US TSYS: Curve Marginally Flatter In Asia

TYU3 deals at 114-01, +0-08, a 0-04 range has been observed on volume of ~56k.

- Cash tsys sit 1bp cheaper to 1bp richer across the major benchmarks, the curve has twist flattened pivoting on 10s.

- Tsys were marginally pressured as spillover from ACGBs, in lieu of RBA Gov Lowe's remarks this morning as he noted further tightening may be needed due to wage gains and persistent service price pressures.

- A bid in JGBs and the Yen, which saw pressure on Japanese equities, facilitated a recovery off session lows. The move didn't follow through and tsys respected narrow ranges for the remainder of the Asian session.

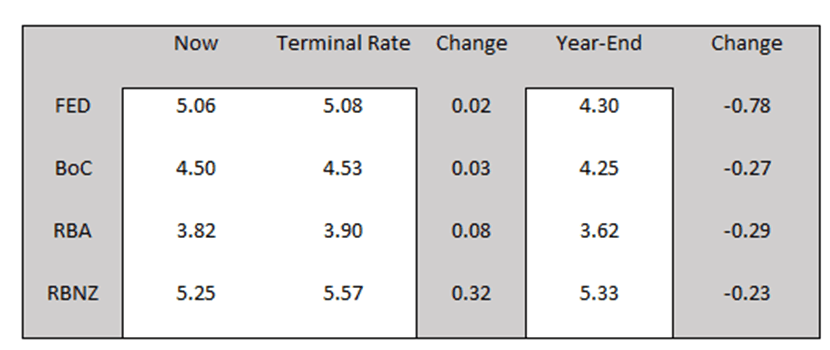

- FOMC dated OIS price ~6bps of hikes into next week's meeting, a terminal rate of ~5.25% is seen in July with ~30bps of cuts priced for 2023.

- German Industrial Production and ECB-speak from de Guindos headlines the European session. Further out we have US Trade Balance and the latest monetary policy decision from the Bank of Canada.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BUND TECHS: (M3) Trend Needle Still Points North

- RES 4: 140.30 High Mar 20 and key resistance

- RES 3: 138.09 High Apr 6

- RES 2: 137.55 61.8% retracement of the Mar 20 - Apr 19 bear leg

- RES 1: 137.22 High May 4

- PRICE: 136.14 @ 05:24 BST May 8

- SUP 1: 135.62 Low Apr 4

- SUP 2: 135.34 20-day EMA

- SUP 3: 134.35 Low May 2

- SUP 4: 133.64/133.10 Low Apr 28 / 19 and the bear trigger

Bund futures trend conditions remain bullish and the recent pullback appears to be a correction. The focus is on 137.55, a Fibonacci retracement. Clearance of this level would open 138.09, the Apr 6 high. On the downside, key short-term support has been defined at the Apr 19 low of 133.10. This is the bear trigger and a break would reinstate the recent bearish theme. Initial firm support is at 135.34, the 20-day EMA.

BONDS: NZGBS: Closed Weaker Near Morning Cheaps

NZGBs closed near session cheaps with benchmark yields 6-9bp higher and the 2/10 cash curve 3bp flatter. With no local data or meaningful local news flow, the NZGB market basically held near opening levels following the weaker lead-in from US tsys after solid non-farm payrolls data on Friday. NZ/US and NZ/AU 10-year yield differential both closed 1bp wider at respectively +72bp and +76bp.

- Swap rates closed 5-6bp higher with implied short-end swap spreads tighter.

- RBNZ dated OIS closed with pricing 1-6bp firmer across meetings with Apr’24 leading. 24bp of tightening is priced for the May 24 meeting.

- The local calendar is scheduled to release Retail Card Spending data for April tomorrow with a continued shift towards services expected.

- In Australia, Treasurer Chalmers is slated to hand down his first Federal Budget tomorrow. If it turns out to be significantly expansionary then RBA rate expectations may be affected.

- Further afield, the calendar is relatively light ahead of Wednesday’s release of US CPI for April.

STIR: Payroll Data Sees US STIR Remove June Easing Expectations

US STIR shifted firmer in NY trade ahead of the weekend following solid payroll growth and an unexpected decline in the unemployment rate. The move was supported by Fed Bullard’s comments that the Federal Reserve needs to raise interest rates further because growth and employment are likely to remain resilient and inflation is set to decline but only slowly.

- The market is now pricing a 6% chance of a 25bp rate hike at the June 14 meeting versus a 16% chance of a 25bp cut in the aftermath of the FOMC’s policy decision late last week.

- Year-end easing expectations were scaled back to 78bp from 87bp at Thursday's close.

- There has been little movement in CA, AU or NZ STIR since late last week.

Figure 1: $-Bloc STIR: Terminal Rate Expectations & Year-End Pricing

Source: MNI – Market News / Bloomberg