EM ASIA CREDIT: China Water Affairs Group: New USD priced

(CWAHK, Ba1/BB+/NR)

"PRICED: China Water Affairs $150m 5NC3 Guar. Blue to Yield 6.125%" - BBG

China Water Affairs priced its new USD150m 5NC3 note after close, more or less in line with our fair value estimate (6.1-6.2% area).

New Issue: USD150m 5NC3

IPT: 6.375% area

Final: 6.125%

FV estimate: 6.2% area

Our fair value estimate: https://mni.marketnews.com/4oq8eAd

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Stronger After A Modest Rally From US Tsys

In local morning trade, NZGBs are 2-3bps richer after US tsys finished with a modest rally.

- There was little in the way of meaningful fresh drivers but with pre-FOMC positioning and Trump’s continued call for rate cuts (“bigger” than Powell “had in mind”) possibly at play.

- The move started beforehand but won’t have been hindered by a soft Empire manufacturing survey which saw new orders fall 35 points to their lowest since Apr 2024.

- Today will see retail sales and import prices for August in focus, all ahead of the FOMC decision on Wednesday.

- In August, NZ electricity, gas, food, rents, and tobacco prices all rose slightly, while alcohol, petrol, and both domestic and international airfares declined, with diesel recording a small increase. NZ food prices rose 0.3% from a month earlier.

- Swap rates are 2bps lower.

- RBNZ dated OIS pricing is little changed across meetings. 22bps of easing is priced for October, with a cumulative 40bps by November 2025.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-34 bond.

GOLD: Gold Reaches New Record High Ahead Of Fed

Gold reached a new record high of $3685.64/oz on Monday as the US dollar softened (BBDXY -0.3%) and Treasury yields were lower ahead of Wednesday’s Fed decision. It is the main event for the week and as a 25bp rate cut is widely expected, the tone of the statement and Chair Powell’s comments will be monitored closely to gauge the outlook for policy. Bullion was 1% higher yesterday at $3678.99 to be up 6.7% this month and is currently around $3678.6.

- Gold’s break above the previous record high of $3674.3 has opened up round number resistance at $3700. The metal remains in a clear bull cycle. Initial support is at $3579.7, 8 September low.

- Geopolitical uncertainty around pressure to increase sanctions on Russia and impose tariffs on those who buy its energy and uncertainty regarding the outcome of attacks on Fed independence are also supporting gold prices. Central banks, especially the PBoC, are also buying the yellow metal.

- Silver was 1.2% higher at $42.681 after a peak of $42.742 and is now up 7.5% in September. It is currently around $42.612, above resistance at $42.606 opening $42.974. Initial support is at $40.195, 20-day EMA.

- Equities were generally stronger on Monday with the S&P up 0.5% and Euro stoxx +0.9% but FTSE down 0.1% and the S&P e-mini is currently -0.1%. Oil prices were higher with Brent +0.7% to $67.47/bbl. Copper rose 1.4%.

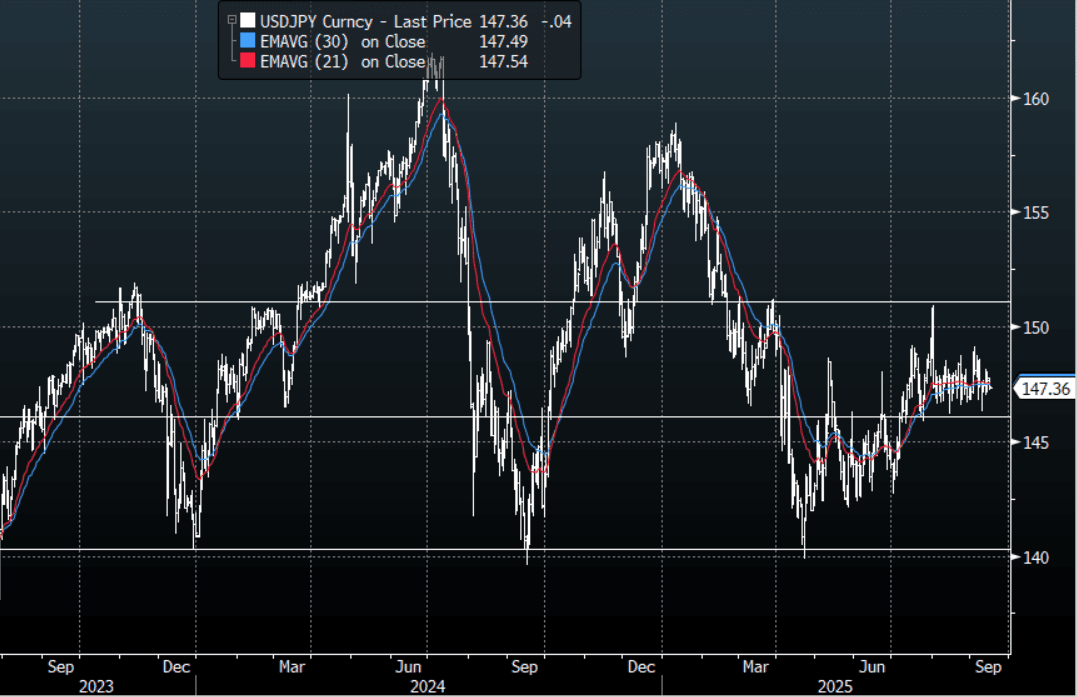

JPY: USD/JPY - Treads Water Ahead Of FOMC & BOJ

The overnight range was 147.23-147.61, Asia is currently trading around 147.35. USD/JPY continues to trade sideways with no clear trend. The price remains in the middle of its recent 146-149 range, and we need a convincing break to see a clearer direction again. CFTC data shows leveraged funds paring back some of their short JPY position last week but remain core short, looking for this support to continue to hold. A move back below 145/146 is needed to potentially start seeing these positions being flushed out.

- MNI BOJ WATCH: Board To Hold, Focus On CPI, Trade. The Bank of Japan board is likely to keep its policy rate unchanged at 0.50% at the two-day meeting ending Friday as it assesses the impact of tariffs on the U.S. and Japanese economies.

- MNI FED PREVIEW: A Reluctant Return to Easing. The Federal Reserve is set to resume its easing cycle at the September 16-17 meeting with a 25bp cut to the funds rate range to 4.00-4.25%. The decision to cut after a 5-meeting pause was well-telegraphed by Chair Powell, whose Jackson Hole speech described a “shifting balance of risks” toward a weaker labor market that “may warrant adjusting our policy stance”. The updated quarterly projections aren’t likely to bring many changes to the macroeconomic variables, but as usual the signal sent from the Fed rate “Dot Plot” will garner attention. A Committee split between expecting one or two further cuts this year is likely, keeping each of the remaining meetings of 2025 “live”.

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.00($1.49b), 146.00($1.41b), 145.00($838m).Upcoming Close Strikes : 145.00($1.32b Sept 19), 145.70($1.22b Sept 17), 146.40($797m Sept 19), - BBG.

- CFTC data shows last week asset managers again added to their JPY longs again as they look to rebuild their position +87239( Last +78427), leveraged funds reduced their short position perhaps losing confidence the support will continue to hold -49591(Last -66914).

- Data/Event : Tertiary Industry Index

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P