CHINA PRESS: China's Industrial Profits Fall At Slower Pace In July

China's industrial enterprises saw their operating income grow by 0.9% y/y, while their total profits decreased by 1.5% y/y, narrowing for the second month by 2.8 percentage points from June, Shanghai Securities News reported citing data by the National Bureau of Statistics. A 6.8% growth in profits made by manufacturing companies, which accelerated 5.4 pp from June, helped to drive the headline number by 3.6 pp. The profit recovery is expected to continue on government efforts to stabilise the economy and curb price wars as well as fading disturbances caused by extreme weather, the newspaper said citing analysts.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: JPY Crosses - Pullback As Risk Sees Profit Taking Heading Into A Big Week

The move higher in US stocks finally stalled as some risk is taken off heading into a big week. This morning has seen US futures open slightly higher, ESU5 +0.10%, NQU5 +0.20%. If risk continues to trade well then this should provide the JPY crosses with a tailwind to move higher, the event-risk posed by this week though could provide some short-term challenges.

- EUR/JPY - Overnight range 172.07 - 173.78, Asia is trading around 172.25. This pair has had a decent move higher and has led the charge against the JPY longs. Short-term it is starting to look a little stretched but the direction is clear and should expect demand on dips. First support 170.00 area then the more important 168.00 area.

- GBP/JPY - Overnight 198.33 - 199.21, Asia trades around 198.35. The pair continues to find strong demand around its 198.00 support. It is looking to regain its momentum for a push higher from this base.

- NZD/JPY - Overnight range 88.50 - 88.90, Asia is currently dealing 88.70. The pair is challenging its recent multiple highs towards 89.00, can it look past the risks of this week and extend higher ? Above here and the focus will turn to the 90.00/91.00 area.

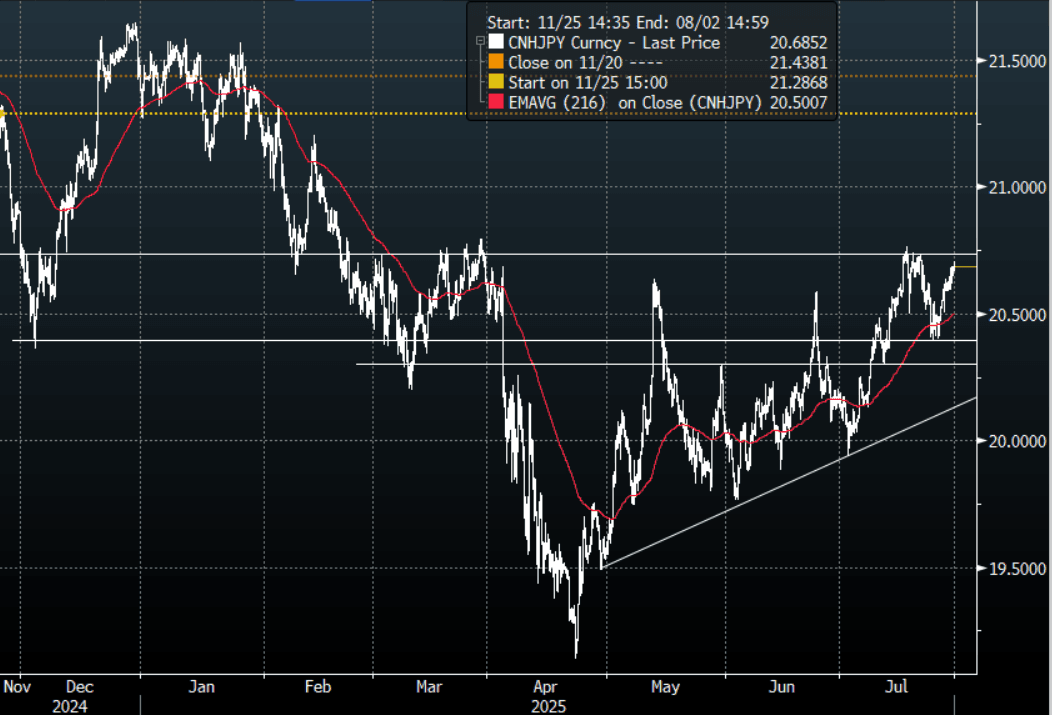

- CNH/JPY - Overnight range 20.6154 - 20.6867, Asia is currently trading around 20.6900. This pair found strong demand towards its 20.3000/20.4000 support area, can it regain the upward momentum ? A sustained move back below 20.3000 would be needed to turn the pendulum back towards the Bears.

Fig 1 : CNH/JPY 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSTRALIA: Q2 Core Inflation Expected To Be 0.1pp Above RBA Forecast At 2.7%

Q2 CPI prints Wednesday and will be monitored closely given that the RBA relies on this series with the monthly version not yet complete (due to take place on November 26). Headline inflation continues to be distorted by federal & state government electricity rebates and so attention will remain on the underlying trimmed mean. Bloomberg consensus expects it to rise 0.7% q/q and for the annual rate to ease to 2.7% y/y from Q1’s 2.9%. The RBA’s May forecast was for 2.6% y/y and so a print close to this would likely result in an August cut but steady around Q1 may add doubt.

- Most analysts reporting to Bloomberg are around consensus at 2.6-2.7% y/y but forecasts range from 2.5-2.8% and the quarterly rate 0.5-0.8%. In terms of the major local banks, NAB and Westpac are in line with consensus, CBA expects 0.7% q/q but the annual rate to rise to 2.8%, while CBA has a slightly lower quarterly increase of 0.6% but annual inflation still 2.7%.

- Services inflation will continue to be watched as a measure of domestically-generated pressures. After being sticky through 2024, core services moderated to 3.3% y/y in Q1 from 4.2%.

- Q2 headline CPI is forecast to rise 0.8% q/q and 2.2% y/y after 0.9% q/q and 2.4% y/y in Q1. The RBA projected 2.1% y/y in May. CBA and NAB are in line with consensus, ANZ is forecasting 0.8% q/q & 2.1% y/y but Westpac is higher with 0.9% q/q & 2.3% y/y.

- Monthly June data are also released Wednesday and headline inflation is expected to be steady at 2.1% with forecasts ranging from 2.1% to 2.5%. ANZ and CBA are in line with expectations, NAB is lower at 2% and Westpac higher at 2.3%.

USD: US-EU Trade Deal Adds Fuel To The Paring Back Of Extreme Shorts

The BBDXY range overnight was 1198.76 - 1208.24, Asia is currently trading around 1208. The USD’s slide lower finally stalled at the back end of last week and some profit-taking was seen. Yesterday's US-EU trade deal was seen as a big loss for the European Union and this has provided the USD bounce with further tailwinds. There is lots of event risk coming up this week and we are heading into month-end so some caution is warranted, this could potentially see some more paring back of USD shorts. Today is corporate month-end and this could also add to some short-term USD demand putting further pressure on the shorts.

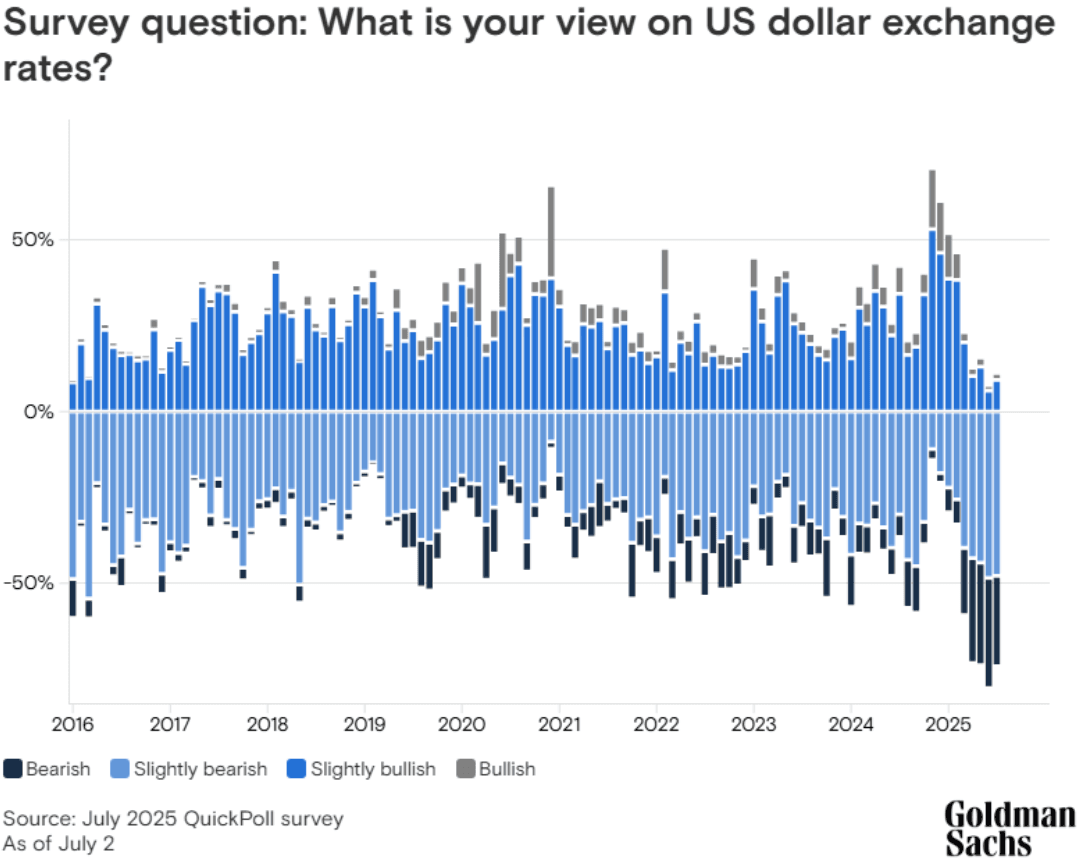

- Daily Chartbook on X: “In "a survey of 800 institutional investors ... The proportion of respondents expecting the dollar to weaken amid growing US fiscal concerns is near an all-time high -Goldman Sachs.” See Graph below.

- Arnaud Bertrand on X: “If Europeans were paying attention (or being told the truth), they should be beyond appalled by this "deal. It's nothing more than one of the most expensive imperial tributes in history. Just a massive one-way transfer of wealth with no reciprocal benefits.”

- Robin Brooks on X: “Today's rise in the Dollar is very unusual. Usually, such increases in the Dollar (vertical) map into a favorable move in the 2y2y forward rate differential (horizontal), but that isn't the case today. That could be a sign that Dollar short positioning is extremely stretched...”

- “The Dollar is seeing a big rise. Several drivers: (i) EU - US trade deal is reminder that - having dropped the ball on Ukraine - EU is supplicant, not master; (ii) tariffs are Dollar-positive, the fact that they drove the Dollar down was always an anomaly. The Dollar has based...”

- There is a broad consensus that the USD is set to embark on a decent move lower as the world reduces its exposure to the US and repatriates a lot of these flows. This consensus will also result in some decent short squeezes as a lot of the market is positioned the same way.

- Data/Events : Advanced Goods Trade Balance, FHFA House Price Index, S&P Corelogic, JOLTS, Conf. Board Consumer Confidence, Dallas Fed Services Activity.

Fig 1: Goldman Survey On USD View

Source: MNI/@dailychartbook/Goldman Sachs