LNG: China's LNG Imports Were 26% Lower y/y In April

May-01 09:31

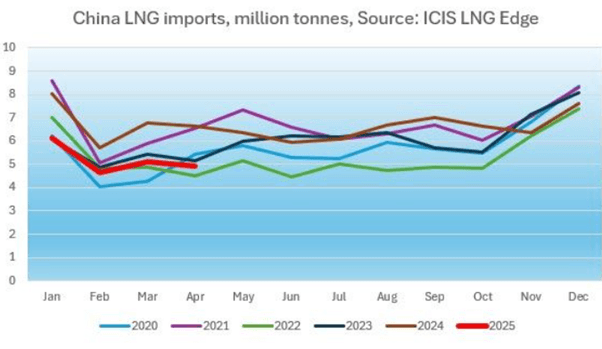

China’s LNG imports were 26% lower y/y in April, while Jan-April imports were down 23% y/y, according to ICIS analyst Alex Froley.

- The share of China’s own production and pipeline imports from Russia through the Power of Siberia pipeline has grown, while total gas demand is also slowing, Froley says.

- Chinese companies have long-term contracts for LNG cargoes from the US and elsewhere, but can resell many of these to alternative destinations and have been doing so even before the introduction of tariffs, according to Froley.

- China’s importers have diverted most of their contracted LNG from the US to Europe due to tariffs. which has helped to boost European supplies as the region looks to restock gas storage.

Source: ICIS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Put spread buyer

Apr-01 09:21

ERK5 97.75/97.6875ps, bought for 1.25 in 6k.

EUROPEAN INFLATION: Services Deceleration Continues in March EZ HICP

Apr-01 09:11

Eurozone March flash HICP Y/Y inflation came in at 2.18%, 0.02 hundredths below the rounded consensus of 2.2% (vs 2.32% February). On a monthly basis, Eurozone inflation came in at 0.61% (0.6% cons, 0.43% prior). The data on services in the release should be seen as a good sign regarding tapering stickiness in the category.

- Core HICP printed below consensus, at 2.41% Y/Y and 0.95% M/M (2.5% cons; Feb 2.57% Y/Y, 0.55% M/M).

- Looking at the individual categories:

- Services inflation notably decelerated to 3.42% Y/Y; rounded to 1dp, there has not been a print lower than 3.4% since April 2022. The median sellside analyst estimate ahead of the national data stood at 3.5% - so that looks like a bit of a downside surprise.

- Energy came in at -0.74% Y/Y, with the deceleration vs February's 0.19% underpinned by a sequential fall (M/M at -1.17%) - this looks broadly in line with expectations.

- Non-energy industrial goods printed 0.63% Y/Y, the category has remained between 0.44% and 0.70% since last May and this broadly in line with analyst consensus.

- Food, alcohol and tobacco inflation, as expected, accelerated in March, at 2.90% Y/Y, above February's 2.66% but also broadly line w/ expectations.

- Looking at the national-level prints, headline HICP inflation accelerated in 7 countries in March vs Feb (Netherlands, Austria, Estonia, Latvia, Malta) despite the overall decrease in headline.

EQUITIES: EU Bank put spread

Apr-01 09:11

SX7E (17th Apr) 180/165ps 1x1.5, bought for 0.90 in 7.2k.