquidity crises."

- "The SNB's emergency liquidity assistance (ELA) framework was first formalised in 2003, incorporating lessons learned from past financial crises. This framework established three conditions for liquidity assistance: only against sufficient collateral, only to solvent banks, and only to banks or groups of banks deemed relevant for financial system stability. In 2023 and 2024, the SNB publicly announced an expansion of its framework, extending access to liquidity support to all banks in Switzerland, using mortgages and securities as collateral."

- The previous ELA was used by Credit Suisse in March 2023, support totalled to CHF168bln, against collateral including mortgages and a federal guarantee. By the end of 2023, most loans under the scheme were repaid following the merger with UBS.

US DATA: Dallas Fed Services Pessimism Deepens

Apr-29 16:28

The Dallas Fed's Texas Service Sector Outlook Survey showed regional services firms' pessimism continued to deepen in April, echoing other regional Fed surveys for the month.

- The general business activity index fell to -19.4 ( -11.3 prior), an 18-month low. 6-month expectations fell to -16.0 (-1.1 prior), a 34-month low.

- As with the Texas manufacturing survey counterpart, the main measure of current activity actually ticked higher (revenue index up 3 points to 3.8, "indicating a small increase in revenue"), however employment weakened and, as noted, forward-looking indicators were very weak.

- Per the report, "the future revenue index dropped 14 points to 16.8, the lowest reading since mid-2020. Other future service sector activity indexes such as employment and capital expenditures also fell but remained in positive territory, reflecting expectations for slower growth in the next six months."

- The inflation readings also ticked higher: current prices paid rose to 32.5 (14-month high) from 27.0, with prices received ticking up to a more modest 4-month high 8.4 from 5.2.

- Anecdotes were broadly negative, mainly citing tariffs - and as we reported previously in our overview of the Manufacturing survey, special questions (which covered the manufacturing, services and retail survey respondents) pointed to significant concerns over tariff implications.

- As a side note, the Texas Retail Outlook Survey - a component of the broader Services survey - showed retail sales activity improved in April, corroborating some signs elsewhere that retail activity to start the quarter (ie Johnson Redbook index) was solid despite sharply weaker sentiment.

US STOCKS: First Half Equities Update: Holding Modest Gains, Earnings going

Apr-29 16:19

- Stocks are holding firmer, top end of mostly narrow ranges ahead midday, DJIA outperforming SPX eminis and Nasdaq indexes. Currently, the DJIA trades up 294.25 points (0.73%) at 40522.85, S&P E-Minis up 21.5 points (0.39%) at 5574.25, Nasdaq up 43.1 points (0.2%) at 17409.22.

- Materials and Health Care sectors outperformed in the first half, chemical makers buoyed the former with Sherwin-Williams +5.04%, Ecolab +2.01%, Mosaic +1.83%, Albemarle +1.69% and International Flavors & Fragrances +1.07%.

- Pharmaceutical makers buoyed the Health Care sectors: Pfizer +3.51% after announcing cost cutting measures as quarterly revenues decline, Merck & Co +2.19%, Amgen +1.45%, Danaher +1.30% and Viatris +1.27%.

- Conversely, Energy and Consumer Discretionary sectors underperformed in the first half, oil & gas stocks weaker with crude lower (WTI -1.37 at 60.68): APA -1.87%, Texas Pacific Land -1.14%, Targa Resources -1.07%, ConocoPhillips -0.97% and Devon -0.82%

- Meanwhile, travel & resort related stocks retreated: Caesars Entertainment -3.24%, MGM Resorts Int -2.20% and Carnival -1.94%.

- Latest earnings expected after the close: Booking Holdings, Mondelez International, Caesars Entertainment, Seagate, Starbucks, Frontier Communications, Expand Energy, Fair Isaac, Visa, BXP, PPG, Edison Int, ONEOK, First Solar, CoStar Group and Snap Inc.