AUDUSD TECHS: Consolidation Mode

- RES 4: 0.6700 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6688 High Nov 7 ‘24

- RES 2: 0.6677 0.764 proj of the Jun 23 - Jul 11 - 17 price swing

- RES 1: 0.6530/6625 High Jul 29 / 24 and the bull trigger

- PRICE: 0.6499 @ 16:13 BST Aug 6

- SUP 1: 0.6419 Low Aug 1

- SUP 2: 0.6373 Low Jun 23 and a bear trigger

- SUP 3: 0.6354 38.2% retracement of the Apr 9 - Jul 24 upleg

- SUP 4: 0.6323 Low Apr 16

AUDUSD rallied well off the week’s lowest levels last week on broad USD weakness. Last week, the pair traded through both the 20- and 50-day EMAs. This undermined the recent bullish theme and signals the likely start of a corrective cycle. Note that support 0.6455 the Jul 17 low, has also been cleared. The breach strengthens a bearish threat and signals scope for an extension towards 0.6373, the Jun 23 low. Key resistance has been defined at 0.6625 the Jul 24 high. It also represents the bull trigger.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Pullback Appears Corrective

- RES 4: 0.6700 76.4% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6688 High Nov 7 ‘24

- RES 2: 0.6603 High Nov 11 ‘24

- RES 1: 0.6590 High Jul 01

- PRICE: 0.6514 @ 16:03 BST Jul 07

- SUP 1: 0.6486 Low Jul 07

- SUP 2: 0.6471/6373 50-day EMA / Low Jun 23 and a reversal trigger

- SUP 3: 0.6357 Low May 12

- SUP 4: 0.6275 Low Apr 14

The trend set-up in AUDUSD remains bullish and the latest pullback appears corrective - for now. Recent gains maintain the bullish price sequence of higher highs and higher lows, the definition of an uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 0.6603 next, the Nov 11 2024 high. Initial firm support to watch is 0.6471, the 50-day EMA.

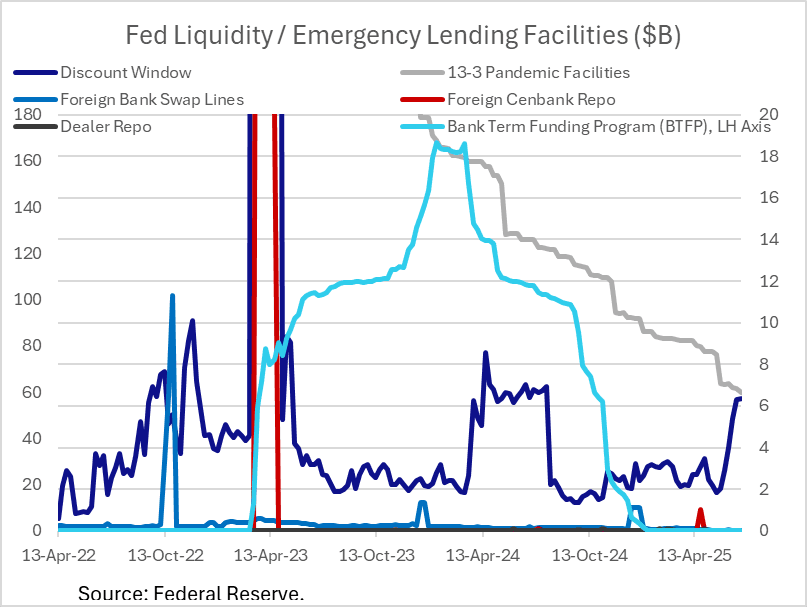

FED: Discount Window Takeup Steadies In Latest Week (1/2)

The latest Federal Reserve H.4.1 release showed limited changes in the size of the Fed's assets and liabilities in the week to Wednesday July 2, with a small drop led by Treasury runoff.

- The latest week saw nominal Treasury holdings fall by around $7B, though the value of TIPS holdings rose $2.3B (presumably due to reflect revaluation on inflation compensation). SOMA runoff over the most recent 4-week period was just under $25B, above the longer-run expected average of $20B ($15B MBS, $5B Tsy).

- Discount window borrowing rose just under $0.5B to $6.4B for a fresh post-July 2024 high, though we don't see the rise as consistent with any sort of meaningful banking sector stress. Pandemic 13-3 program takeup fell $0.2B.

US TSYS: Late SOFR/Treasury Option Roundup: Leaning Bullish

SOFR & Treasury option flow remained mixed Monday, mostly bullish (call buying, put unwinds) with a couple exceptions like the large Sep'25 10Y put skew buyer. Underlying futures broadly weaker but off midday lows, curves steeper with the short end outperforming. Projected rate cut pricing has consolidated vs morning (*) levels: Jul'25 at -1.2bp, Sep'25 at -17bp (-18.9bp), Oct'25 at -32.2bp (-34.7bp), Dec'25 at -49.8bp (-53.0bp).

- SOFR Options:

- -4,000 SFRU5 95.75/96.12 put over risk reversals, 0.5

- 6,500 SFRZ5 96.31/96.37 call spds

- +10,000 SFRZ5 97.18 calls, 3.25 ref 96.17

- -4,000 3QZ5 95.75 puts, 5.5 vs. 96.465/0.16%

- -1,000 SFRN5 95.87 straddles, 3.75

- +8,000 SFRV5 96.25/96.50/96.75 call flys, 3.0

- -1,000 SFRV5 96.18/96.43 strangles, 23.75

- +2,500 SFRM5 96.75/97.25 call spds vs. 0QM 97.25 calls, 1.0 net

- Block/screen 8,000 SFRV5 96.06/96.18/96.31/96.43 call condors, 3.25

- 1,850 SFRU5 95.87 put vs. 95.93/96.12 call spd ref 95.88

- Block, 5,000 SFRV5 96.12/96.18/96.31/96.43 broken call condors, 0.0

- +2,000 SFRH6 96.50/97.00 call spds, 13.5 ref 96.43

- 2,100 SFRN5 95.75/95.81/95.87 put trees, 1.5

- 3,336 SFRZ5 95.75/95.87/96.25/96.37 put condors, 6.5 ref 96.21/0.05%

- Treasury Options:

- -20,000 TYU5 113 calls vs. 109/110 put spds 1 net ref 111-00.5

- Block, 10,000 TYU5 113.5 calls, 13 vs. 111-02/0.05%

- 5,000 TYU5 109.5 puts, 21 ref 110-31.5 to -30.5

- 1,000 FVQ5/FVU5 108.25 straddle spd

- 2,500 TYU5 113/113.5 call spds, 1 ref 111-01

- 6,500 TYQ5/wk2 TY 110.25 put spd, 11 net

- 2,000 TYV5 122.5 calls, ref 111-04.5

- 2,400 TUQ5 104.5 calls, 0.5 (exp 7/25)

- 2,000 TYU5 111.5 puts

- -20,000 TYQ5 109.5 puts, 4 ref 111-07

- +1,000 TYQ5 111.5/112/112.5 call flys, 4

- +1,000 FVQ5 108/108.5 2x1 put spds, 3