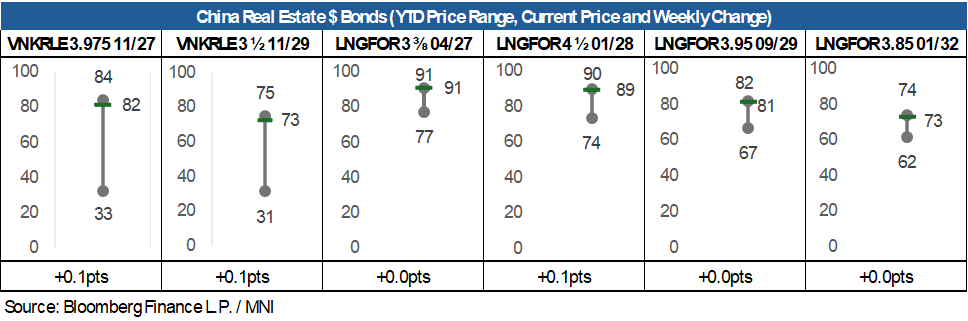

EM ASIA CREDIT: China Real Estate: Valuations settle ahead of possible support

The positive momentum surrounding yesterday's unconfirmed reports that the Chinese government will discuss new measures to support the real estate sector were not sustained. Vanke rose 1pt on the news, and like peer Longfor are trading at the highs of the YTD range. We continue to think that valuations already assume ongoing State support for the sector, and any new support will have only a marginal positive impact on valuations.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JAPAN: MOF Says July Bond Buyback Speculation Is Unrealistic - BBG

Headlines have crossed via BBG from Japan's MOF that speculation around July bond buybacks is unrealistic.

- BBG notes: " Buying back of super-long government bonds from July is unrealistic and not envisioned, an official from Japan’s Ministry of Finance said in an email to Bloomberg News."

- This follows recent speculation around various shifts/efforts that the Japan authorities may enact to calm longer dated yields. This could involve shifts in BoJ taper plans, along with potential changes to government bond issuance plans (with a focus on more shorter dated issuance).

- Note Rtrs reported yesterday: "Japan is considering buying back some super-long government bonds issued in the past at low interest rates, two sources with direct knowledge of the plan said on Monday, underscoring its focus on reining in any abrupt rises in bond yields." See this link.

- Market reaction has been limited in terms of JGB futures. June futures are still close to session highs, last near 139.30, while USD/JPY is relatively steady, near 145.00.

FOREX: Asia FX Wrap - Quiet Session Ahead Of US CPI

The BBDXY has had a range of 1209.44 - 1212.04 in the Asia-Pac session, it is currently trading around 1211.”With weaker data eroding the UK’s relative yield advantage and the Federal Reserve clinging to its higher-for-longer script, GBP/USD now faces a more challenging landscape. The pound has rallied nearly 8% year-to-date against the dollar, but the backdrop may be shifting”(BBG). PPG Macro on X: “UK (un)employment. HMRC PAYE employees total for May fell 109k. Even allowing for revisions, payrolled employment has fallen for 7 months in a row. 6-month average fall of 41.7k. The equivalent of nonfarm payrolls falling at over 200k a month.”

- EUR/USD - Asian range 1.1406 - 1.1439, Asia is currently trading 1.1415. EUR has drifted down during the Asian session in response to the move lower in US stocks. Dips should continue to find demand, first support around 1.1350 then the 1.1100/1200 area.

- GBP/USD - Asian range 1.3475 - 1.3510, Asia is currently dealing around 1.3485. The GBP looks to be failing in its attempt to gain any momentum above the pivotal 1.3500 weekly pivot. Poor data yesterday capped the move, support seen back towards 1.3400 and then 1.3200.

- USD/CNH - Asian range 7.1823 - 7.1897, the USD/CNY fix printed 7.1815. Asia is currently dealing around 7.1865. Sellers should be around on bounces while price holds below the 7.2500 area.

- Cross asset : SPX -0.29%, Gold $3340, US 10-Year 4.47%, BBDXY 1211, Crude oil $64.95

Data/Events : US CPI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

BONDS: NZGBS: Closed With A Twist-Flattener Ahead Of US CPI

NZGBs closed showing a twist-flattener, with yields 2bps higher to 1bp lower.

- Bloomberg - "New Zealand's annual net immigration fell to 21,317 in April, a two-and-a-half-year low, which could slow the country's economic recovery and lead to more interest-rate cuts."

- "The decline in net immigration is partly driven by New Zealand citizens leaving the country to seek better incomes, which could dampen demand and prompt the Reserve Bank to provide policy stimulus."

- Cash US tsys are little changed in today's Asia-Pac session ahead of today's CPI data.

- Focus has also been firmly on US-China trade talks, with headlines from London crossing earlier. The market reaction has been fairly muted, with the main outcome being agreement to move forward with what was agreed at the Geneva talks in May (although both US and Chinese leaders need to sign off on implementation).

- Swap rates closed showing a flatter curve, with yields 2bps higher to 2bps lower.

- RBNZ dated OIS pricing closed firmer across meetings. 4bps of easing is priced for July, with a cumulative 27bps by November 2025.

- Tomorrow, the local calendar will see Card Spending data, ahead of BusinessNZ Manufacturing PMI on Friday.