MALAYSIA: Country Wrap: Fiscal Deficit Down on Higher Revenue

- Federal government’s fiscal deficit fell to 21.9 billion ringgit ($5.1 billion) as of end-March, from 26.4b ringgit the same period a year ago, due to higher revenue collection and lower spending of subsidies, according to Malaysia’s Ministry of Finance. Revenue in 1Q climbed 3% y/y to 72.1b ringgit, driven by higher tax collection, particularly from a surge in the sales tax and service tax receipts and stronger individual income tax (source BBG)

- Foreign reserves amounted to 528.1b ringgit ($119.1b) as of May 15 (source BNM)

- The FTSE Malay KLCI bounced higher today by +0.48% yet is down by -2.38% for the week.

- The ringgit has had posted strong gains today of +0.55% and has gained more than 1% for the week.

- Bonds have finished the week with a strong rally with the 10YR lower by-4.5bp at 3.56%hh

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP TECHS: MA Studies Continue To Highlight An Uptrend

- RES 4: 0.8800 Round number resistance

- RES 3: 0.8781 2.236 proj of the Mar 3 - 11 - 28 price swing

- RES 2: 0.8768 High Nov 20 ‘23

- RES 1: 0.8624/0.8738 High Apr 21/ High Apr 11 and the bull trigger

- PRICE: 0.8580 @ 16:17 BST Apr 22

- SUP 1: 0.8524 20-day EMA

- SUP 2: 0.8477 61.8% retracement of the Mar 28 - Apr 11 rally

- SUP 3: 0.8442 50-day EMA

- SUP 4: 0.8415 76.4% retracement of the Mar 28 - Apr 11 rally

Recent weakness in EURGBP appears corrective and the retracement has allowed an overbought trend condition to unwind. Support to watch lies at 0.8524, the 20-day EMA. Below this level, support at the 50-day EMA is at 0.8447. The area between these two averages represents a key support zone. For bulls, a resumption of gains would refocus attention on 0.8738, the Apr 11 high and bull trigger. First resistance is 0.8624, the Apr 21 high.

SCHATZ TECHS: (M5) Approaching The Bull Trigger

- RES 4: 107.812 0.618 proj of the Mar 6 - Apr 7 - 9 price swing

- RES 3: 107.800 Round number resistance

- RES 2: 107.775 High Apr 7 and the bull trigger

- RES 1: 107.735 High Apr 22

- PRICE: 107.595 @ 06:06 BST Apr 23

- SUP 1: 107.370 Low Apr 17

- SUP 2: 107.298 20-day EMA

- SUP 3: 107.125 Low Apr 10

- SUP 4: 106.965 Low Apr 9 and a key support

Schatz futures maintain a firmer tone and sights are on 107.775, the Apr 7 high and bull trigger. The recent pullback between Apr 7 - 9, appears corrective. Clearance of 107.775 would confirm a resumption of the uptrend and open 107.812, a Fibonacci projection. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. Firm support to watch lies at 107.298, the 20-day EMA.

AUSTRALIA: Q1 NZ CPI Data Suggest Australian Services Inflation Moderated

Q1 Australian CPI data is released on Wednesday April 30 and will be an important input into the May 20 RBA decision, where a rate cut is largely expected. There are high correlations between NZ and Australian CPI data and given NZ’s Q1 has already been released, there are possibly trends that we can ascertain. Australia may see a pickup in goods inflation, while sticky services may moderate.

- NZ headline, non-tradeables & tradeables printed higher than expected but both headline and core were in the RBNZ’s 1-3% target band at 2.5% y/y and 2.9% y/y respectively.

- With government electricity rebates continuing to reduce Australia’s headline inflation, there is little to be gained by looking at NZ’s trends here.

- There is a 3-year rolling correlation of around 90% between Australia/NZ underlying inflation measures. The RBNZ’s sector factor model estimate of core moderated 0.1pp to 2.9% in Q1. In addition, Australia’s monthly data are pointing to a moderation in quarterly trimmed mean inflation in Q1.

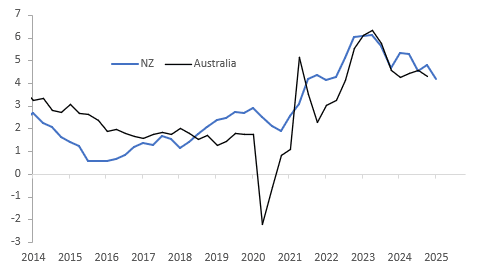

Australia vs NZ core CPI y/y%

- Domestically-driven services inflation has been monitored closely for some time and the Australia/NZ correlation is also close to 90%. NZ services inflation moderated 0.6pp to 4.2% y/y and non-tradeables 0.5pp to 4.0% y/y, which is good news for Australia.

- Australia is likely to see a pickup in goods inflation, which is significantly determined by global factors. It rose to 1.4% y/y in NZ from 0.6% signalling that its disinflationary pressure is likely over, consistent with Australia’s monthly goods inflation data.

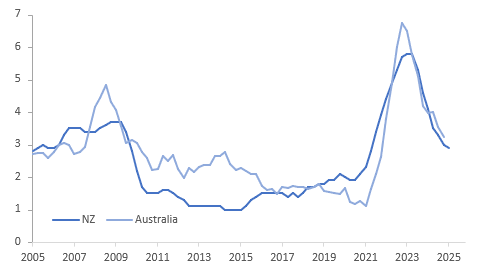

Australia vs NZ services y/y%