ASIA: Coming Up in Asia Today

-------------------------------------------- 0200BST 0900HKT 1100AEST BOK Base Rate source: B...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA: Coming Up In Asia Pac Markets On Tuesday

| 2345BST | 0645HKT | 0845AEST | New Zealand May Food Prices |

| 0230BST | 0930HKT | 1130AEST | China May Home Prices |

| 0300BST | 1000HKT | 1200AEST | China May Retail Sales |

| 0300BST | 1000HKT | 1200AEST | China May Industrial Production |

| 0300BST | 1000HKT | 1200AEST | China May Fixed Asset Investment |

| 0300BST | 1000HKT | 1200AEST | China May Property Investment |

| 0400BST | 1100HKT | 1300AEST | South Korea Apr Money Supply |

| 0530BST | 1230HKT | 1430AEST | RBA Cash Rate Target |

| 0630BST | 1330HKT | 1530AEST | RBA Governor Press Conference |

| BoJ Target Rate |

Source: Bloomberg Finance L.P./MNI

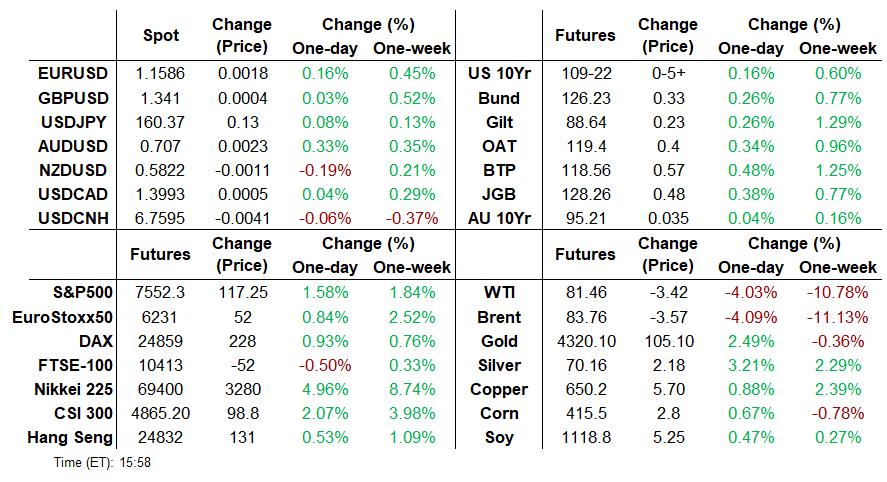

US TSYS: MNI ASIA MARKETS ANALYSIS: US-Iran Respite Sinks Oil, Boosts Stocks

MNI (NEW YORK) -

HIGHLIGHTS:

- US-Iran Memorandum of Understanding buoys risk sentiment and drives oil and the USD lower

- Bond gains capped by heavy US corporate issuance, led by Nvidia

- Attention turns to Tuesday's BOJ and RBA decisions

US TSYS: Light Twist Steepening Ahead Of Busy Central Bank Week

The Treasury curve twist steepened Monday.

- Tsys firmed across the curve in overnight trade, as a US-Iran interim ceasefire agreement (due to be officially signed Friday) was announced.

- However, gains were capped with early gains faded as corporate supply weighed. Issuers attempted to take advantage of the MidEast conflict respite - including $25B Nvidia 7-parter.

- Data was largely 2nd tier, including softer-than-expected but solid-enough Empire Manufacturing and Industrial Production readings that did nothing to shift the macro narrative going into the Fed meeting Wednesday.

- The short-end outperformed throughout the session, led by the 3Y segment (-2bp on the day), though Fed rate hike expectations were little changed across the strip, with only about 1 less basis point of hiking seen through end-2026 (around 17bp cumulative).

- Latest levels: The 2-Yr yield is down 1.3bps at 4.0684%, 5-Yr is down 1.4bps at 4.1916%, 10-Yr is down 0.6bps at 4.473%, and 30-Yr is up 1.1bps at 4.9775%. Sep 10-Yr futures (TY) up 3/32 at 109-19.5 (L: 109-19.5 / H: 110-0)

- Attention overnight turns to monetary policy decisions by the BOJ and RBA, with the Fed among others later in the week.

- Tuesday's data slate is busy but largely second-tier data, including ADP payrolls, import prices, housing starts, and the NY Fed services survey.

- We also get 20Y Treasury Bond reopen Tuesday.

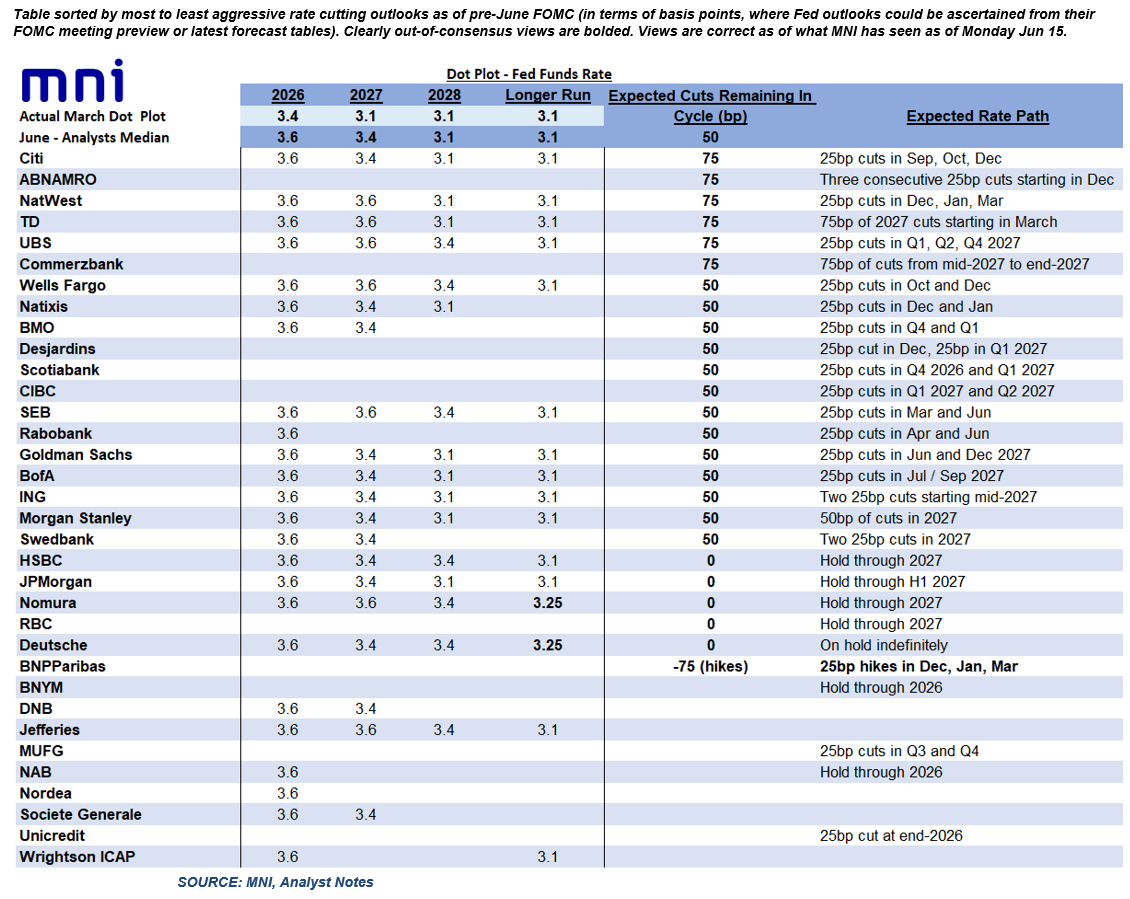

MNI Fed Preview - June 2026: Analyst Outlook

All analysts (among 39 previews seen by MNI) expect the FOMC to hold the Fed funds rate at 3.50-3.75% at its June meeting, with broad consensus over the removal of the Statement easing bias; the 2026 “Dot” in the SEP; and the direction of travel for macro projections. However, there is significant intrigue over Chair Warsh’s first press conference, and the longer-dated Dots.

- Statement: It’s unanimously agreed that the Statement’s easing bias (“in considering the extent and timing of additional adjustments”) will be altered to make the outlook more neutral/two-sided. There doesn’t seem to be much conviction on exactly how it will be changed, with some seeing the removal of “the extent and timing of additional” for example, while some see a more radical change, including NatWest which sees the elimination of forward guidance altogether with the Statement as a whole pared down drastically. Analysts do not expect any dissents, while there is some anticipation that the language assessing the labor market (“Job gains have remained low") could be upgraded.

- SEP/Dot Plot: While it’s firm consensus that the median Dot Plot participant will remove their 2026 rate cut (for a year-end 3.6% rate), it’s more mixed going over the forecast horizon. We’d say consensus is split between those who expect the median Dot to show a hold through 2027, and those who expect one cut. We note some expectations (Deutsche, Nomura) for a higher longer-run dot median (3.25%), helping inform a higher 2028 rate (3.4%, vs most expectations of 3.1%).

- In the economic projections, the most closely-watched aspect is core PCE. This is expected to be increased significantly for 2026 from the existing 2.7% to the low 3.0s area (analysts see anywhere from 2.9% to 3.3%, with a rough 3.2% consensus). 2026 GDP and Unemployment are seen edging slightly lower but outer years largely unchanged.

- Future action: There is consensus among analysts that the Fed has a bit further to go on cuts, though a few see the easing cycle as having already concluded. Compared with the previews we saw going into the last meeting in April meeting, the median analyst’s outlook for total further cuts has not changed from 50bp. However, the timeline has clearly been pushed back with most analysts not seeing cuts restarting until 2027, vs the previous consensus that there would be 25bp cuts in September and December 2026. The big outlier here is BNP Paribas’s forecast for 75bp of hikes starting at end-2026, the only analyst whose Fed preview we saw that has tightening as a base case for the next move.

OPTIONS: US Options Roundup - Jun 15 2026

Monday's US rates/bond options flow included:

- SFRH7 96.00/95.50ps 1x2, sold the 1 at 3.25 in 2k

- SFRU6 96.31/96.37cs, traded 1.5 in 2k

- SFRU6/SFRH7 96.18/96.06ps spread, bought the H7 for 3.75 in 10k total

- SFRV6 96.25/96.43/96.50c ladder, traded flat in 1.5k

- SFRX6 96.06/96.18/96.31c fly, traded 1.5 in 4k

- SFRX6 96.06/96.18/96.31c ladder, traded 2.25 (for the 2) in 1k

- SFRZ6 96.25/95.93ps 2x3, traded 14.25 & 14.5 in 2k

- SFRZ696.18/96.37cs 1x2, traded 1 (for the 2) in 2k

- SFRZ6 96.87/97.12cs, traded 1 in 2k

- SFRZ6 96.50/96.68cs, traded 1.75 in 3.5k

- SFRZ6 96.00p, bought for 12.5 in 5k

- SFRM7 96.31/96.06/95.06p ladder, traded 2.5 in 3k

- 0QN6 95.81/96.06/96.31 iron fly traded 15.5 & 14.5 in 4k

BONDS: EGBs-GILTS CASH CLOSE: US-Iran Detente Triggers Bull Steepening

EGBs and Gilts rallied Monday after the US and Iran reached a tentative ceasefire accord over the weekend.

- A much-awaited US-Iran memorandum of understanding due to be officially signed on Friday will see a 60-day negotiation, with the Strait of Hormuz opened in the meantime (subject to various caveats).

- That saw oil prices sink overnight, bringing front end yields lower in a bull steepening move.

- However, early gains faded somewhat. Heavy US corporate issuance (led by Nvidia seeking to raise at least $20B) weighed on Treasuries, in turn keeping a lid on global core FI.

- In data, Eurozone industrial production was in line with consensus.

- Both the German and UK curves bull steepened on the day, with Gilts outperforming at the short end but underperforming Bunds further down the curve.

- Periphery/semi-core EGB spreads tightened modestly.

- UK data/events dominate the week's European calendar, including CPI and labour market readings, the BOE decision Thursday, and the Makerfield by-election.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 4.5bps at 2.572%, 5-Yr is down 4.8bps at 2.665%, 10-Yr is down 4.1bps at 2.954%, and 30-Yr is down 2.3bps at 3.526%.

- UK: The 2-Yr yield is down 6.2bps at 4.173%, 5-Yr is down 4.4bps at 4.326%, 10-Yr is down 2.4bps at 4.812%, and 30-Yr is down 0.1bps at 5.535%.

- Italian BTP spread down 1.3bps at 71.4bps / French down 0.8bps at 74.7bps

Monday's Europe rates/bond options flow included:

- OEN6 115.25/115.75cs, bought for 13 in 8k total

- OEN6 114.5/114ps, sold at 5 in 3k

- OEN6 115.25/115.75cs, sold at 13 down to 11.5 in 19.3k total (closing).

- ERU6 97.56/97.68cs, bought for 3.75 in 10k

- ERZ6 97.8754c, bought for 1.5 in 18k.

- SFIU6 96.30/96.20/95.40p ladder, sold at 6.75 in 9.5k

- SFIU6 96.10/96.25cs sold at 6.75 in 14k

- SFIZ6 95.95/96.05/96.10/96.20c condor, bought for 0.75 in 2.5k

- SFIH7 96.25/96.50cs vs 95.65/95.40ps, bought the cs for -0.5 in 10k

FOREX: USD Consolidates Moderate Decline Amid Risk-On Mood

- Oil prices extended their three-session decline to around 13% on Monday as further optimism regarding a peace deal in the Middle East buoys global risk sentiment. Alongside further gains for the major equity benchmarks, further short-term pressure has been placed on the US dollar, with the DXY currently 0.2% in the red as we approach the APAC crossover.

- Greenback weakness mechanically translates to EURUSD rising back to the 1.1600 handle, however depressed volatility levels has failed to spur much additional momentum. Resistance to watch is at 1.1640, the 50-day EMA, a clear break of which would signal a possible reversal.

- The risk rally has worked in favour of AUDUSD (+0.43%), which extends its recovery from last week’s lows to around 1.5%. A short-term bear cycle remains in play for the pair, and therefore these gains are considered corrective at this juncture. The recently breached 50-day EMA is the first notable resistance, located at 0.7109 as we approach tomorrows expected hold from the RBA.

- Price action for the Japanese yen has been notably contained in recent weeks, with USDJPY operating within a 1% range across the entirety of June and consolidating around 160.25 on Monday. However, close attention will be on tomorrow’s BOJ meeting/decision, especially given the BoJ is expected to hike rates and there should be mentions of the future pace of the bond buying programme.

- The Swedish Krona was the major beneficiary on Monday, and a 0.95% decline for NOKSEK emphasises the fresh Scandi divergence, helping the cross push cleanly below the 50-day EMA. A 3.4% pullback from the mid-May highs has likely cleaned up the positioning backdrop in NOKSEK ahead of central bank decisions this week, with the primary support level located around the 0.9800 area.

- Aside from Tuesday’s BOJ and RBA decisions, Chinese activity data, German ZEW and US import prices/building permits highlight the calendar.

FX OPTIONS

FX OPTIONS: Expiries for Jun16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1540(E1.4bln), $1.1600(E1.2bln), $1.1700(E911mln), $1.1830(E1.3bln)

- USD/JPY: Y157.00($1.3bln), Y158.00($2.2bln), Y164.00($1.7bln)

- GBP/USD: $1.3385-00(Gbp715mln), $1.3440-45(Gbp650mln), $1.3500-15(Gbp1.4bln)

- USD/CAD: C$1.3735-50($1.4bln), C$1.3900($570mln)

| Date | GMT/Local | Impact | Country | Event |

| 16/06/2026 | 0200/1100 | *** | BOJ Policy Rate Announcement | |

| 16/06/2026 | 0200/1000 | *** | Fixed-Asset Investment | |

| 16/06/2026 | 0200/1000 | *** | Retail Sales | |

| 16/06/2026 | 0200/1000 | *** | Industrial Output | |

| 16/06/2026 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 16/06/2026 | 0430/1430 | *** | RBA Rate Decision | |

| 16/06/2026 | 0800/1000 | ** | Italy Final HICP | |

| 16/06/2026 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 16/06/2026 | 0900/0500 | * | CREA Existing Home Sales | |

| 16/06/2026 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 16/06/2026 | 1200/0800 | * | NY Fed SOFR | |

| 16/06/2026 | 1215/0815 | *** | ADP Employment Report | |

| 16/06/2026 | 1230/0830 | *** | Housing Starts | |

| 16/06/2026 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 16/06/2026 | 1230/0830 | ** | Import/Export Price Index | |

| 16/06/2026 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 16/06/2026 | 1300/0900 | * | NY Fed EFFR | |

| 16/06/2026 | 1310/1510 | ECB Lane Conversation at Reuters NEXT Europe Event | ||

| 16/06/2026 | 1700/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 17/06/2026 | 2350/0850 | * | Machinery Orders | |

| 17/06/2026 | 0600/0700 | *** | Consumer Inflation Report) | |

| 17/06/2026 | 0600/0700 | *** | Producer Prices | |

| 17/06/2026 | 0700/0900 | ECB Cipollone Fireside Chat at Salzburg Global Finance Forum | ||

| 17/06/2026 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 17/06/2026 | 0730/0930 | ECB Cipollone Panel on Future of Money at Salzburg Global Finance Forum | ||

| 17/06/2026 | 0900/1100 | *** | EZ HICP Final | |

| 17/06/2026 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 17/06/2026 | 1200/0800 | * | NY Fed SOFR | |

| 17/06/2026 | 1230/0830 | *** | Retail Sales | |

| 17/06/2026 | 1300/0900 | * | NY Fed EFFR | |

| 17/06/2026 | 1400/1000 | ** | NAR Pending Home Sales | |

| 17/06/2026 | 1400/1000 | * | Business Inventories | |

| 17/06/2026 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 17/06/2026 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/06/2026 | 1800/1400 | *** | FOMC Statement | |

| 18/06/2026 | 2245/1045 | *** | GDP |

US TSYS: Light Twist Steepening Ahead Of Busy Central Bank Week

The Treasury curve twist steepened Monday.

- Tsys firmed across the curve in overnight trade, as a US-Iran interim ceasefire agreement (due to be officially signed Friday) was announced.

- However, gains were capped with early gains faded as corporate supply weighed. Issuers attempted to take advantage of the MidEast conflict respite - including $25B Nvidia 7-parter.

- Data was largely 2nd tier, including softer-than-expected but solid-enough Empire Manufacturing and Industrial Production readings that did nothing to shift the macro narrative going into the Fed meeting Wednesday.

- The short-end outperformed throughout the session, led by the 3Y segment (-2bp on the day), though Fed rate hike expectations were little changed across the strip, with only about 1 less basis point of hiking seen through end-2026 (around 17bp cumulative).

- Latest levels: The 2-Yr yield is down 1.3bps at 4.0684%, 5-Yr is down 1.4bps at 4.1916%, 10-Yr is down 0.6bps at 4.473%, and 30-Yr is up 1.1bps at 4.9775%. Sep 10-Yr futures (TY) up 3/32 at 109-19.5 (L: 109-19.5 / H: 110-0)

- Attention overnight turns to monetary policy decisions by the BOJ and RBA. Tuesday's data slate is busy but largely second-tier data, including ADP payrolls, import prices, housing starts, and the NY Fed services survey.

- We also get 20Y Treasury Bond reopen Tuesday.