US NATGAS: Chicago Natgas Fundamentals

Aug-29 17:55

The total supply-demand balance currently shows a surplus of around 1788 mmcf/d, widening from a 1591 mmcf/d surplus the previous day.

- End user demand is down 67 mmcf/d to 1.68 bcf/d. This compares to the 30-day average of 2.05 bcf/d.

- The latest GFS 15-day forecast for Chicago has total CDDs at 90 which is an increase of 9 CDDs compared to the previous run. It is 13 CDDs colder than the 10-year normal.

- Net pipeline inflows into the region are showing at 3.53 bcf/d today up 0.12 bcf/d on the day. This is 2.95 bcf/d above the 30-day average of 0.58 bcf/d.

- Data from Bloomberg is of time of publishing and is subject to change throughout the day.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

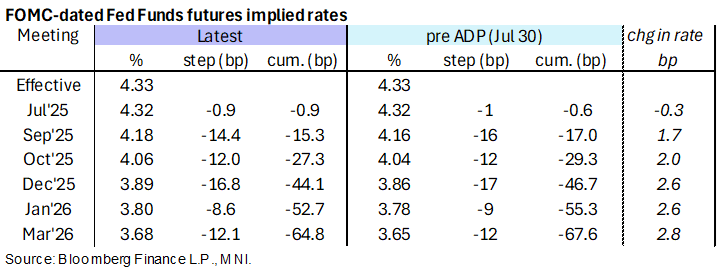

STIR: Snapshot Of Fed Rate Path Pre-FOMC Decision

Jul-30 17:53

- Today’s mostly robust economic data have helped see Fed Funds implied rates shift back a little closer to recent hawkish extremes when it comes to 2025 meetings.

- The 44bp of cuts eyed to year-end is off last week’s 42bp which was the fewest cuts sustainably priced since February.

- With no rate change expected today (just 1bp priced), a snapshot of near-term meetings:

Cumulative cuts from 4.33% effective: 15.5bp Sep, 27.5bp Oct, 44bp Dec, 52.5bp Jan and 65bp Mar. - The SOFR implied terminal yield of 3.20% (SFRH7) is 3bp higher on the day, firmly within 3.1-3.3% range seen through July.

- President Trump shortly ahead of the meeting: "*TRUMP: I HEAR FED WILL CUT RATES IN SEPTEMBER" - bbg

BONDS: EGBs-GILTS CASH CLOSE: Flatter Curves Amid Heightened Data Flow

Jul-30 17:48

European curves flattened Wednesday.

- Early trade was constructive for EGBs and Gilts, stemming from the prior session's late strength in US Treasuries.

- A solid long-end Gilt tender and potentially some month-end dynamics also assisted. 10Y Gilt yields briefly hit their lowest intraday level since Jul 22; for Bunds Jul 24.

- Above-expected US data including private payrolls and GDP triggered a selloff in Treasuries that weighed across the Atlantic, seeing yields finish off their lows.

- Earlier, a slew of Eurozone data didn't really move the needle for markets: Euro Q2 GDP and July consumer confidence were slightly stronger than expected, while Spanish flash July inflation was slightly above-consensus and Belgian HICP decelerated. The ECB's forward looking wage tracker points to a continued decline in negotiation wage growth in Q1 2026.

- The German curve twist flattened, with the UK's bull flattening. Periphery/semi-core EGB spreads were mixed.

- The Federal Reserve decision will be a focus overnight, with Thursday bringing French, Italian, and German flash July inflation data (MNI's preview is here).

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.2bps at 1.954%, 5-Yr is up 0.3bps at 2.296%, 10-Yr is down 0.2bps at 2.706%, and 30-Yr is unchanged at 3.204%.

- UK: The 2-Yr yield is down 1.8bps at 3.876%, 5-Yr is down 2.6bps at 4.041%, 10-Yr is down 3bps at 4.603%, and 30-Yr is down 2.5bps at 5.416%.

- Italian BTP spread up 0.4bps at 81.4bps / French OAT down 0.3bps at 65.3bps

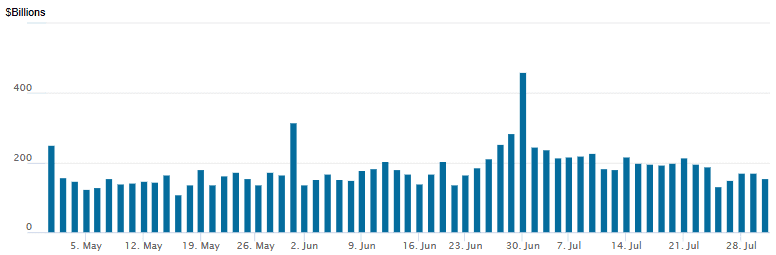

US: FED Reverse Repo Operation

Jul-30 17:37

RRP usage retreats to $155.481B this afternoon from $171.018B yesterday, total number of counterparties at 27. Usage had fallen to $54.772B on Wednesday, April 16 -- lowest level since April 2021 - compares to July 1: $460.731B highest usage since December 31.