BOC: BOC Instant Answers

Mar-06 14:46

- Overnight Rate Target (level) 5%

- Does the Bank say it may need to raise interest rates further? Not answered

- Does the Bank signal it could lower interest rates? No

- Does the Bank signal it may slow quantitative tightening? No

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: EUR Markets Unwilling To Price Less than 125bp Of '24 ECB Cuts

Feb-05 14:42

ECB-dated OIS has been unwilling to sustain any moves pricing less than 125bp of cuts for ’24 (equating to a 25bp cut at 5/7 remaining '24 monetary policy meetings), with session extremes of ~124bp registered on that front, before a move back to ~128bp as of typing. The U.S. ISM services survey and final reading of the S&P Global equivalent print provide the next macro inputs.

| ECB Meeting | €STR ECB-Dated OIS (%) | Difference Vs. Current Effective €STR Rate (bp) |

| Mar-24 | 3.872 | -3.4 |

| Apr-24 | 3.748 | -15.8 |

| Jun-24 | 3.497 | -40.9 |

| Jul-24 | 3.261 | -64.5 |

| Sep-24 | 3.019 | -88.7 |

| Oct-24 | 2.826 | -108.0 |

| Dec-24 | 2.628 | -127.8 |

CANADA: BoC FX Volumes Survey - October

Feb-05 14:39

The BoC has today released its semi-annual survey of the nine banks with the largest FX sales activity in Canada (full here).

- The monthly turnover in October of traditional FX products (spot transactions, outright forwards and foreign exchange swaps) totaled ~US$3.3 trillion, or $163.5bn on an average daily basis (+9.7% from Apr’23).

- Traditional products: Spot transactions $19.6bn (+4.5% from April), outright forwards $18.0bn (-6.1%) and FX swaps $125.8bn (+13.3%) – all average daily basis.

- FX derivatives: $13.3bn average daily turnover (unch from April).

- Vs a year-ago: the average daily turnover of traditional FX products +9.4% vs FX derivatives -18.7%.

- Institutional investors dominate spot and outright forward markets (62.5% and 59.4% shares) but the market is more balanced across FX swaps (36.5% vs 31.2% hedge funds and prop. trading).

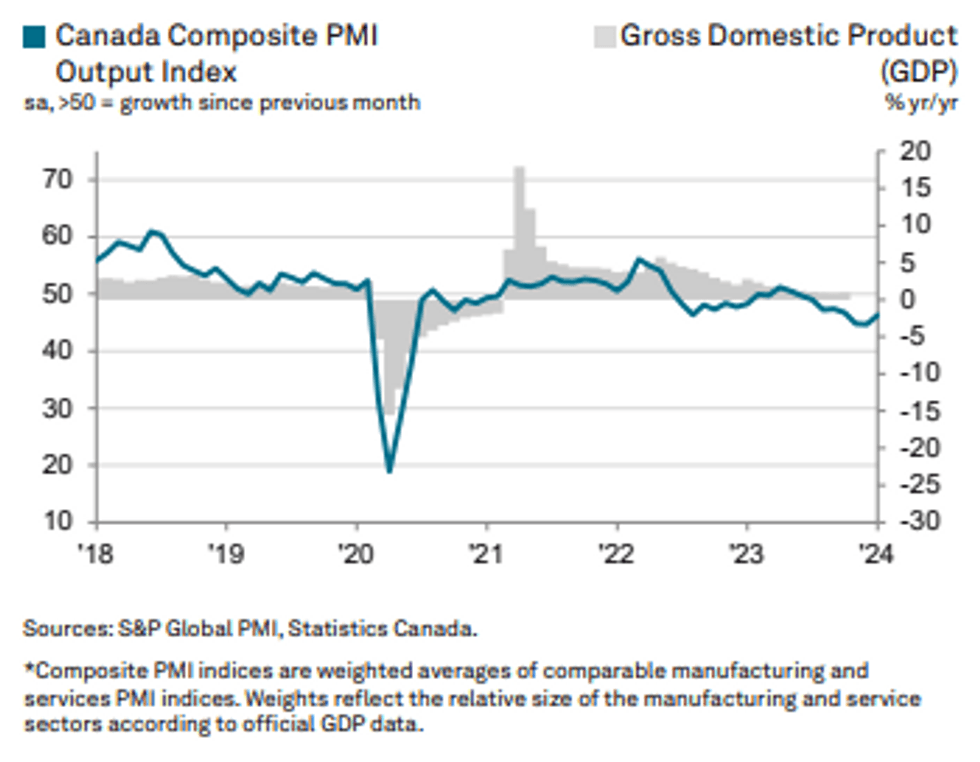

CANADA DATA: PMI Sees Slower Pace Of Contraction, Firms Pass On Higher Costs

Feb-05 14:37

- The S&P Global Canadian composite PMI increased from 44.7 to 46.3 in January, a shallower contraction than in December but nevertheless extending the current decline to eight months. Full press release here.

- “Volumes of new orders displayed a similar trend to activity, falling again but at a slower rate. This allowed companies to keep on top of work outstanding, which fell for a nineteenth month in a row” whilst employment increased for first time in three months.

- “Price indices showed accelerated rates of inflation in January as firms sought to pass on higher costs to clients.”

- “Confidence in the future softened since December to its lowest level since July 2022.”

Source: S&P Global

Source: S&P Global