OIL: Crude Continues Trending Higher On Geopolitics

Oil prices jumped on Wednesday as risks around Russian supply rise from both Ukrainian strikes and increased sanctions. Russia considered limits on diesel exports after recent damage to ports and refineries. US President Trump’s loss of patience with Russia’s unwillingness to contemplate an end to its war in Ukraine has also added upward pressure to crude.

- Trump stated that he believed Ukraine could win back its territory with European help, omitting the US.

- WTI rose 2.2% to $64.81/bbl to be up almost 4% this week as short positions in the market are reduced on geopolitical tensions. The benchmark fell to $63.25 before reaching $65.05. Breaks above $65 were brief. It is currently around $64.73. Initial support and bear trigger is at $60.85 with key resistance at $68.43.

- Brent was up 2.1% to $69.07/bbl and is 3.6% higher this week. It rose to $69.37 after an intraday low of $67.51. Despite the 2.4% increase in September, a bear cycle remains and gains continue to be considered corrective. Key short-term support is at $64.50 and key resistance at $71.93.

- The EIA reported a 0.61mn barrel US crude drawdown last week after the previous substantial 9.29mn. Product stocks were also lower with gasoline down 1.08mn and distillate 1.7mn. Refining utilisation dropped 0.3pp to 93%, 2.1pp above the same time last year.

- Also on the supply side, a deal is apparently being finalised which will allow exports of 230kbd from Iraqi Kurdistan to resume which have been halted for two years.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: UK AUG BRC SHOP PRICES +0.2% M/M, +0.9% Y/Y

- MNI: UK AUG BRC SHOP PRICES +0.2% M/M, +0.9% Y/Y

AUSSIE BONDS: ACGBS Yields Tick Up, But Slightly Lagging US Tsys, RBA Mins Today

The early bias in Aussie bond futures is modest weakness, in line with US Tsy futures softness from Monday trade. 10yr (XM) futures were last around 1.52bps lower, tracking at 95.675, while 3 yr futures (YM) were also down 1.5bps to 96.595. These shifts keep us within recent ranges.

- In the cash government bond yield space, we are +1-1.5bps firmer in the first part of dealings, so slightly lagging the moves seen in US Tsy yields from Monday's session. US yields were 2-3bps firmer, led marginally by the front end. Treasuries opened weaker - scaling back a fair portion of Friday's post-Chair Powell speech in Jackson Hole that left the door open to a possible rate cut at the next FOMC. Liquidity was likely impacted with UK markets out. Treasury futures also maintained losses after higher than expected new home sales data.

- The 10yr Aussie bond yield sits just under 4.30%, while the 3yr is close to 3.40%.

- On the data front today, the focus is on the RBA Minutes from the August policy meeting. They will likely be monitored for further details on its concerns regarding lacklustre productivity growth, its view on the labour market and any discussion of the risks around its inflation outlook. The vote to ease was unanimous.

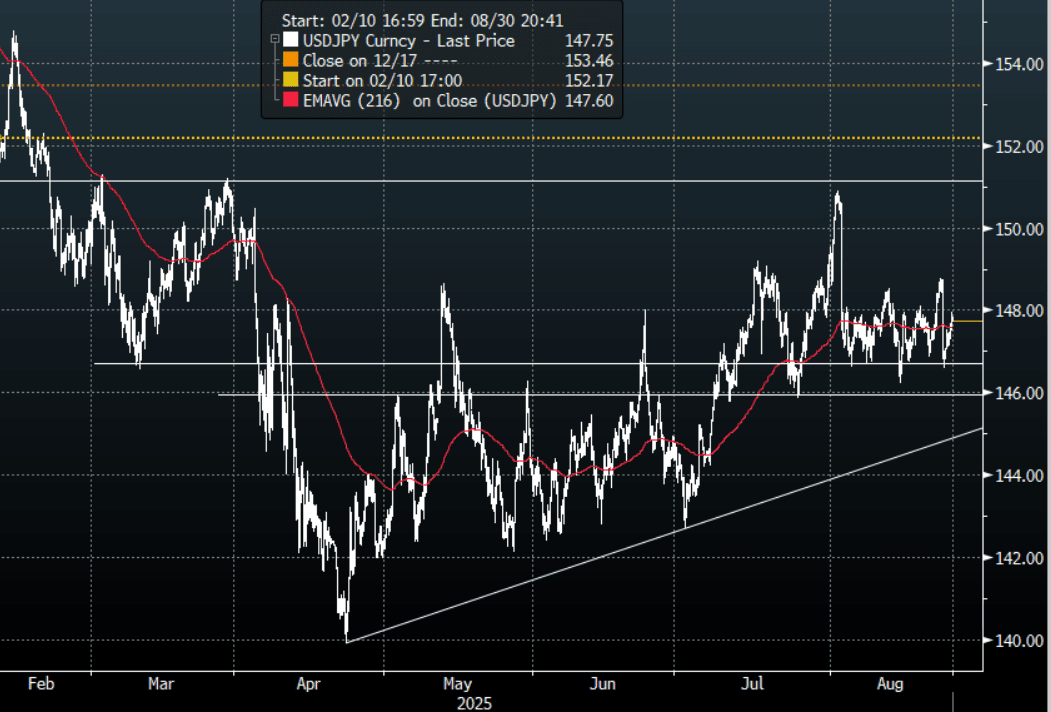

JPY: USD/JPY - Support Holds And Pares Back Some Of Fridays Drop

The overnight night range was 147.10-147.94, Asia is currently trading around 147.75. USD/JPY grinded higher all day yesterday paring back just over 50% of the knee-jerk lower. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. CFTC data for last week shows leveraged accounts again added to JPY shorts so the initial reaction to Powell would have been unwelcome and they would be breathing a little easier today as the support continues to look solid.

- Joseph Wang on X: “Good speech by Ueda on how Japan's aging demographics are driving up wages. Increasing participation rates and retiring at a later age have reached their limits. It looks like the theory that aging demographics is inflationary will be validated. https://t.co/YyW7JcMySw”

- "Japan’s trade negotiator may visit the US this week, FNN reported. The country is also preparing a joint communique for its US investments." - BBG

- "JAPAN MULLS 5-YEAR TAX BREAK ON CAPITAL INVESTMENTS: YOMIURI" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 148.00($992m), 146.35($716m).Upcoming Close Strikes : 148.00($893m Aug 27), 146.50($1.14b Aug 29), 145.00($1.7b Aug 29) - BBG.

- CFTC data shows last week asset managers have begun to add to their JPY longs after a consistent period of reduction +71379( Last +60866), leveraged funds though again used the dip to add to their newly built short JPY position -50848(Last -41257).

- Data/Event : PPI

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P