MNI EXCLUSIVE: BoJ Set To Look Through Recent Market Moves

The BOJ sees no immediate impact of higher JGB yields and yen strength on monetary policy -- on MNI Policy MainWire now, for more details please contact sales@marketnews.com.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

UK DATA: UK Public Sector Finance Due at 7:00 GMT

- UK markets are particularly sensitive to growing fiscal risks at present. This is likely to be the last release to be incorporated into the OBR's EFO forecasts (which will be published alongside the Chancellor's spring statement on 26 March).

- December is a month where self-assessment income tax receipts edge up, ahead of the January 31 payment deadline, as early tax submissions begin. The OBR forecasts SA tax receipts of GBP2.2bln in December (vs GBP0.6bln in November).

- Interest payments are likely to be higher than the OBR forecast (the OBR expected the Bank rate at 4.40% in Q1 and 3.84% by end of 2025).

- Currently, the fiscal year-to-date CGNCR (Central Government Net Cash Requirement) is running a cumulative GBP147.4bln between April and November 2024, after rising GBP16.3bln in November. It lies marginally below the updated OBR forecast of GBP148.2bln for Apr-Nov 2024 period. For the month of December, the OBR expect it to rise a further GBP19.4bln.

- PSNBex (public sector net borrowing ex public sector banks) is expected to be GBP14.6bln according to the OBR. Current PSNBex fiscal YTD is slightly above the OBR estimate at GBP113.2bln (OBR forecast GBP111.2bln).

- The Bloomberg consensus looks for PSNB inc public sector banks at GBP14.2bln (vs 11.2bln prior), with analyst estimates wide ranging between GBP13-15.5bln.

- Finally, the OBR forecast the current budget deficit to rise GBP 8.7bln in December (vs 6.8bln prior). Between April and November 2024 the deficit stands at GBP76.8bln, 0.3bln above the OBR forecast.

EURGBP TECHS: Outlook Remains Bullish

- RES 4: 0.8545 High Aug 21

- RES 3: 0.8530 76.4% retracement of the Aug 8 - Dec 19 downleg

- RES 2: 0.8494 High Aug 26 ‘24

- RES 1: 0.8474 High Jan 20

- PRICE: 0.8444 @ 06:43 GMT Jan 22

- SUP 1: 0.8403/8371 Low Jan 16 / 20-day EMA

- SUP 2: 0.8345 50-day EMA

- SUP 3: 0.8284 Low Jan 8

- SUP 4: 0.8263 Low Dec 31

A bull cycle in EURGBP remains intact and the cross is trading closer to its recent highs. Gains this month undermine a bearish theme and suggest scope for stronger short-term recovery. Resistance points at 0.8376, the Nov 19 high, and 0.8448, the Oct 31 high, have been breached, strengthening the current bullish theme. Sights are on 0.8494 next, the Aug 26 ‘24 high. Support at the 50-day EMA is at 0.8345.

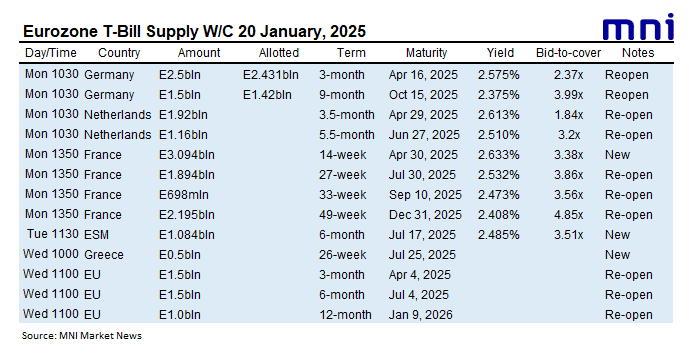

EUROZONE T-BILL ISSUANCE: W/C January 20, 2025

Greece and the EU are both due to sell bills this week, whilst Germany, the Netherlands, France and the ESM have already issued this week. We expect issuance to be E20.3bln in first round operations, up from E18.0bln last week

- Today, Greece will issue E0.5bln of the new 26-week Jul 25, 2025 GTB.

- Also today, the EU will sell up to E1.5bln of the 3-month Apr 4, 2025 EU-bill, E1.5bln of the 6-month Jul 4, 2025 EU-bill and E1.0bln of the 12-month Jan 9, 2026 EU-bill.

For more on future auctions see the full MNI Eurozone/UK T-bill auction calendar here.