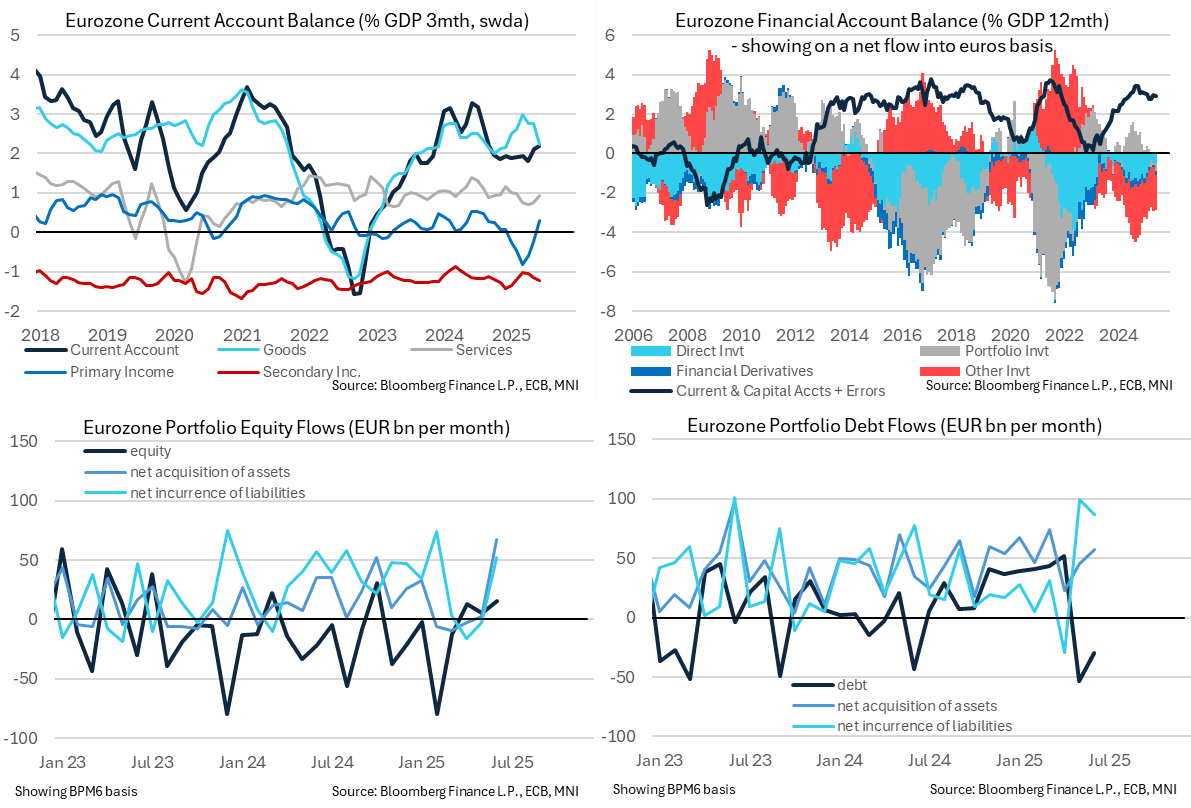

EUROZONE DATA: CA Surplus Widened In June On Income Boost

Aug-20 17:37

- Released yesterday, the current account surplus increased to E35.8bn (swda) in June after a slightly downward revised E31.8bn (initial E32.3bn) in May.

- The goods balance narrowed E10.5bn to E22.6bn (vs a peak of 44bn in March and an average of 30bn in 2024) but it was more than offset by a surge in primary incomes of +E13.4bn to E14.0bn for its largest net inflow since Jun 2024.

- The NSA data suggest that was driven by a swing in portfolio investment flows, with a net outflow of E14bn after a particularly heavy E55bn in May.

- In broader trend terms, the current account surplus amounted to 2.2% GDP in Q2 for a widening from 1.9% GDP in Q1. The goods surplus narrowed to 2.2% GDP from 3.0% GDP but it was countered by the primary income balance shifting to a surplus of 0.3% GDP from a deficit of 0.8% GDP.

- On the financial account side, portfolio net flows were dominated by debt with a not as large net inflow (from a currency perspective) of E30bn after an unusually large E54bn in May. The previous six months saw an average net outflow of E42bn.

- This came as a strong build in overseas debt instruments (E57bn) wasn’t enough to offset another very strong increase in foreign investment into the Eurozone (E87bn in June after E99bn in May).

- Net equity outflows meanwhile increased to E15bn after E5bn, as a large build in Eurozone investor holdings overseas (E68bn) was mostly offset by foreign investment in Eurozone equities of E53bn.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Interview with British Columbia's Energy Minister

Jul-21 17:35

- MNI interviews British Columbia's energy minister on energy sector projects -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

GBPUSD TECHS: Bear Cycle Remains In Play

Jul-21 17:30

- RES 4: 1.3835 High Oct 20 2021

- RES 3: 1.3800 Round number resistance

- RES 2: 1.3681/3789 High Jul 04 / 01 and the bull trigger

- RES 1: 1.3519 20-day EMA

- PRICE: 1.3494 @ 17:00 BST Jul 21

- SUP 1: 1.3365 Low Jul 16

- SUP 2: 1.3335 Low May 20

- SUP 3: 1.3245 Low May 19

- SUP 4: 1.3144 38.2% retracement of the Jan 13 - Jul 1 bull cycle

Prices rallied Monday, prompting GBPUSD to entirely reverse the weakness off Friday highs. This kept the pair clear of any test on recent lows. Nonetheless, last week’s extension lower resulted in a breach of trendline support currently at 1.3470 - drawn from the Jan 13 low. The breach strengthens a bearish threat, exposing 1.3335 next, the May 20 low. On the upside, initial firm resistance to watch is 1.3519, the 20-day EMA. A clear break of this average is required to highlight a potential base.

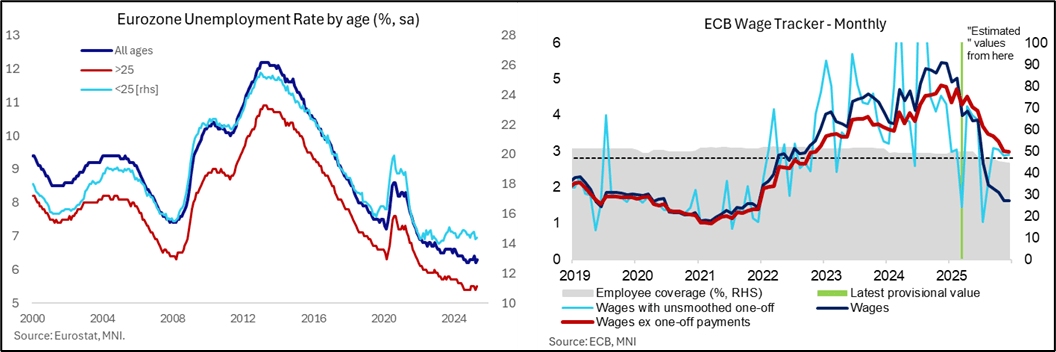

ECB: Macro Since Last ECB - Labour: Wages Still Expected To Cool

Jul-21 17:28

- The unemployment rate was a tenth higher than expected in May at 6.3% as it increased off historical lows of 6.2% in April. It doesn’t change the story, having averaged 6.3% since mid-2024.

- It’s a release that hasn’t been commanding much market attention but President Lagarde has regularly cited this relative resilience of the labour market.

- The more up to date German unemployment rate series from the Bundesbank meanwhile pointed to some further stabilization in June, with a fourth month at 6.3% having ended 2024 at 6.1%, 2023 at 5.8% and 2022 at 5.5%.

- On the wage side, there were slight upward revisions to the ECB's forward looking wage tracker compared to the April vintage, but the broader theme of softening compensation pressures remains intact. The tracker excluding one-off payments is seen at 3.082% in 4Q25 (vs 3.024% in the April iteration).

- On the envisaged moderation from 4.5% in 1Q25, the ECB writes: "The downward trend of the forward-looking wage tracker for the remainder of 2025 partly reflects the mechanical impact of large one-off payments (that were paid in 2024 but drop out in 2025) and the front-loaded nature of wage increases in some sectors in 2024."

- Recall that the ECB projects compensation per employee growth at 2.8% by the last quarter of this year, down from 3.8% in Q1.

- More recently, the Indeed wage tracker for May eased to 2.5% Y/Y (vs 3.2% prior) for the lowest rate since late 2021. The smoother three-month average rate meanwhile was steady at 3.0% Y/Y, revealing a broadly consistent message to that of the ECB’s forward-looking tracker.