EM LATAM CREDIT: Canacol: Potential Ecopetrol Acquisition - Positive

(CNECN;Caa1neg/CCC+/NR)

"Exclusive | Ecopetrol and Canacol Energy signed an agreement to evaluate a potential acquisition or negotiation." - Valora Analitik

A confidentiality agreement was signed between Charle Gamba, CEO and president of Canacol Energy, and Julián Fernando Lemos Valero, corporate vice president of Strategy and New Business at Ecopetrol to discuss a potential acquisition of the largest independent gas exploration company in Colombia and Colombia government-controlled energy company Ecopetrol.

Canacol has 17% of gas production in the country while Ecopet has 58% with proven reserves of six years of supply for the country overall and imports equaling 20% of consumption as of January 2025 according to Fitch. Canacol was in discussions with Ecopetrol last year about the potential sale of assets.

The deal makes sense as Colombia has become increasingly reliant on gas imports, primarily from the U.S. and Trinidad and Tobago since the current administration does not allow any new fossil fuel exploration. President Petro urged Ecopetrol to consider importing from Qatar as well in order to diversify the country's sources.

Exxon is pursuing regasification in the country to take advantage of the lack of supply. Meanwhile there was an important offshore gas discovery named Sirius made earlier by Petrobras with Ecopetrol having 55% ownership of the joint venture.

CNECN 28s are quoted USD29.5 so clearly at distressed trading levels as the company has been battling liquidity issues as well as production declines for at least a year now. The bonds are down 10 points QTD and about 27 points YTD.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Key Resistance Remains Exposed

- RES 4: 151.21 High Mar 28

- RES 3: 150.49 High Apr 2

- RES 2: 149.38 50.0% retracement of the Jan 10 - Apr 22 bear leg

- RES 1: 148.80/149.18 High Jul 29 / High Jul 16 and the bull trigger

- PRICE: 148.47 @ 18:12 BST Jul 29

- SUP 1: 146.92 20-day EMA

- SUP 2: 146.11/145.86 50-day EMA / Low Jul 24

- SUP 3: 145.16 61.8% retracement of the Jul 1 - 16 bull cycle

- SUP 4: 144.21 76.4% retracement of the Jul 1 - 16 bull cycle

A bull cycle in USDJPY remains in place. The latest recovery signals the end of the corrective phase between Jul 16 - 24. Attention is on key resistance and the bull trigger at 149.18, the Jul 16 high. A break of this hurdle would confirm a resumption of the uptrend. Pivot support to monitor is 146.11, the 50-day EMA. A clear breach of it would instead signal scope for stronger reversal. First support is at 146.92, the 20-day EMA.

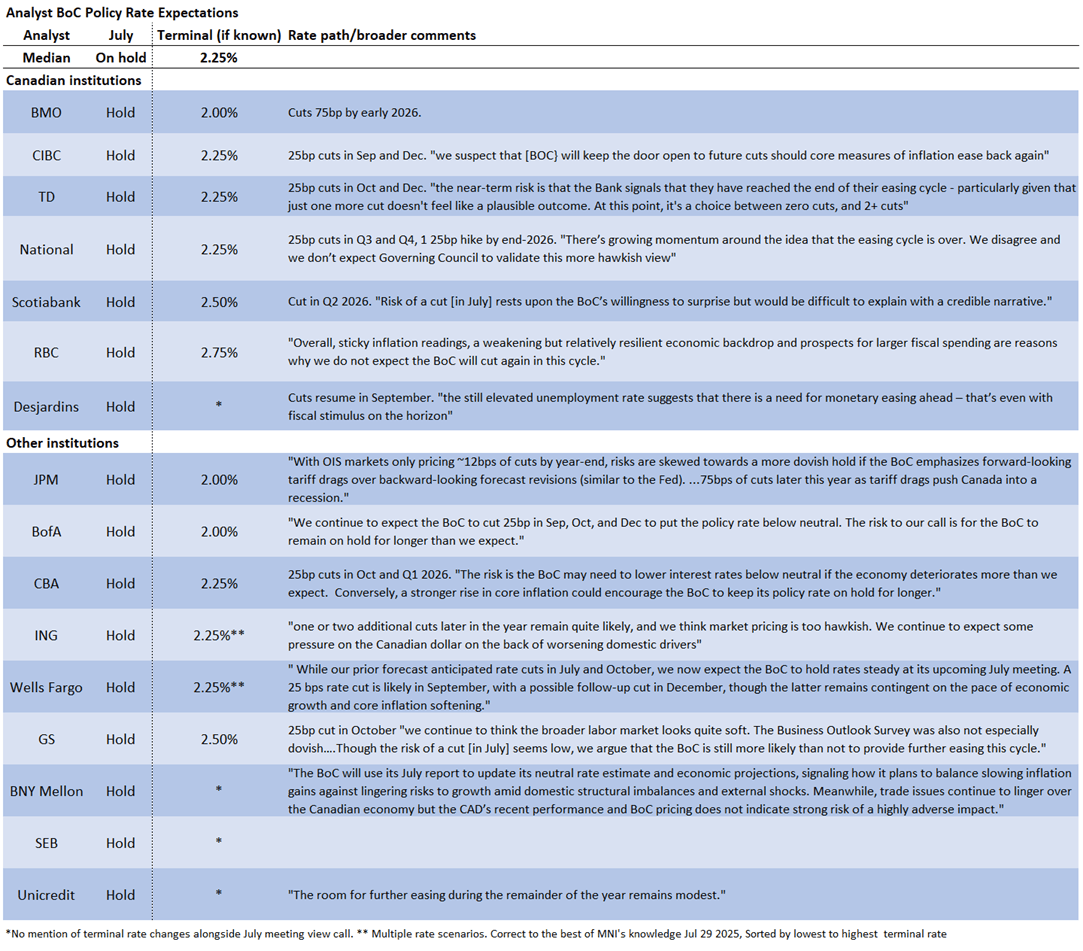

BOC: Rate Cut Expectations Fade Alongside Data Surprises (1/4)

The Bank of Canada is set to hold the overnight rate at 2.75% on Wednesday Jul 30 (decision 0945ET), a third pause after seven consecutive cuts. This would keep rates in the middle of the BOC’s neutral range of 2.25–3.25%. MNI's preview is here (PDF).

- The BoC is prone to surprising markets more than most of its central bank peers. But this is the first upcoming meeting in the last three at which opinion is not split over the decision: there’s under 5% implied probability of a rate cut at this meeting per OIS markets.

- Compare that to 20% on the eve of the June meeting (decision was a hold) and 30-40% in April (again, a hold) when the outcome wasn’t entirely clear. Indeed the last fully-priced decision was March’s 25bp cut, which may turn out the be the final one of the cycle after 225bp in easing.

- Since Q1, data developments have seen market pricing for future cuts slowly evaporate, with analysts not quite convinced but moving in that direction.

- Below is our table of analyst consensus for BOC rates. While most analysts continue to expect at least one or two more cuts by year-end, with most basing their view on expectations that the Canadian economy will weaken sharply, markets (OIS) see no full 25bp reductions seen through year-end (17bp in total over the next 4 meetings to December). That compares to just after the June meeting when a full 25bp cut and then some had been expected.

- We’ve seen the expected BOC terminal rate rise to 2.25% (per MNI consensus), versus 2.125% prior seen prior to the June meeting, and we think this could creep up further.

PIPELINE: Corporate Bond Update: $750M EW Scrips 5NC2 Launched

- Date $MM Issuer (Priced *, Launch #)

- 07/29 $2B #NextEra Energy 2Y +63

- 07/29 $1.5B #Sherwin Williams $500M each: 3Y +47, 5Y +62, 10Y +82

- 07/29 $750M #EW Scripps 5NC2 9.875%