EM CEEMEA CREDIT: BSFR: USD BM PNC6 AT1 - FV

Apr-30 10:53

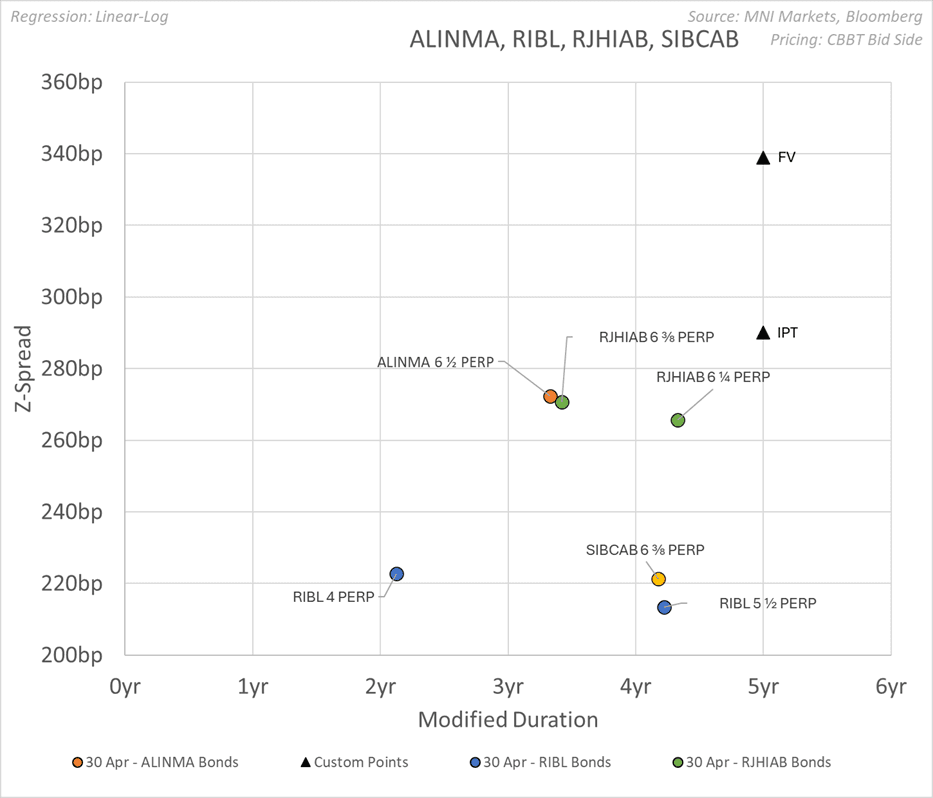

Banque Saudi Fransi (BSFR; A1/A-/A-)

New Issue: USD BM PNC6 AT1

IPT 6.875%

FV: 6.375% or Z+290bp

- Bank Fransi issuing a Perpetual NC6 AT1 bonds. We use 6.5 ALINMA PNC Mar29 which is around 6.05% yield or Z+265bp, 5.5% RIBL PNC Oct29 which are around 6% yield or Z+257bp, 6.25% RJHIB PNC Jul30 which are around 5.96% or z+251bp and 6.375% SIBCAB PNC Nov29 which are around Z+256bp. Adjusting for structure, maturity and ratings we estimate a FV of 6.375% yield or z+290bp.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Gold Bulls Remain In The Driver's Seat

Mar-31 10:50

- On the commodity front, the trend condition in Gold is unchanged, it remains bullish. Today’s strong gains highlight a bullish start to this week’s session and confirm a continuation of the primary uptrend. The rally also once again, highlights fresh all-time highs for the yellow metal. Sights are on the $3151.5, a 3.000 projection of the Nov 14 - Dec 12 - 19 price swing. Support to watch lies at $2992.4, the 20-day EMA. A pullback would be considered corrective.

- In the oil space, despite recent gains, a bearish trend condition in WTI futures remains intact, and gains this month are considered corrective. However, a key resistance at $69.17, the 50-day EMA, has been pierced. The breach strengthens a bullish theme and opens $70.98, the Feb 25 high. For bears, a reversal lower would expose the bear trigger at $64.85, the Mar 5 low. Clearance of this level would resume the downtrend and open $63.73, the Oct 10 ‘24 low.

EQUITIES: Stoxx 50 Futures Move Closer To Next Support

Mar-31 10:44

Euro Stoxx 50 futures see a more convincing break below 5,200.00 at the second time of asking.

- Nothing much in the way of a fresh headline catalyst to drive the latest leg of the sell off, with early NY reaction to overnight price swings perhaps factoring in.

- Oil has pulled back from session highs, another potential factor aiding the move.

- The break below 5,200.00 obviously deepens the bearish technical threat in Euro Stoxx 50 futures. Next support seen at the Feb 4 low (5,160.00).

US TSYS: Risk-Off Start To Quarter-End

Mar-31 10:43

- Treasuries have been confined to relatively tight ranges since opening markedly higher in Japan trading, reflecting broad risk-off flows on a combination of tariff concerns ahead of April 2 "Liberation Day" and geopolitical fears

- Goldman Sachs for example have marked up their 12-month US recession probability from 20% to 35% on the assumption of a 15pp increase in the average US tariff rate vs 10pp previously.

- Cash yields are 4.5-6bp lower on the day, with declines led by the front end.

- 2Y yields have stabilized around 3.85% (touched Mar 11 but last sustainably lower in Oct 2024) whilst 10Y yields have stabilized around 4.20% (hit a few times throughout March).

- 2s10s at 35bp (+1bp) remains off last week’s recent high of above 38bps.

- TYM5 trades at 111-18 (+11+) off an earlier high of 111-22+, on strong overnight volumes of 545k. Resistance at the March 20 high (111-17+) has been pierced, with bulls now looking to force a break above the March 11 high (111-25) as they aim to build further on last week's gains. Attention is on key resistance at 112-01 (Mar 4 high).

- Data: MNI Chicago PMI Mar (0945ET), Dallas Fed mfg Mar (1030ET)

- Bill issuance: US Tsy $76B 13W & $68B 26W Bill auctions (1130ET)