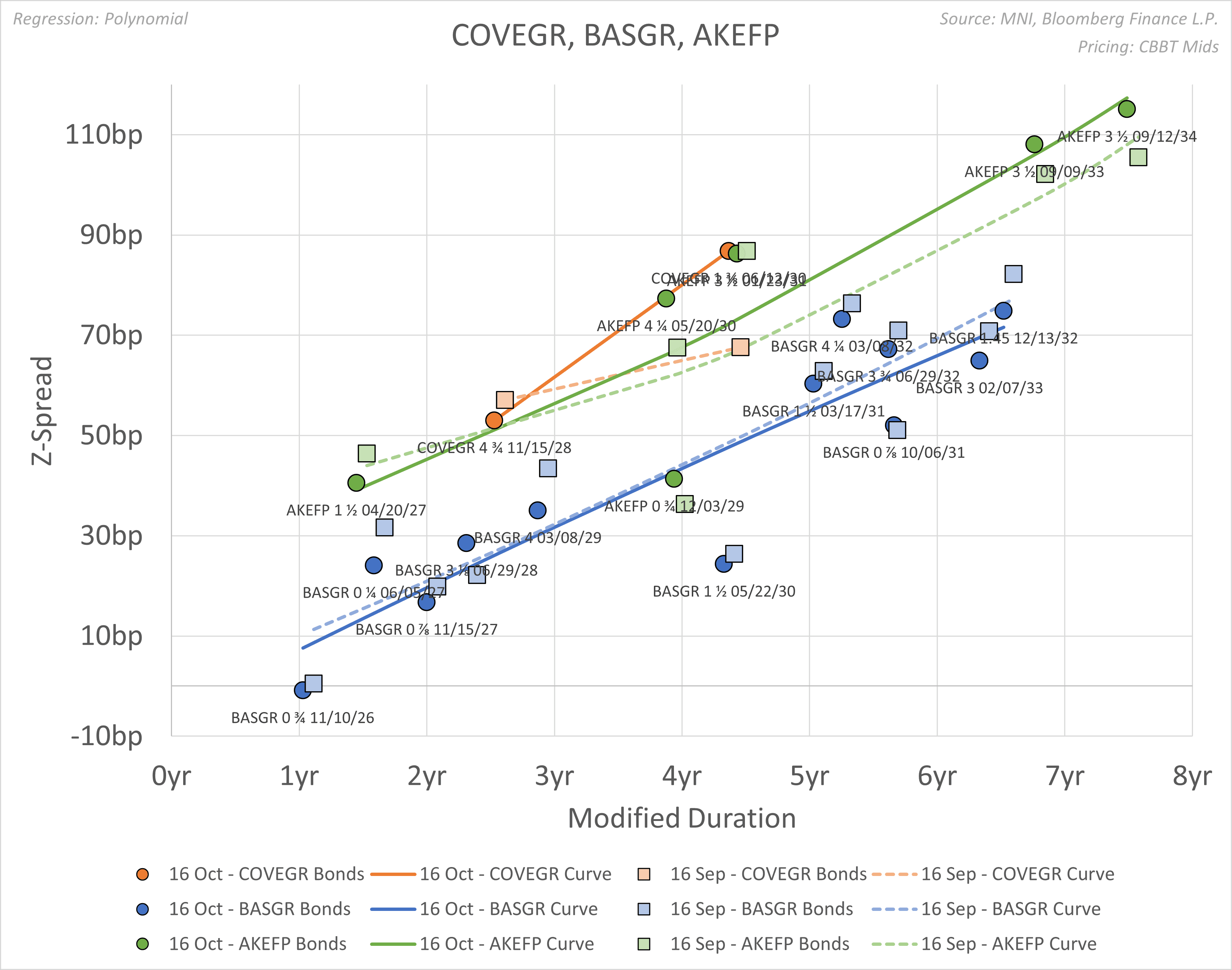

EU BASIC INDUSTRIES: Covestro: Covestro 30s (COVEGR; Baa2/NR/NR)

• COVEGR 1.375 30s have widened +22bps MoM.

• Bonds now sit outside the Arkema curve.

• Reuters reported on Tuesday that "ADNOC set to win EU nod for $17 billion Covestro deal with remedy tweaks, sources say"

Reuters Link

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US: Speaker Johnson Canvasses GOP Support For Govt Funding Measure

After the release slipped yesterday, House Speaker Mike Johnson (R-LA) is expected the final text of a short-term funding measure (CR) to keep the government open through mid-November at around midday today. Johnson met his conference this morning to build support ahead of a final House vote, likely on Friday.

- Johnson can only drop one vote on the floor as Rep Thomas Massie (R-KY) always votes against CRs. Senate Republicans need at least 7 Democratic votes to clear the filibuster, effectively giving Senate Majority Leader Chuck Schumer (D-NY) the power to force a shutdown.

- Punchbowl News notes, “If you listen to [Democrat leader Chuck] Schumer, you come away believing he’s prepared to dive into a government shutdown. Schumer said Monday that Republicans refuse to negotiate and are “causing [a] shutdown.””

- To endorse a funding patch, Democrats are seeking, at a minimum, an extension of 'Obamacare' tax credits. Senate Majority Leader John Thune (R-SD) has ruled out health care provisions in the CR, appearing to set the stage for ‘jamming’ Democrats with a clean bill that forces Schumer into a decision on shutting down the government.

- There will be a high volume of newsflow aimed at controlling shutdown messaging today. House Republicans will hold a presser at 10:00 ET 15:00 BST, House Democrats at 10:45 ET 15:45 BST, and Senate Democrats at 11:30 ET 16:30 BST.

- The implied probability of a shutdown is currently 37%, per Polymarket, which appears low considering the absence of any agreement, but traders likely believe that Schumer will ultimately fold.

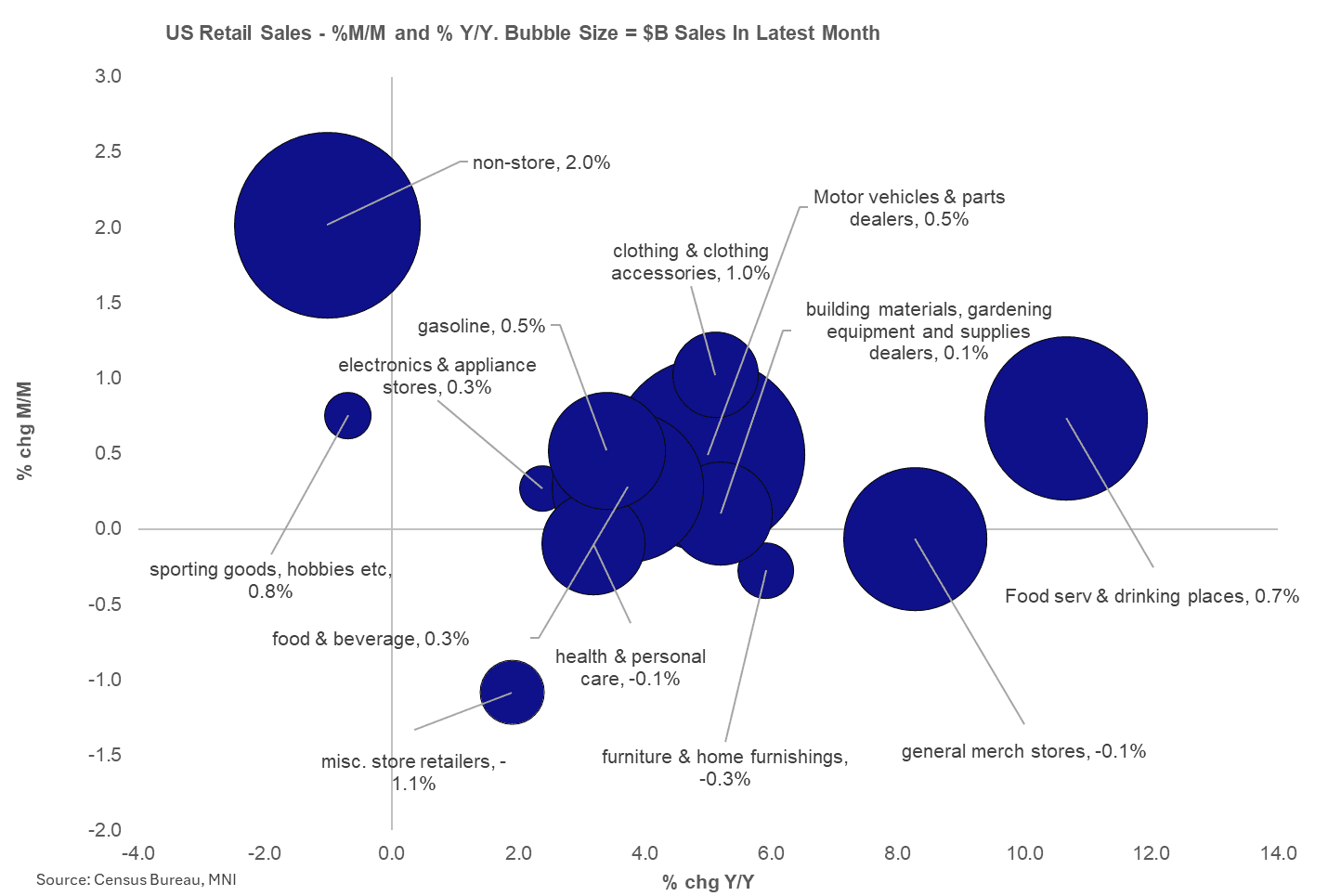

US DATA: Non-Store Retail, Autos Resilience Drives Strong Overall Sales Beat

August retail sales beat expectations in all departments, with higher revisions adding to the positive takeaways suggesting potential upgrades to Q3 personal consumption expenditures estimates.

- Headline retail sales ticked up to 0.63% M/M from an upwardly-revised 0.61% prior (rev from 0.51%), a significant upside beat vs the 0.2% consensus (all figures nominal, seasonally-adjusted). Ex-auto/gas sales rose to 0.68% M/M from 0.30% prior (rev from 0.23%, vs 0.4% consensus) while the GDP-input Control Group rose to 0.74% from 0.50% (unrevised; and vs 0.4% consensus).

- Momentum is picking up in retail sales: 3M/3M annualized control group sales are now at the highest in a year at 6.7%, having bottomed out below 4% over March-May, while overall retail sales are above 4.0% on that basis (4.1%) for the first time January.

- They key surprise as indicated from the above headline breakdowns is that motor vehicle sales growth remained positive (+0.4% after +1.9%) amid widespread expectations of contraction in August in this 2nd largest category of retail sales. The major upside driver though was the single largest retail sales category: non-store (ie online) retail, which saw 2.0% sales growth in August, best in 11 months and a significant acceleration from 0.6% prior (which in itself had been seen as a strong month helped by Amazon Prime Day sales). We should point out here that non-store sales exceeded vehicle sales by the most ever, at $1.6B.

- Elsewhere, categories grew more slowly than in July, including electronics/appliances; food and beverage; gasoline; clothing; and sporting goods/hobbies; in contracting on the month were furniture; health/personal care/and general merchandise stores.

- One exception was building materials stores which pared a 0.9% contraction in July with 0.1% growth, and even more notably, food services / drinking places which jumped to 0.7% growth after -0.1%. Both of those categories are ex-control but we would argue are important categories to gauge the health of the consumer. Indeed, restaurants/bars are the 3rd largest retail category and the robustness in August is suggestive of resilience in discretionary demand.

- All that said, the strong CPI prints in some categories in the month are suggestive of a nominal vs a real effect here, particularly with the pickup in food and vehicle prices of late.

SOFR OPTIONS: SFRZ5 96.00 Puts Sold

SFRZ5 96.00 puts 23K given at 1.0 over several clips.