EU CREDIT UPDATE: CREDIT UPDATE: EUR Market Wrap

Nov-18 07:00

- Bunds closed 1-4bp wider with 2y/10y yields at 2.11%/2.35% - after the afternoon’s ECO data tilted slightly hawkish while German budget headlines provided some support in the morning. WoW move of -6.6bp/-1.1bp.

- Main/XO ended +1.6bp/+8bp at 56.4bp/304bp while €IG was +0.6bp at 0.99% (Corps +0.5bp at 0.94%, Fins +0.6bp at 1.06%, €HY flat at 3.23%) for a WoW move of -0.6bp (Corps +0.1bp, Fins -1.5bp, €HY -1bp). 3-10yr spreads outperformed WoW at ~-1bp while Cycs lagged at +1.4bp with Autos +1.5bp and Retailers +3bp. $IG was +0.8bp at 0.77% (Corps +0.7bp at 0.77%, Fins +1bp at 0.78%, $HY +11bp at 2.65%).

- SXXP/SPX ended -0.8%/-1.3% at 503pts/5871pts. €IG's biggest risers/fallers included Norsk Hydro ASA (+7%), Mizuho Financial Group Inc (+7%), Generali (+5%), Lonza Group AG (-8%), Omnicom Group Inc (-8%), Warner Bros Discovery Inc (-6%).

- SX5E/SPX futures are +0.1%/+0.3%. Overnight team flagged that It has been an uneventful day in USTs so far, ranges have been narrow, with little in the way of headlines. BoJ Governor Ueda maintained his stance that the bank will continue to raise the policy rate though he slightly downplayed an imminent hike.

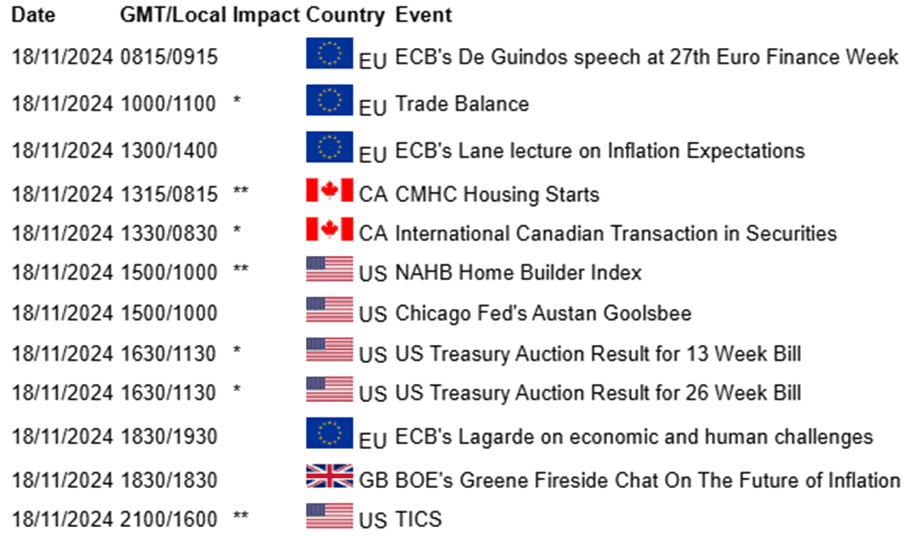

- Later the Fed’s Goolsbee speaks, and November NY Fed services and NAHB housing indices print. We also hear from the RBA's Kent. The ECB’s Lagarde, de Guindos, Lane and Buch also appear, and euro area September trade data are out. BoE’s Greene speaks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RATINGS: UK, Italy Affirmed by S&P; Scope Downgrades France

Oct-18 21:02

Recapping sovereign ratings actions today:

- S&P affirms Italy's Long-Term Local Currency Debt Rating at BBB, outlook remains stable

- S&P affirms the UK's Long-Term Local Currency Debt Rating at AA, outlook remains stable

- Scope downgraded France to AA- (from AA) with a stable outlook

- S&P did not affirm/update the ratings of Greece or the Netherlands as part of their semi-annual review of the sovereigns.

US FISCAL: Budget Deficit Rises As Interest Payments Soar

Oct-18 20:27

The US's September budget balance came in very close to expectations with a $64B surplus, just the 2nd monthly surplus posted in the 2024 fiscal year just ended (Monthly Treasury Statement here - PDF).

- For the fiscal year as a whole (Oct-Sep), the nominal deficit came in at $1.83T, equating to 6.4% of GDP - that's up from $1.70T in FY 2023 (6.2% of GDP).

- For the year, revenues rose by a little under $500B but outlays grew by over $600B. Notably, interest rose 29% to $1.13T (net $882B), with the net figure 3.06% of GDP: the highest since 1996. That came as the weighted average interest rate of debt outstanding rose 35bp on the year to 3.32%, while social security payments rose by $103B on higher cost of living increases and more retirees.

- The 2025 fiscal year deficit is not expected to be much changed as a percentage of GDP, though that could depend on the November election results.

- CBO director Phillip Swagel told MNI recently America has fiscal headroom in the near-term but spending is on an unsustainable track over the long-term (link).

MNI: US SEP TREASURY BUDGET $64.3B

Oct-18 20:00

- MNI: US SEP TREASURY BUDGET $64.3B