CANADA: Credit Loss Provisions Generally Level Out With BMO An Exception

Dec-05 13:20

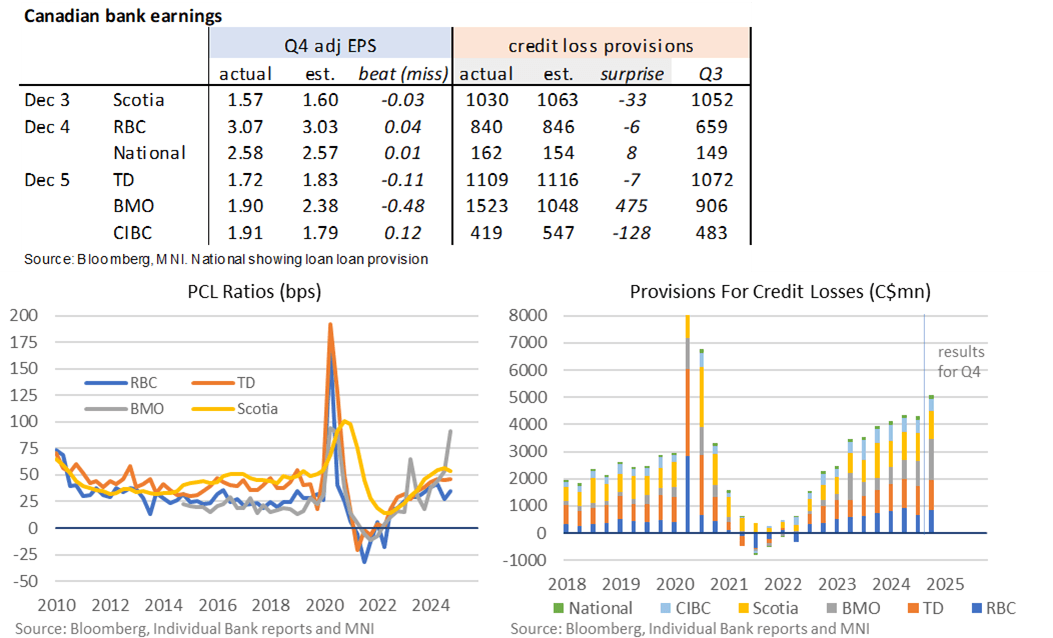

- Today’s bank earnings complete out a narrow window for the “big six” banks this quarter.

- Adjusted EPS estimates were lower than expected for BMO (notably so with C$1.90 vs est C$2.38) and TD (C$1.72 vs est C$1.83) but higher for CIBC (C$1.91 vs est C$1.79).

- From a macro angle, credit loss provisions have on the most part been close to expectations or lower, but BMO again stands out with a much larger than expected C$1.5bn (est C$1.0bn) for a jump from C$0.9bn in in Q3.

- BMO details: “Higher provisions primarily from BMO Capital Markets and Commercial businesses, reflecting impact of elevated interest rates on certain customer segments.”

- In terms of a read specifically for Canadian lending health, “personal & business banking” provisions were steady at C$275m after C$274m with latest increases in commercial banking from C$79m to C$165m (total from C$353m to C$440m). US personal & commercial provisions increased from C$368m to C$435m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILT PAOF RESULTS: The PAOF for the 4.25% Jul-34 Gilt was not taken up.

Nov-05 13:03

- GBP937.5mln had been available.

- This leaves GBP26.637bln in issue.

FOREX: USDJPY Prints 152.09, Short-Term Attention on Gap to Friday’s Close

Nov-05 12:48

- While US yields have ticked higher on Tuesday, USDJPY has operated in a relatively contained 45 pip range, recently edging back towards session lows of 152.09. Betting odds for a Trump victory are now more reflective of Friday’s levels, which might suggest the short-term risks could be tilted towards the greenback filling the gap to last week’s closing prints.

- For USDJPY, closing this gap would require a move to 153.01, and technical conditions suggest an overall bullish trend structure remains intact for the pair. On the topside, a clear breach of 153.40 (retracement level) would set the scene for an extension towards 155.27, a Fibonacci projection.

- It is also worth highlighting that overnight Reuters cited former BOJ board member Makoto Sakurai as saying the BOJ are likely to wait until January to raise interest rates when there will be more clarity on political and market developments. Given some analysts have touted December for the next move, this could be deemed as a dovish view at the margin.

- On the other hand, with the election remaining a close call and a potentially subdued session ahead, any early leanings towards a Harris victory could further weigh on USDJPY and there remains plenty of downside before initial firm support at 149.11, the 50-day EMA. The 20-day EMA is at 150.86.

ITALY DATA: Familiar Industry-Level Divergence Signalled In Bank of Italy Survey

Nov-05 12:30

The Bank of Italy’s latest Business Outlook Survey of Industrial and Services Firms points to further growth in the services industry but continued weakness in manufacturing. These signals are consistent with recent PMI and flash GDP data. A few excerpts of note from the release:

- “Manufacturing was mainly affected by the performance of exports, which reflected a weak manufacturing cycle in the euro area, particularly in Germany”.

- “Firms expect both domestic and foreign sales to grow over the next six months”.

- “The number of hours worked continued to rise in services and slowed down in manufacturing; in both sectors, firms expect it to climb higher over the next six months”.

- “Borrowing conditions, which had worsened significantly over the last two years, are seen as improving, but assessments of stability still prevail”.

- “For 2025, firms anticipate a further expansion across all sectors except for textiles, clothing and footwear. The adoption of generative artificial intelligence in business processes is expected to rise over the next 12 months”.