JGBS: Cash Bonds Mostly Cheaper At Lunch

Aug-08 02:35

At the Tokyo lunch break, JGB futures are weaker but off session lows, -8 compared to settlement levels.

- (MNI) Some Bank of Japan board members acknowledged upside risks to prices but saw no need to rush a rate hike at the July 30-31 meeting, the summary of opinions showed Friday. But one member noted that it would take at least two-to-three more months to gauge the effects of U.S. tariff policy. "If the U.S. economy is able to withstand the impact to a greater extent than expected, the downward effects on Japan's economy are likely to remain minimal. In that case, it may be possible for the Bank to exit from its current wait-and-see stance, perhaps as early as the end of this year.”

- Cash US tsys are slightly mixed in today's Asia-Pac session after yesterday's modest sell-off.

- Cash JGBs are flat to 2bps cheaper across benchmarks out to the 30-year, with the 4-5-year underperforming and the 40-year outperforming (-3bps). The benchmark 10-year yield is 1.4bps higher at 1.502% versus the cycle high of 1.616%.

- Swap rates are 1-2bps higher.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBNZ: On Hold, Considered Cutting Rates By 25bps, Awaiting More Information

Jul-09 02:32

As widely expected, the RBNZ held the policy rate steady at 3.25%. This was in line with the sell-side consensus (although some forecasters saw risks of a 25bps cut), while market pricing only gave a very small chance to a cut today.

- The RBNZ gave a nod to stronger near term inflation pressures, it noted: "Annual consumers price inflation will likely increase towards the top of the Monetary Policy Committee’s 1 to 3 percent target band over mid-2025. However, with spare productive capacity in the economy and declining domestic inflation pressures, headline inflation is expected to remain in the band and return to around 2 percent by early 2026."

- On growth, it saw supports from higher export prices and lower interest rates. It noted the better Q4/Q1 growth trends but recognized softer trends more recently (April and May figures). It expects the lower rates backdrop (along with higher commodity prices) to support a gradual recovery in activity.

- The central bank emphasized considerable uncertainty around both the domestic and international economic outlooks. On the international side this reflected the tariff/trade outlook. Locally, the RBNZ noted: "The Committee noted uncertainty about the speed with which the domestic economy would continue recovering. Some members highlighted that prolonged economic uncertainty might induce further precautionary behaviour by households and firms. "

- Still, it added: "In contrast, other members emphasized stronger household consumption and business investment in the March quarter, along with higher surveyed investment intentions in the June quarter, as possible signals of a recovery in interest rate sensitive parts of the economy."

- The RBNZ considered two options at this meeting, to cut by 25bps or hold policy steady. The case to ease largely reflected concerns around faltering economic momentum. The case to hold won out, amid high uncertainty: The RBNZ noted: "Some members emphasized that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve."

- The central bank maintained an easing bias, subject to medium term inflation pressures easing.

- Note that Q2 CPI for NZ prints on July 21.

BONDS: NZGBS: Cheaper After RBNZ’s Decision To Leave OCR Unchanged

Jul-09 02:18

NZGBs are 2-4bps cheaper after the RBNZ left the cash rate unchanged at 3.25%. The decision was widely expected by the market, with only 4bps of tightening priced in.

- From the RBNZ: "The case for lowering the OCR at this meeting highlighted weak near-term growth momentum and the risk of prolonged weakness in economic activity from excess caution by households and businesses in the face of economic uncertainty. This could lead to downward pressure on medium-term inflation. Some members emphasised that further monetary easing in July would provide a guardrail to ensure the recovery of economic activity, whilst being consistent with price stability.”

- “The case for keeping the OCR on hold at this meeting highlighted the elevated level of uncertainty, and the benefits of waiting until August in light of near-term inflation risks. Some members emphasised that waiting would allow the Committee to assess whether weakness in the domestic economy persists, and how inflation and inflation expectations evolve. It would also allow more time to observe developments in the global economy.”

- Swap rates are 6-7bps higher on the day, 4-5bps higher after the decision.

- RBNZ dated OIS pricing is flat to 4bps firmer across meetings. A cumulative 31bps by November 2025 remains priced.

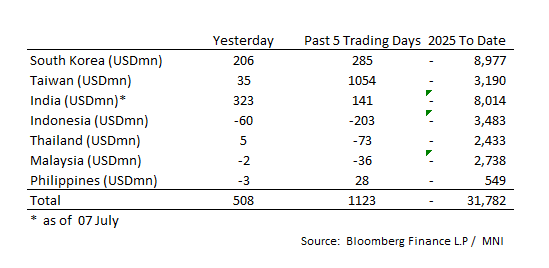

ASIA STOCKS: Decent Day of Inflows as Tariff Headlines Dominate

Jul-09 02:06

Ahead of a Potentially Volatile Period as the tariff deadline approaches, inflows returned yesterday.

- South Korea: Recorded inflows of +$206m yesterday, bringing the 5-day total to +$285m. 2025 to date flows are -$8,977. The 5-day average is +$57m, the 20-day average is -$35m and the 100-day average of -$75m.

- Taiwan: Had inflows of +$35m yesterday, with total inflows of +$1,054 m over the past 5 days. YTD flows are negative at -$3,190. The 5-day average is +$211m, the 20-day average of +$397m and the 100-day average of -$7m.

- India: Had inflows of +$323m as of the 7th, with total inflows of +$141m over the past 5 days. YTD flows are negative -$8,014m. The 5-day average is +$28m, the 20-day average of +$126m and the 100-day average of +$8m.

- Indonesia: Had outflows of -$60m yesterday, with total outflows of -$203m over the prior five days. YTD flows are negative -$3,483m. The 5-day average is -$41m, the 20-day average -$23m and the 100-day average -$33m.

- Thailand: Recorded inflows of +$5m yesterday, with outflows totaling -$73m over the past 5 days. YTD flows are negative at -$2,433m. The 5-day average is -$15m, the 20-day average of -$15m and the 100-day average of -$21m.

- Malaysia: Recorded outflows as of -$2m yesterday, totaling -$36m over the past 5 days. YTD flows are negative at -$2,738m. The 5-day average is -$7m, the 20-day average of -$11m and the 100-day average of -$20m.

- Philippines: Recorded outflows of -$3m yesterday, with net inflows of +$28m over the past 5 days. YTD flows are negative at -$549m. The 5-day average is +$6m, the 20-day average of -$2m the 100-day average of -$5m.