ASIA: Coming Up In Asia Pac Markets On Friday

Sep-11 21:04

| 2330BST | 0630HKT | 0830AEST | New Zealand Aug BusinessNZ Mfg PMI |

| 2345BST | 0645HKT | 0845AEST | New Zealand Aug Card Spending |

| 0430BST | 1130HKT | 1330AEST | Japan 3mth Bill Sale |

| 0440BST | 1140HKT | 1340AEST | RBA Jones Speech |

| 0530BST | 1230HKT | 1430AEST | Japan July F IP |

| 0530BST | 1230HKT | 1430AEST | Japan July Capacity Utilization |

Source: Bloomberg Finance L.P/MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

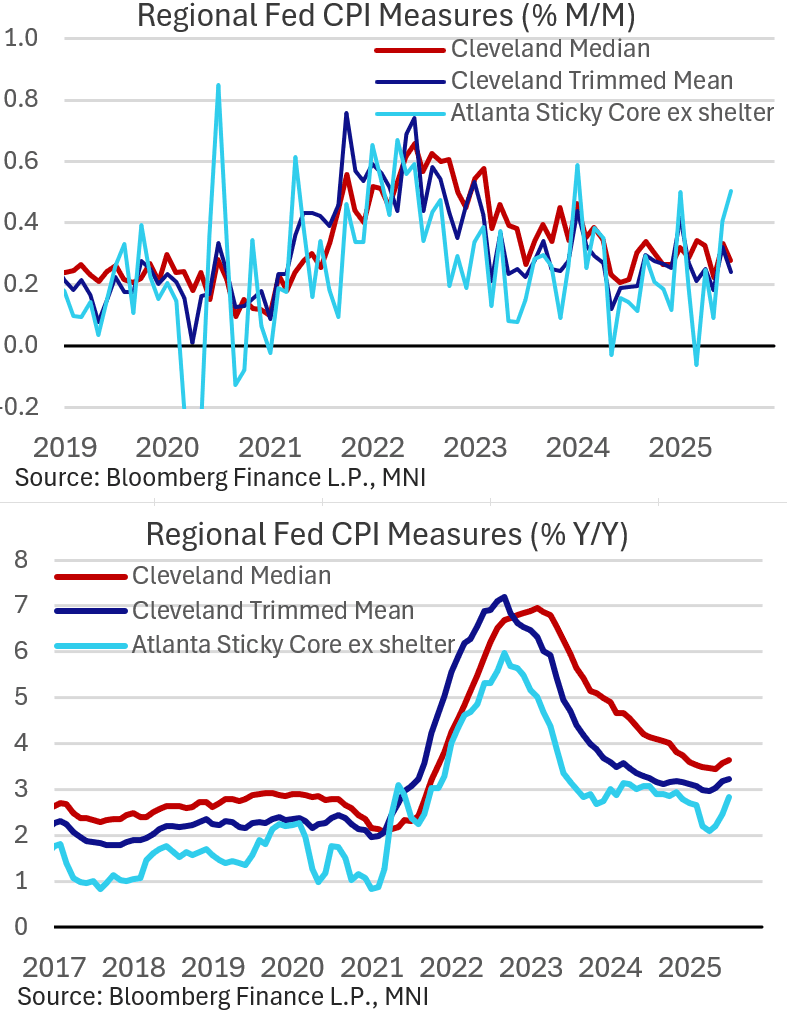

US INFLATION: Regional Fed Metrics Show Sticky Above-Target Inflation

Aug-12 20:52

Both the Cleveland and Atlanta Fed's core inflation metrics released post-CPI showed largely worrying developments in July, adding to evidence that underlying inflation has already bottomed out above the Federal Reserve's 2% target.

- The Atlanta Fed's "sticky" CPI readings came in on the warm side, with the total Y/Y at a 5-month high 3.43% after 3.31% prior. Ex-shelter picked up to an 8-month high 2.95% Y/Y after 2.63%, with the M/M reading rising to a joint-18 month high 0.46% after 0.40% in June. This brought the 6-month annualized rate to 3.99%, a 16-month high.

- The core "sticky" CPI measures were no better: ex-shelter M/M rose to 0.50% from 0.40%,the latest figure being a joint 18-month high, pushing the 6-month annualized rate up to a 16-month high 4.08%. The Y/Y core CPI rate is running at 3.42% (5-month high), with ex-shelter running at 2.83% (8-month high) whereas as recently as April it was basically in line with the 2% target for the first time since early 2021.

- To put these into perspective: While July's core Y/Y CPI reading picked up to 3.06% from 2.93% prior for a 5-month high, the 6-month annualized rate actually fell to a 52-month low 2.43% Y/Y from 2.69% prior.

- The Cleveland Fed's readings were more ambiguous. The median CPI reading came in at 3.65% Y/Y for a 6-month high, up from 3.59% a month earlier. The M/M metric was better-behaved at 0.28% however (after 0.33%). Similar dynamics were seen in the Trimmed Mean 16% measure: the 3.22% Y/Y was a 12-month high, though the 0.24% M/M was down from 0.32% prior (which had been a 5-month high).

US TSYS: Lack Of Core Goods CPI Acceleration Triggers Twist Steepening

Aug-12 20:14

The Treasury curve twist steepened Tuesday as the key details of the July CPI report came in softer than widely expected.

- Despite a further acceleration in monthly core inflation in July, there was an unexpectedly steady rate of core goods CPI - key to the overall inflation outlook given expectations for tariff passthrough to accelerate this summer. (MNI's Inflation Insight has more details, PDF here).

- The short-end saw a post-CPI rally, buoyed by deepening Fed cut expectations: a 25bp reduction in September is now 94% priced (up from about 88% Monday), with 60bp of cuts through end-2025 (up from 57bp Monday).

- This wasn't greatly dampened by Fed hawks Barkin and Schmid who expressed no urgency to cut rates in the near future.

- The long end, conversely, sold off after an initial rally. German Bunds appeared to lead the retracement, amid heavy volumes there albeit with little obvious catalyst. However some of the sell-off came after President Trump said on social media that he was considering a "major lawsuit" against Fed Chair Powell over Federal Reserve building renovation cost overruns.

- Latest cash levels: the 2-Yr yield is down 3.8bps at 3.7308%, 5-Yr is down 1.6bps at 3.8207%, 10-Yr is up 0.2bps at 4.2868%, and 30-Yr is up 2.1bps at 4.8736%. Sep 10-Yr futures (TY) down 2/32 at 111-26.5 (L: 111-19.5 / H: 112-06)

- Wednesday's data calendar is lighter (ahead of PPI and retail sales later in the week), with weekly MBA mortgage data in the morning, though we hear from a few FOMC participants including Barkin, Goolsbee, and Bostic.

FOREX: USD Slides as CPI Clears Way for Sept Fed Cut

Aug-12 20:03

- The USD slid against all others Tuesday as the July CPI print cleared the path for the Fed to resume rate cuts from the September meeting. Core goods inflation undershot expectations for a further acceleration in M/M terms, and while still a solid monthly clip compared to 2024 levels, there few sufficient signs of tariff-led inflation that could derail easing both in September, as well as further rate cuts before year-end.

- The resultant USD Index weakness pushed the price back below the 50-dma, testing last week's lows in the process. Medium-term, this clears markets for a test of the late July pullback lows of 97.109 - a level that should see firm support.

- EUR was the primary beneficiary of the USD pullback, and EUR/JPY extended gains above 172.50 for the first time since July - keeping momentum pointed higher and tilting focus toward the YTD highs of 173.97. In addition, GBP/USD saw support, with the CPI reaction prompting a new weekly high and a test at the 50-dma of 1.3502. Clearance above this level would further reverse the downleg off the late July high and put markets near 3% off the early August low.

- Despite the post-RBA weakness, AUDUSD is yet to challenge any meaningful support. The pair rallied well off the week's lowest levels last week on broad USD weakness - erasing any signs of a bearish breakout on the show through the 20- and 50-day EMAs. While support at 0.6455 the Jul 17 low, has been cleared, the recovery in prices keeps key resistance in focus at 0.6625 the Jul 24 high.

- Focus Wednesday shifts to Japanese PPI data, German final CPI and appearances from Fed's Barkin and Schmid.