ASIA: Coming up in the Asian session on Friday

Jun-13 21:00

| 2100GMT | 0500HKT | 0700AEST | South Korea May Import/Export Price Index |

| 0300GMT | 1100HKT | 1300AEST | South Korea Apr Money Supply |

| 0630GMT | 1430HKT | 1630AEST | India May Wholesale Prices |

| 0730GMT | 1530HKT | 1730AEST | Thailand June Gross International Reserves |

| 0830GMT | 1630HKT | 1830AEST | Hong Kong 1Q PPI |

| 0830GMT | 1630HKT | 1830AEST | Hong Kong 1Q Industrial Production |

| India May Trade Balance | |||

| India June Foreign Exchange Reserves |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US OUTLOOK/OPINION: Potential Reactions To CPI Report

May-14 20:33

[The below taken from the MNI CPI Preview. Full note found here]

- An upside surprise, with even another ‘low’ 0.4% if driven by areas away from PPI-relevant categories (which could limit the impact from any supercore surprises this month), could bring 5% 2Y Treasury yields back into play again.

- Expect sizeable resistance at this level though, having struggled to hold a sustained break on multiple occasions over the past month.

- The longest foray into a 5 handle was after the surprisingly strong ECI data for Q1 on Apr 30, reaching a high of 5.043%, before it slipped below with the FOMC on May 1 and it hasn’t tested it since.

- Instead, it reached a snap low of 4.708% after payrolls on May 3 – demonstrating the heightened sensitivity to softer labor data – but is currently back at 4.85% after some upside inflationary surprises.

- This 5% level could still see a firm test though as it would be seen as further evidence that the start-of-year acceleration is more than just a bump in the disinflationary path back towards 2% PCE inflation.

- We imagine this would come from a further delay in the start point of rate cuts rather than outright expectations of a near-term hike.

- An inline reading of around 0.30% M/M would further dial up attention on labor data.

- Markets will still clearly be sensitive to a downside surprise of 0.2% M/M but after three months averaging 0.37% M/M for core CPI, the onus is clearly on seeing multiple softer inflation readings as various FOMC members have said.

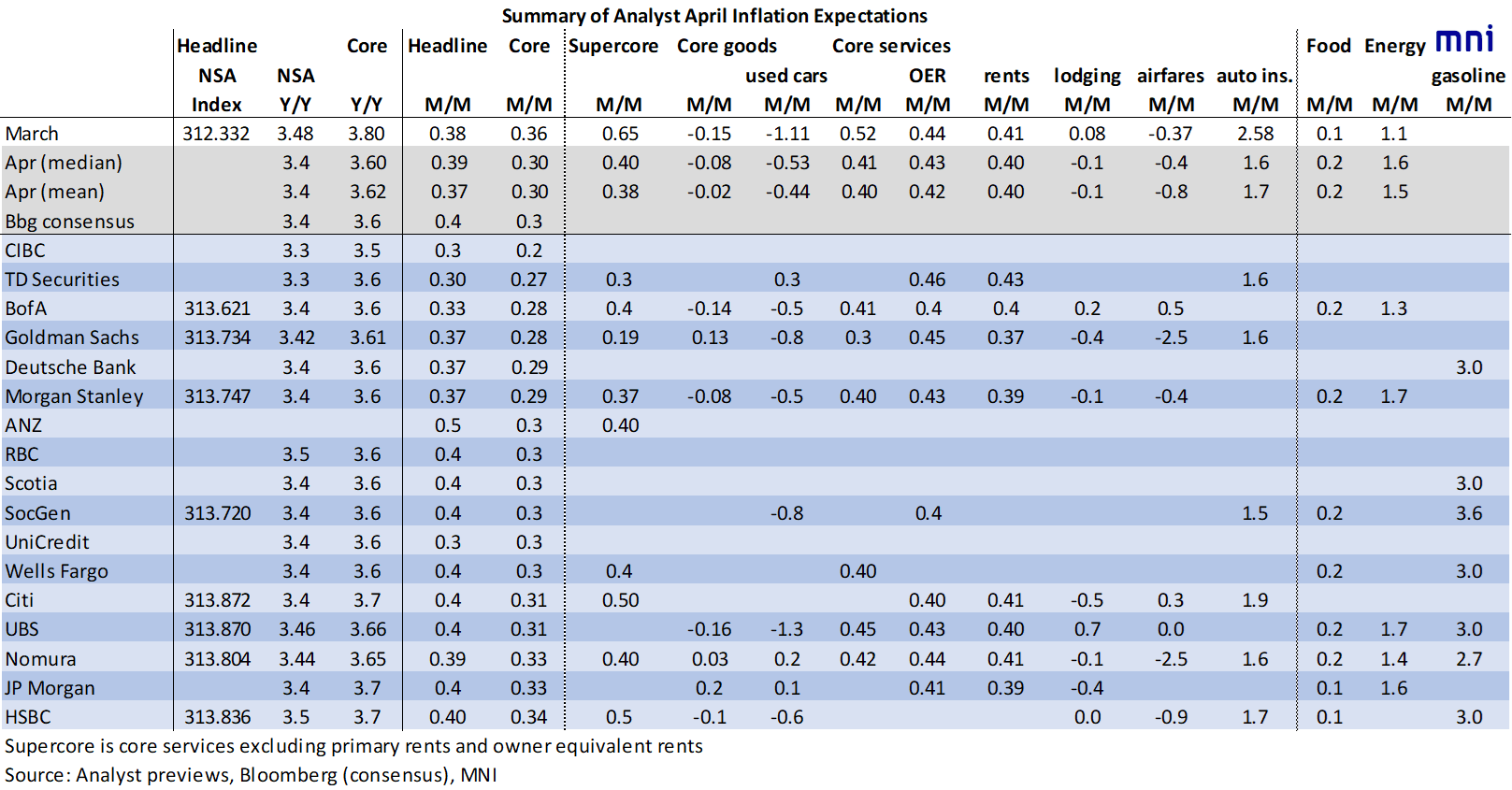

US OUTLOOK/OPINION: Summary Of Analyst Estimates For CPI

May-14 20:01

[Table taken from the MNI CPI Preview - find the full report here, although note the table in the link incorrectly labels auto insurance as airfares]

- Analysts are broadly centered around a 0.3% M/M print for core CPI inflation in April, as seen by those estimates to 2.d.p below.

- The range of supercore CPI estimates is relatively narrow compared to recent months, for the most part close to 0.4% M/M and within 0.3-0.5% M/M.

USDCAD TECHS: Bullish Trend Structure

May-14 20:00

- RES 4: 1.3977 High Oct 13 ‘23 and a key M/T resistance

- RES 3: 1.3899 High Nov 1 and a key resistance

- RES 2: 1.3846/55 High Apr 16 and the bull trigger / High Nov 10 2023

- RES 1: 1.3785 High Apr 30

- PRICE: 1.3647 @ 16:12 BST May 14

- SUP 1: 1.3638 50-day EMA

- SUP 2: 1.3610 Low May 3

- SUP 3: 1.3547 Low Apr 9

- SUP 4: 1.3478 Low Apr 4

A bullish trend condition in USDCAD remains intact for now, despite Thursday’s weakness. Key support to watch is 1.3638, the 50-day EMA. This average was pierced on Friday, but remains intact as a support, for now. A continuation higher would expose the key resistance and bull trigger at 1.3846, the Apr 16 high. Note that moving average studies are in a bull-mode position, highlighting an uptrend.