EU CREDIT MACRO: Consumer & Transport: Week in Review

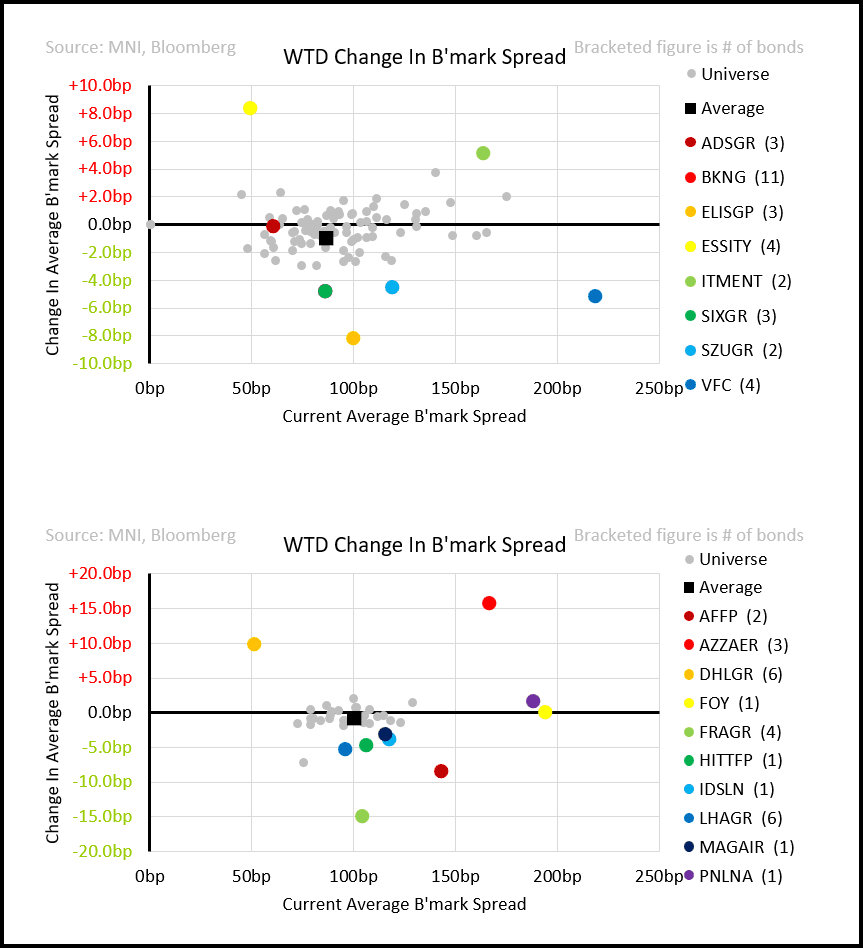

Secondary took a break from last week’s vol but equities did not – earnings which saw cuts to guidance citing US weakness drove their moves. Adding to that there was little good news for apparel retailers on the Feb US retail sales print. On the other side the best performing curve in consumer this week is Elis – our only value view in services. A nice to see, but as we said this week caution on running too fast away from the US consumer. Particularly for longer term investors (selective) Yankee names may show relative value here and we saw an accelerated version of that play out in Carnival this week. Finally, and as always caution on conflating macro and issuer specific weakness – General Mills blaming US macro this week was quiet amusing. If investors have to sit through MSD sales fall and double-digit EBIT falls at the start of cycle, they should question if it is a staple and if it can demand +70 over swaps on the 5y - tight vs. other subsectors. GIS admits it is underperforming broader market which is still growing (slowly) and seems to be driven by a lack of investment to keep up with the accelerated trend towards healthier snacking. It says it is working on it.

Event driven news

- Barry Callebaut continues rallying on Cocoa price falls. On the lower WC swing we hold a marginal value view unch from primary on the step-up protected 28s. Caution - Cocoa is volatile and rough-on-BS earnings ahead.

- Air-France is not trending at a run-rate in-line with its Dec-2025 emissions reduction target – partly on new fleet delivery delays. We see some value on the May-26 SLBs that could receive +75bp on maturity. Sellers still emerged on Thursday.#

- Sudzucker gives a surprising upgrade to its FY25 (to Feb) EBITDA numbers only a month after issuing pre-lim numbers. FY26 guidance is left lacklustre and was enough to disappoint equities. We expect downgrades but would caution challenging the retail curve till we see evidence of further deterioration.

- Walgreen Boots chair Pessina may reinvest more than his current 17% stake according to the FT. We still see enough for downgrade but paired with the speculation it may secure the debt it may weaken the case for CoC at 101.

- Sodexo 1H results flag US slow-down. We are not concerned for ratings but equally do not see catalyst to stop widening from current levels.

- Fraport indicates there is a 50% chance of German government implementing changes to alleviate cost pressures on the aviation industry. With capex coming down it may be rolling through peak bad news here – one which credit has been immune to on retail denominations.

- Heathrow closing for 1-day on a power outage surprisingly causes euro lines to move wider. We briefly revisit near-term fundamentals and technicals for the UK airport issuers.

- Compass faces some pressure in equities on a broker flagging US exposure. We see credit as low beta still.

- Travel weakened on a lack of air-space ceasefire with Russia. We revisit exposure to Asia and Ukraine here.

Primary (NIC in brackets)

- Deutsche Post: 5y/9y/15y (+6/+10/+10)

- Aeroports de Paris: max €250m tender of €1b 26s at MS+10 was pro-rota’d at 67.6%.

Rating Action

- B&M: S&P moves to negative outlook not on leverage but lacklustre sales. Future for credit will depend on if the new CEO can turn around the performance while maintaining the current credit-positive BS leverage.

- Gatwick: S&P clears its dividend distributions from last year. Hard to see it as low levered after the shift in capital allocation that S&P expects will continue in the face of rising capex.

- Avolta is affirmed by Moody’s after earnings with limited rating headroom. Co is not a rising star with no interest in pursuing further deleveraging.

- Reckitt: Moody’s moves off positive outlook in an overdue reaction to NEC litigation and lacklustre earnings growth.

- Lottomatica upgraded by S&P to BB Stable. Curve has and continues to trade tight

- Asmodee receives a double notch upgrade from S&P post its debt redemption

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: GDPNow Steady After Construction Data

The Atlanta Fed's GDPNow estimate of Q1 2025 real GDP growth was remarkably unchanged after the mixed January New Residential Construction report: 2.3% Q/Q annualized, same as the last update on Feb 14 (both 2.34% unrounded).

- Indeed the estimate of residential investment growth in the quarter was unchanged at 1.8% (up 3bp on an unrounded basis but basically no change).

- The only category to shift was imports, which are seen growing a little more slowly (5.4% vs 5.5% prior) but with no discernable impact on the contribution of net exports to overall GDP.

- Again, a 2.3% outturn would represent no change from Q4 2024's GDP reading, albeit with notably softer consumption, stronger business investment, and renewed drag from net exports offset by inventory buildup.

STIR: Market Tilts Back To Pricing More Than 50bp Of BoE Cuts Through Year-End

Recovery from lows in the long end comes alongside a move off hawkish session extremes in GBP STIRs.

- This morning’s CPI data, in isolation, shouldn’t be enough to shift any single vote at the March MPC.

- Markets continue to price minimal odds of a move at next month’s MPC decision, with ~80% odds of a cut showing through March and ~27bp priced through May.

- 51bp of cuts priced through December vs. ~48.5bp at one stage today and ~53.5bp at yesterday’s close.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Mar-25 | 4.449 | -0.5 |

May-25 | 4.251 | -20.3 |

Jun-25 | 4.186 | -26.8 |

Aug-25 | 4.050 | -40.4 |

Sep-25 | 4.020 | -43.5 |

Nov-25 | 3.957 | -49.8 |

Dec-25 | 3.944 | -51.0 |

MNI EXCLUSIVE: Industry officials anticipate Canada's response to U.S. tariffs

Industry officials anticipate Canada's likely response to U.S. tariffs.-On MNI Policy MainWire now, for more details please contact sales@marketnews.com